⚖️ MMAT (Meta Materials Inc.)

Case: In re Meta Materials Inc.

Case No.: 24-50792-gs (Chapter 7, District of Nevada)

Document: 2836

Filed/Entered: June 4, 2026

📋 What Happened?

Judge Gary Spraker denied the Trustee’s request for an expedited status hearing regarding the DTCC subpoena dispute.

Importantly, the judge did not rule on the merits of the DTCC issue itself.

Instead, the judge said the Trustee’s application was too vague and did not adequately explain:

Whether the hearing was about the entire bankruptcy case or just DTCC.

Key Quote

“It is unclear to the court whether the scope of the requested status conference is the bankruptcy case in general or only the allegedly deficient response from DTCC to the trustee’s subpoena.”

Key Outcome

“The Ex Parte Application to Set Status Hearing (ECF No. 2833) is DENIED without prejudice…”

The words “without prejudice” are important. They mean the Trustee can come back and file a more detailed request.

⸻

🤔 What Could This Mean?

Most Likely Interpretation

The judge appears to be saying:

“Tell me exactly what the problem is, what you want me to do, and follow the proper procedure.”

This looks more like a procedural denial than a substantive rejection.

Possible Next Steps

The Trustee could:

File a Motion to Compel DTCC compliance.

File a more detailed request for a hearing on shortened time.

Raise the issue during an already scheduled hearing if appropriate.

Continue negotiations with DTCC before seeking court intervention.

⸻

👀 Reading Between the Lines 👇

💥💥One sentence stands out:

💥💥”The court has reviewed the case docket, and it does not appear that any motion to compel DTCC’s compliance with the trustee’s subpoena is pending.”

👆 👆👆👆👆👆👆👆👆👆👆👆👆👆

That could be interpreted as the judge signaling:

“If DTCC isn’t producing what you need, file the proper motion and bring the dispute before me.” 🎯

In other words, the court may be looking for a concrete discovery dispute rather than a general status conference. 💥

⸻

Bottom Line

📌 This is a procedural setback, not necessarily a substantive loss.

📌 The DTCC issue remains unresolved.

📌 The Trustee can refile with more detail or pursue a motion to compel.

📌 The June 16 hearing will be worth watching to see whether the DTCC dispute is addressed in some form.

⚠️ Not legal advice. This is a layman’s interpretation of Doc. 2836 filed June 4, 2026.

