One Pager on Three Interesting Data Center proxies:

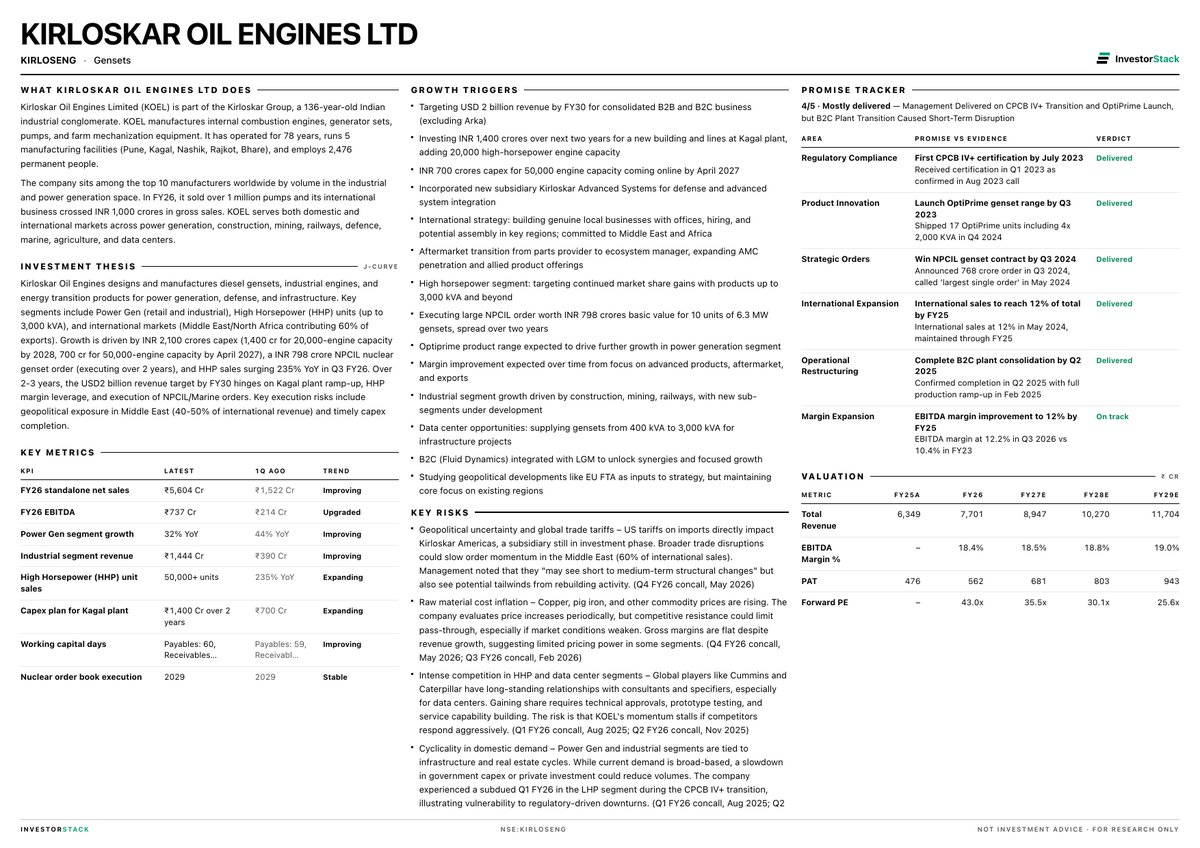

Kirloskar Oil Engines: manufactures diesel gensets, industrial engines. Growth driven by 2100cr capex, nuclear genset order, and HHP sales. secured a 192MW data centre genset supply order.

Clean Max: India's largest renewable energy provider, Data center contracted capacity grew 10x to 2,400 MW in two years. Over 2-3 years, the company will execute 2,600 MW under construction, expand Datacenter exposure, and reduce leverage costs to 8.5%

