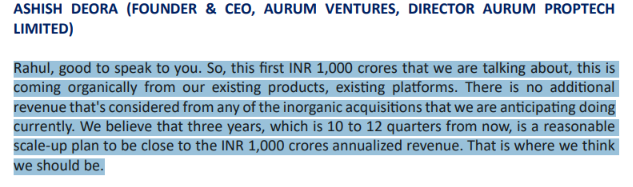

Aurum Proptech : Company aims to touch 1000 cr in annualized revenue within 10 to 12 quarters. Their current revenue in FY26 is 381 cr, which means they aim for more than 30% CAGR revenue growth rate.

Profitability margin will be around 8-10% when they will touch 1000 cr.

It is surely one of the few companies in the IT services industry which can grow at such high pace.

Piccadily Agro : Aims to grow the top-line by 60-70% in FY27 and similar growth is expected in EBITDA also.

It is surely one of the fastest growing companies in the alcohol industry..

Avoid doing the following 3 mistakes in the stock market as an investor :

1. Many people intentionally ignore a falling stock because seeing losses makes them disheartened. Find out the reasons for the fall. If business fundamentals seems strong for the next few quarters, then stay invested in the business and ignore the share price. But, if business fundamentals have changed, then exit the stock immediately, even if you have to sell it at a loss. Your aim at that time should be to protect the remaining capital.

2. Avoid investing in business models you can't understand. There are so many companies across various sectors and you should invest only in those companies whose business you can understand.

3. Never invest in FOMO. If you are buying a stock simply because there a lot of people around you talking about the company or because the stock is making new ATH everyday or because the stock is trading at a very cheap P/E, then you are entering into the trade without conviction.

These stocks may bring profits for you but it will come at the cost of mental stress. Ex - Investing around US stocks. I am not saying that they are fundamentally good or bad, but you should only buy US stocks if you are not having FOMO and your investment is backed by proper logic.

Q4 FY26 results season has been a memorable one for me..

I have analyzed so many companies across various sectors and uploaded my analysis on my X handle. We still have 20 days remaining before we start the Q1 FY27 earnings season and I would like to cover 3-4 more sectors.

Btw, the sectors which I have analyzed are :

1. Affordable Housing

2. NBFC

3. C&W industry

4. Stock Exchanges

5. Microfinance space

6. Alcohol

7. Tea & Coffee sector

8. EMS

9. Hospital

10. Jewellery (Sky Gold and Kalyan only)

11. Small Finance Banks

12. Stock brokers

13. E2W (Ather only)

I have analyzed only those companies in each of the above sector which can grow their business at a very high pace in the future. I have not analyzed those companies which will be growing at a very low speed in the future.

I believe that investors should only focus on good companies and cut out all other companies with worsening fundamentals.

For the remaining 20 days, I will try to analyze Auto Ancilliaries, Small cap IT companies, PEB, Real estate and Jewellery sector. If I analyze 2 companies everyday, I can easily complete this target. Let's see what happens..

InfoBeans Tech is a small cap company in the IT sector industry. It primarily engages in providing solutions to their clients' complex business problems by using modern technology.

Some examples of services they provide are specially designed AI-powered solutions for Banking, Insurance aur Risk management, HR led services, AI led engineering projects, etc.

95% of their clients give them repeat business orders, and their top 5 clients contribute to 40% of total revenue.

They have their two own AI accelerators namely Expona 2.0 and InsaneSDD 2.0, which play an important role in their AI led development strategy.

Q4 FY26 has been their best quarter so far, with revenue reaching 142 cr, a 37% YoY growth. In FY26, revenue grew by 30% YoY to 514 cr and EBITDA margins went up to 22%.

Receivables have been increasing at a fast pace because most of their revenue comes from Fortune 500 clients, and they follow a 90 days payment cycle.

They did not give any revenue guidance but said that EBITDA margins will be around 24% or above.

Polycab has the highest market cap in the Cables & Wires industry and has grown its revenue in Q4 FY26 by 27%.

All the other companies in this industry must grow faster than Polycab because they have a relatively smaller base and huge market to capture.

But not everyone are performing better than Polycab. We shall not analyze those companies which are not doing better than Polycab, and shall analyze those which are doing better.

Don't give me direction on what to do and what not to do. I have already started my content creation journey and one day I might start a smallcase.

Focus on yourself. You are just an anonymous fool who doesn't even has the courage to keep your picture as your profile photo and your name as username. Better focus on improving yourself in life rather than giving gyan to anyone else and commenting on their posts.

Only 7 companies in Nifty 50 have reported more than 25% revenue growth in this quarter.

20 companies have reported revenue growth less than 10% in this quarter.

The performance of Nifty 50 has not been good and this is not the story of just this quarter, but it has happened in multiple quarters before.

All the persons who are doing SIP in Nifty 50 have no knowledge about markets and are just doing what they system is telling them to do.

Learning active investing is no longer a choice, it has become a necessity if you want to earn superior returns on your capital.

Fund managers are educated fools. A retail investor can easily beat the returns generated by a fund manager if he invests in companies which have high earnings growth momentum in future.

And I am not feeling anything. Anybody who wants to earn superior returns has to learn active investing. 90% lose in trading because they trade without logic. Here I am talking about investing, not trading.

How can anyone give his hard earned money to an unknown fund manager who is further investing the money in these shit stocks. Mutual funds will never make you rich. Learn active investing and don't relate this with cooking. Both are different.

If you do some mistake while cooking pakora, it can be corrected when you cook next time. If you do some mistake in investing, your capital is gone. Tata, good bye 👋

Aeroflex Industries : A company which will benefit from the AI boom!!!