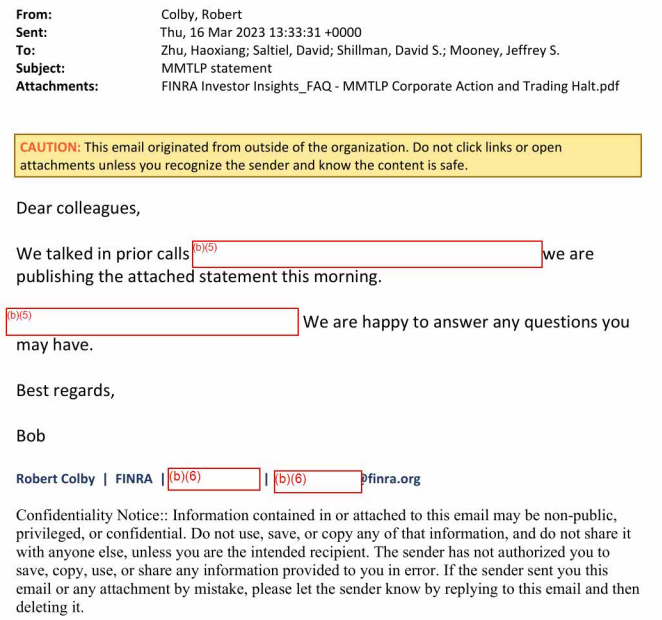

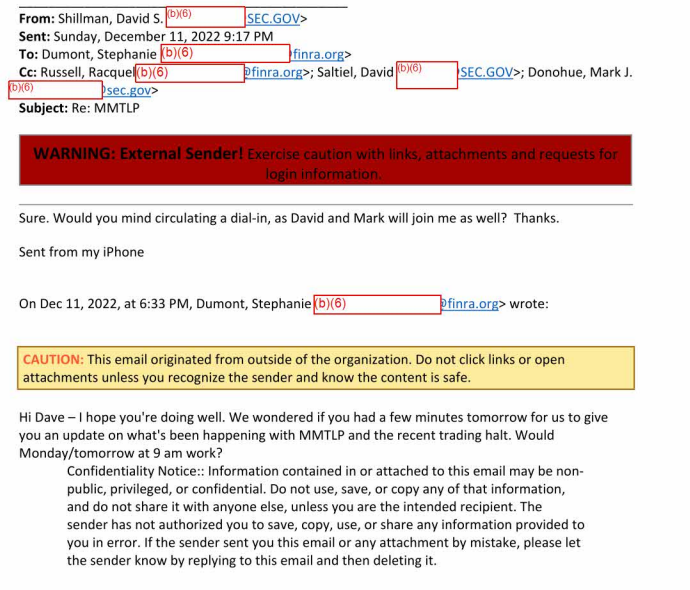

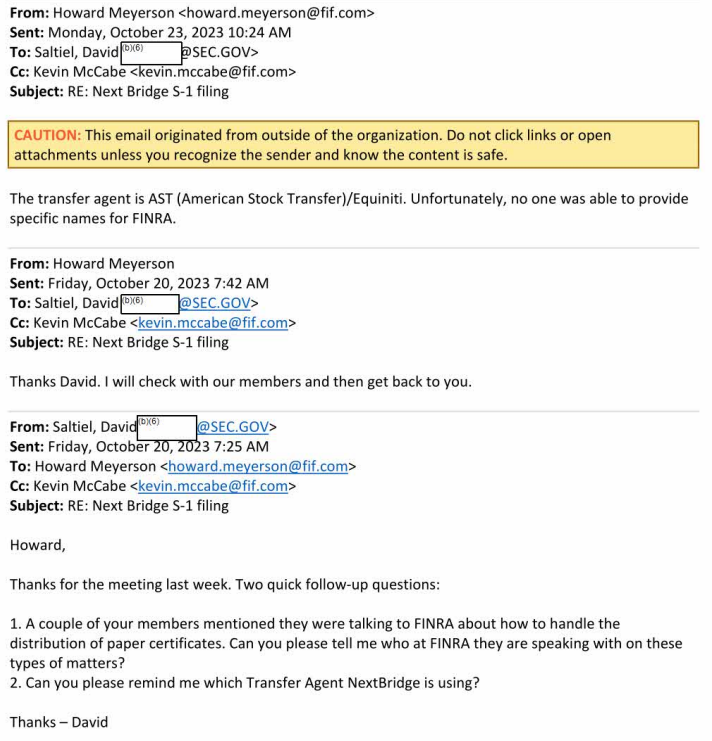

🚨 NEW SEC FOIA RESPONSE 🚨

FOIA 26-00651-FOIA

This one matters.

This FOIA requested records showing communications/referrals between SEC Corporation Finance and SEC Trading & Markets regarding Next Bridge Hydrocarbons’ S-1 activity.

The response shows something important:

Once FIF entered the discussion, the tone and substance appear to shift.

Before FIF:

SEC / NBH S-1 communications were largely about registration mechanics, eligibility, disclosure, and process.

After FIF steps in:

The discussion turns to operational market-structure concerns:

• shares on loan

• lending broker-dealers unable to recover shares

• customer protections under SEC Rule 15c3-3

• IRA/tax consequences

• transfer-agent capacity

• whether shareholders should be forced out of bank/broker/nominee holding

One FIF point is especially hard to ignore:

“Because of the prior FINRA trading halt, there are shares on loan that lending broker-dealers cannot recover.”

That is not retail speculation.

That is an industry group raising operational concerns to the SEC about the Next Bridge S-1 process.

And FIF’s recommendation?

Do not force participating customers out of bank, broker-dealer, or nominee custody — because preserving that structure would allow for “future reconciliation of outstanding stock loans.”

Read that again.

Future reconciliation of outstanding stock loans.

This FOIA does not prove every theory.

But it does prove the S-1 issue was not just routine paperwork.

It involved broker-held shares, loaned shares, customer protections, transfer mechanics, and reconciliation concerns.

That is exactly why MMTLP shareholders have been asking questions for years.

#MMTLP #MMAT #NextBridge #FOIA #SEC #FINRA

🦋 MMAT | Meta Materials Inc.

Case No. 24-50792-gs (Chapter 7)