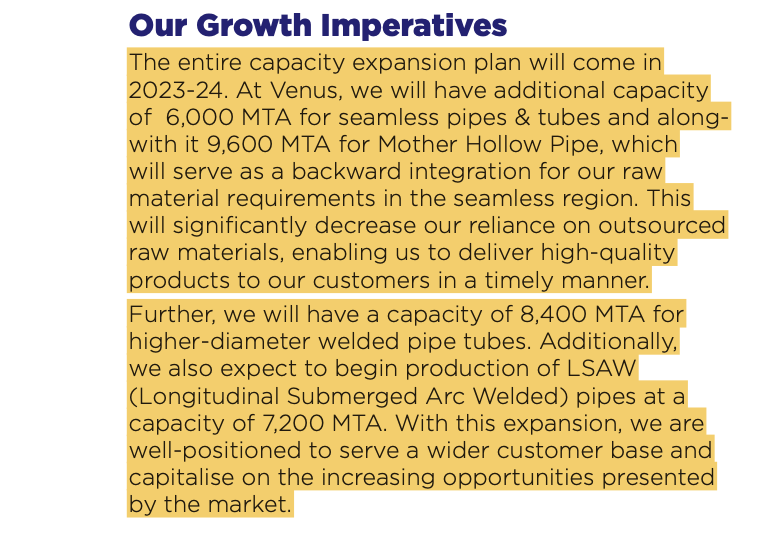

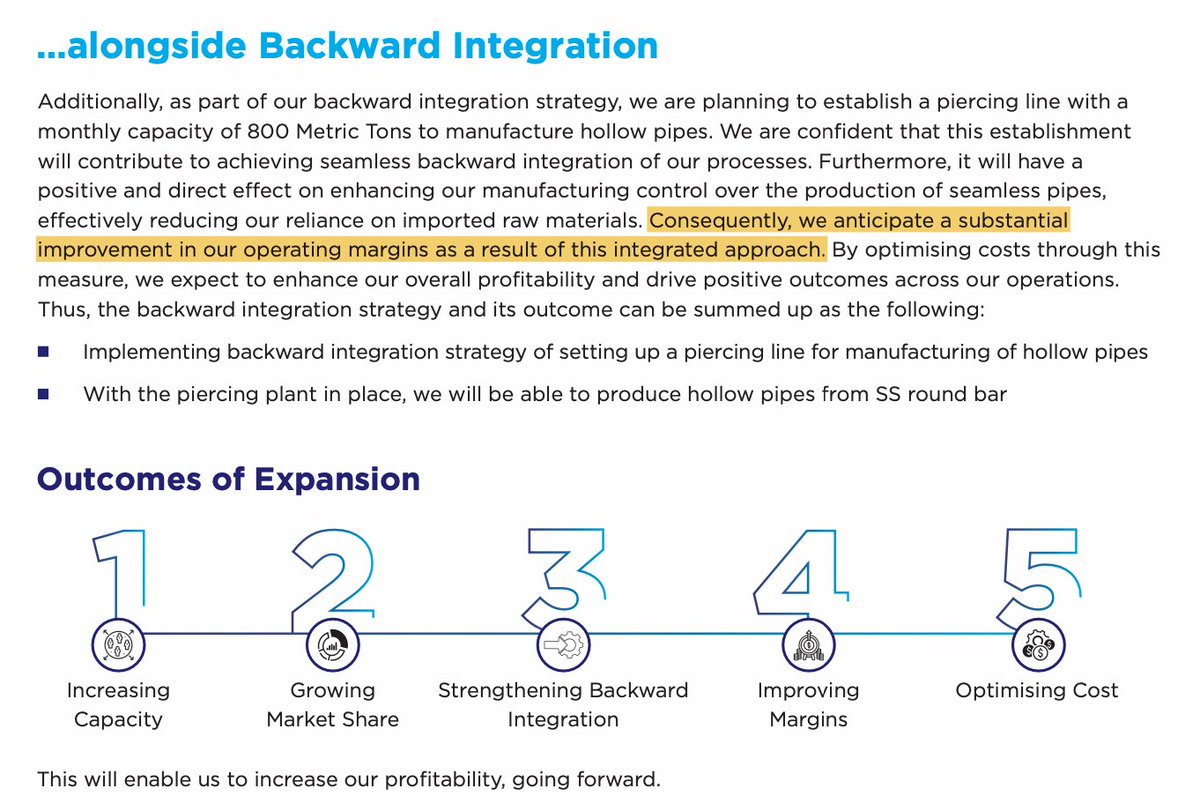

Venus pipes: Manufacturer of stainless steel seamless and welded pipes. Expanding into higher margin value added products like fittings and condenser tubes. 20% revenue growth for the next two years. 185cr LOI for a liquid cooling fluid network from data center operator.

Guidance just after listing will always be good , don't forget promoter block selling always come a year after , so they will always paint the best picture !

guidance based investing is a very risky business , works mostly in aggressive bull markets and in bear markets those same stocks are over owned by the same people calling it turnaround !