Business performance in FY26--

Exports contributes to - 69% revenue

Domestic contributes to - 31% revenue

Assembles & Others contributes to - 52% revenue

Hoses contributes to - 43%

SFN Skid Assemblies (High margin product) contributes to - 5%

They currently have the capacity to manufacture 6000 skid assemblies p.a. which they will take upto 15000 by Q2 FY27. Capacity will also be increased for hoses, and assemblies.

In Q4 FY26-- Revenue growth - 37%, EBITDA margins - 24%

ROCE & ROE impacted by deployment of funds in capex, subsidiary investments, and long-term working capital and others, will improve over the next few years.

My 5 favourite Microfinance players after the Q4 FY26 results selected according to the future guidance given by the management :

1. Credit Access Grameen - Expected growth in AUM in FY27 is 20-25%.

2. Suryoday SFB - 30% growth in loan book expected & PAT of more than 300 Cr (2X YoY)

3. Ujjivan SFB - Grew by 27% in Q4 FY26. Expected to grow by 25% in FY27.

4. Arman Financial - FY27 guidance not given, but the performance of the business is improving. Definitely one of the few companies which should be in your watchlist if you want to play the MFI cycle.

5. Utkarsh SFB - 25-30% AUM growth expected in FY27.

Diagnostics space : Detailed discussion on the entire space and further analysis of three companies Vijaya Diagnostics, Thyrocare, and Metropolis.

The companies are analysed on the basis of several parameters like:

1. B2C vs B2B comparison

2. Pathology vs Radiology department

3. Current performance

4. Future capex and guidance

.

.

B2C(high margin) and B2B share -

Vijaya- 92% and 8%

Thyrocare - 45% and 55%

Metropolis - 60% and 40%

Radiology(high margin segment)-

Vijaya - 40%

Thyrocare - 5%

Metropolis - 5%

Vijay has a current EBITDA margin of 42%, FY27 guidance is 40% on a conservative basis. They plan to deepen their presence in existing non-core clusters like Kolkata (West Bengal), Pune, and Bangalore (Karnataka) to maximize operating leverage. All their new stores will be COCO models. The company's major focus for the next 2 to 3 years is capacity addition and volume-driven revenue growth, rather than price hikes (which are only expected to contribute around 1% to 1.5% to realizations).

Thyrocare FY26 reported EBITDA margin is 32%. Their focus is to provide good quality diagnostics at affordable cost. So their revenue growth eventually comes down to how much volume growth they can expect, which will come by more and more expansion as well as benefit from existing hospitals.

• Overall Expectations: The company is guiding toward a mid- to high-teens overall revenue growth expectation for FY '27. Management noted they feel reasonably confident revising this guidance marginally upward compared to their historical mid-teens baseline.

• Drivers: Volume growth is expected to be the primary catalyst, driving roughly 75% of the revenue growth, with the remaining 25% coming from the product mix. They expect to maintain current 32% EBITDA margins.

Metropolis guide this mid-teens revenue growth, 14% to 15% that they have guided for the next 3 years, is obviously a combination of volume, RPP increase, as well as some price increase, and that's the breakup of it. Metropolis has an EBITDA margin of 24% in FY26 and they guide for around 28% in FY27.

[Watch the video for detailed analysis]

In Q4 FY26, MCX grew its revenue by 205% YoY to 889 cr and PAT grew by more than 3.5 times. Let's analyze the company in detail.

🔹MCX is India’s leading commodity derivatives exchange. MCX has over 99% share across bullion, base metals and energy.

🔹In FY26, revenue grew by 107%, primarily driven by the growth in Average Daily Turnover (F&O) of Bullion and Energy across the entire market. Turnover in Bullion increased due to the rapid growth in gold price over the past few quarters. Turnover in Energy increased due to the Iran-US war.

🔹They did not give any revenue growth guidance for FY27 but according to me, If the war ends soon, the ADTO in Energy might take a hit after one or two quarters, while the ADTO in bullion is expected to remain high in India for the upcoming few quarters. So, the revenue growth in FY27 depends primarily on the Iran-US war. If this war continues for a long time, we can expect FY27 as another good performing year for MCX.

🔹They will focus on launching new products in FY27 which will primarily be related to metals and energy. Focus will also be on improving the BULLDEX and METALDEX indices like introducing shorter notional amount contracts in the index.

🔹Volumes some sort of dipped in April in Futures and Options segment, but management says that they still expect FY27 to be a strong year.

🔹The core moat of the business is liquidity, because of which they have a competitive advantage. Although their competitors have plans to start commodity and metals trading, they still believe that they are in a comfortable position with respect to market share and they believe that since they provide high liquidity, retailers are likely to stick with them.

Iran - US war is still going on. Till the war goes on, volume in energy contracts will continue rising. Apart from this, we can never predict gold and silver prices. Any movement in prices and the volume in gold and silver will also increase. Earnings might not have peaked as management says FY27 will also be a strong year.

My 5 favourite NBFCs after the Q4 FY26 results selected according to the future guidance given by the management :

1. Poonawalla Fincorp- Management gave guidance of 35-40% growth in AUM but can do even more better than this.

2. Capri Global Capital - 25-30% AUM growth rate expected in FY27.

3. Aye Finance - 25-30% AUM growth rate expected in FY27.

4. Tata Capital - 23-25% expected growth rate in AUM (Considering their huge base, this is a good guidance if executed successfully)

5. SBFC Finance - AUM growth expected to be around 23% in FY27. They guide to double their loan book over the next 3-3.5 years.