🚨 The Next #Multibaggers May Not Be In The #Nifty 50. 👀

I'm tracking these companies that are targeting aggressive growth over the next few years 🚀👇

🔹#Azad Engineering

🔹 #GNG Electronics

🔹 #TD Power Systems ⭐

🔹 #Sai Life Sciences

🔹 #Aeroflex Industries

🔹 #Inox India

🔹 #Quality Power Electrical Equipments

🔹 #DEE Development Engineers ⭐

🔹 #Lumax Auto Technologies

🔹 #MTAR Technologies

🔹 #Aimtron Electronics

🔹 #Sansera Engineering

🔹 #CCL Products

🔹 #Navin Fluorine

🔹 #SJS Enterprises

🔹 #Sterlite Technologies

🔹 #Emcure Pharmaceuticals

🔹 #Knowledge Marine & #Engineering Works

#Great wealth is often created when companies scale faster than the #market expects.

📌 Save this list.

Which stock from this list has the highest upside potential? 👇

#IndianStockMarket #MultibaggerStocks #Investing #SmallCapStocks

#SECTOR #Analaysis

#Post

#ParthElectrical & Engineering Ltd

Very informative presentation from a 320 Cr MicroCap growing more than 50% in power sector may be kept in Radar for nibbling when available at decent valuations during ongoing market correction.

Link to Investor Concall : https://t.co/AqCizdo7xG

STL Networks Ltd

Business: End-to-end fibre network services + system integration + data-centre network build company (brand: Invenia); demerged from Sterlite Tech on 31-Mar-25 and listed 4-Sep-25. Does design → deploy → O&M for telcos, govt (BharatNet, NFS-defence), enterprises. 1.35 lakh+ route-km of OFC laid across 23 states, 2.5 lakh home passes done, ~50 DCs under management.

Why this stock now ? Answer is " Promotor Warrants".

Board approved 18-Apr-26: 4.5 Cr convertible warrants to promoter Twin Star Overseas at ₹24 (vs CMP ₹30.2) = ₹108 Cr raise. 75% (₹81 Cr) earmarked for debt repayment, 25% (₹27 Cr) for general corporate purposes.

Promoter stake rises from 44.16%→47.73% post-conversion.

Quantified impact: On Sep-25 borrowings of ₹827 Cr, ₹81 Cr repayment = ~10% absolute debt reduction. At ~14% borrowing cost, interest savings of ~₹11 Cr/yr material when TTM loss is ₹73 Cr.

Promoter taking 18-month exposure at ₹24 (share value) = strong conviction signal; parent #STLTECH warrant issue at ₹110 simultaneously shows group-level re-rating push.

Valuation: Stock trades at ~1.6x P/S, 1.7x P/B — at a severe discount to larger comparable services peers (HFCL ~2.5x P/S at substantially bigger scale).

Risk: Top customer concentration not publicly disclosed but BharatNet J&K = ~40% of order book.( Of course WC challenges can be )

All key information's has been explained in below.

Disc: This is only for education purpose.

@Shashank1171@manikanth2304 aur kuch ?

One of the unique capital good companies that checks our filter of unique businesses -

→ High barriers to entry

→ Cannot be replicated just via blank cheque

→ Good return ratios

→ Limited competitors

→ Doing something cutting edge

Let’s discuss more on Inox India’s Business in 3 simple steps

→ Why this business is Unique

→ Financial Health

→ Growth Triggers

Pharma/chemicals isn't my niche but I'm learning.

Came across a player attempting something impressive.

While most Indian API companies live with one constant risk:

🇨🇳 China cuts prices → margins disappear.

This one company is playing a completely different game.

Instead of fighting Indian peers in crowded generic APIs, they are targeting niche molecules where China dominates and then taking market share away through regulatory approvals, quality and backward integration.

Management has openly stated that they prefer products where China has dominance and they can replace Chinese suppliers.

The playbook is simple:

→ Enter small, high-value markets

→ Avoid commodity price wars

→ Build deep backward integration

→ Use US FDA & EU GMP credentials as a competitive weapon

→ Capture business from less regulated Chinese suppliers

Today ~75-80%+ of the business is backward integrated.

And the next phase could be even more interesting.

The Ambernath facility is expected to become a major growth engine, with management targeting asset turns of ~2.5x from the site.

If executed well, Supriya won't be just another API manufacturer.

It could become one of the few Indian pharma companies systematically building micro-monopolies in niche chemistries.

While everyone is watching the obvious China+1 beneficiaries...

A less hyped trend may be unfolding:

An Indian company taking market share directly from China, molecule by molecule.

Expect to launch 30 approved ANDAs in the next 6 to 8 quarters

This will result in significant growth by taking total products from 20 to 50

US govt national contracts will be major growth driver

Plan to do 4000 registration in EMs from current 500

Senores pharmaceuticals

"Competition heats up in India’s smartphone manufacturing sector as PLI winds down - The Economic Times"

That's what a scheme like PLI should result in, isn't it ?

https://t.co/bXBDpYglj4