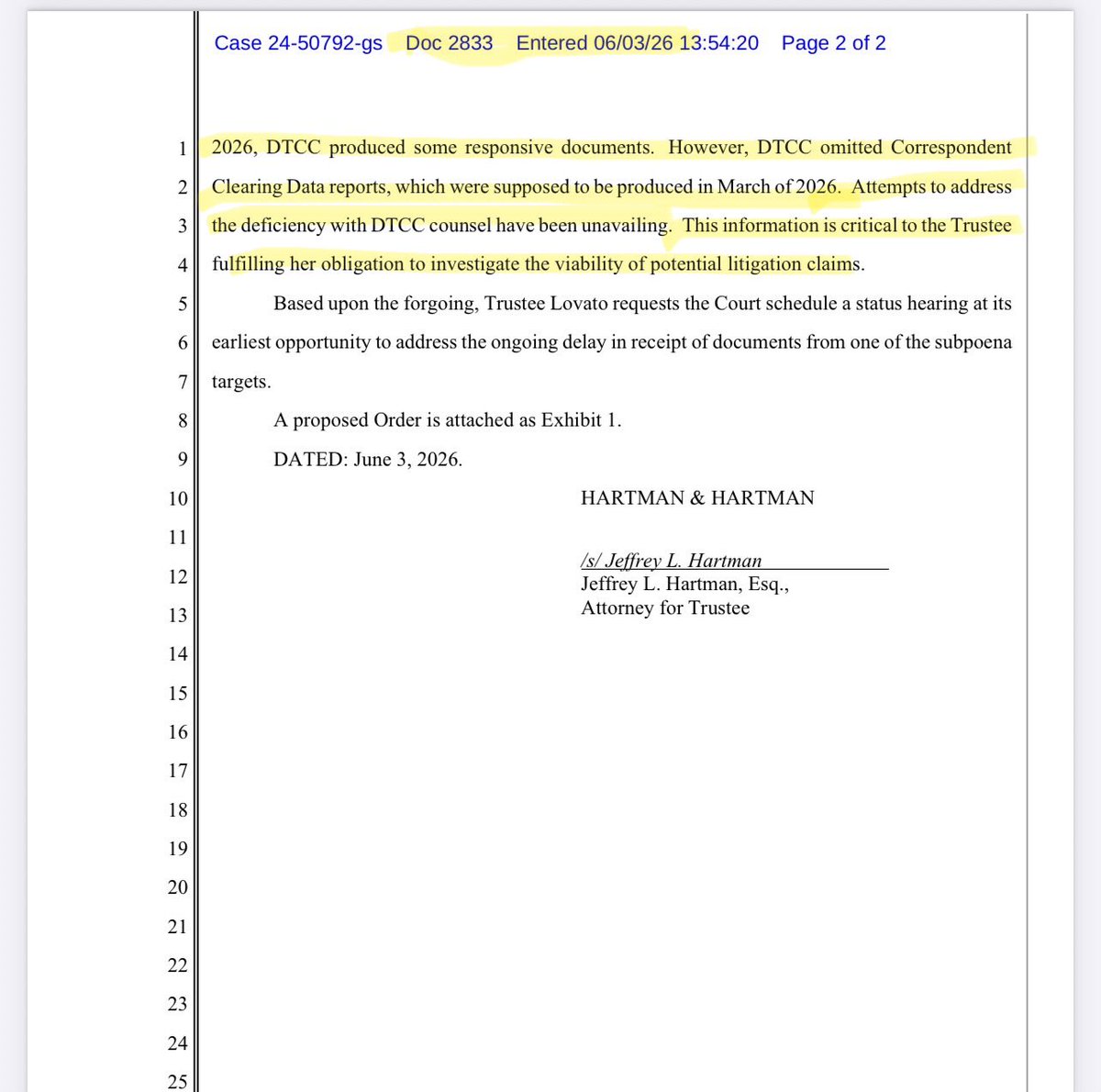

📅 Filed: June 3, 2026

📄 Docket No. 2833 – Ex Parte Application to Set Status Hearing

⚖️ Layman’s Summary

Trustee Christina Lovato is asking Judge Spraker to schedule a status hearing because DTCC has allegedly not provided all of the subpoenaed records the Trustee believes were due months ago.

🔥 Key Quote

“DTCC omitted Correspondent Clearing Data reports, which were supposed to be produced in March of 2026.”

🚨 Why It Matters

The Trustee tells the Court:

“This information is critical to the Trustee fulfilling her obligation to investigate the viability of potential litigation claims.”

In plain English:

👉 The Trustee believes important DTCC data is still missing.

👉 Efforts to resolve the issue privately have failed.

👉 The missing information is important to determining whether litigation claims exist.

👉 The Trustee wants the Court involved to move the process forward.

📌 Bottom Line

This filing suggests the MMAT investigation is still active, the Trustee is still seeking additional DTCC records, and she believes those records are important to evaluating potential legal claims.

⚠️ Not Legal Advice.

Ohhhh, now I understand what you mean when you said “With transparency, not everything is always great. You turn on the lights and you see things.” (video below)

part 7: I would like to share compelling points relating to the HBC equity raise and its use to secure the position of the Holder of Interests, which forced participation in the $BBBYQ third-party release. I hope you like it.

$BBBY

(old).

MMTLP #NBH#FOIAdenials#SECfraud

Another day, another step forward in exposing the #MMTLPfiasco manufactured by FINRA and the SEC.

Today I received an Appeal response that included a new batch of documents from a shareholder who chose to remain anonymous. Appreciate your hard work on this FOIA.

The result: 91 additional Congressional & SEC letters tied to MMTLP. All PDFs will be added to the dashboard for full transparency.

The contents of these letters and responses were efforts of shareholders and Members of Congress asking for answers about MMTLP and the U3 halt. Amazing effort!

To everyone pushing for truth and accountability — thank you. Stay locked in.

Focus...

🚨NEXT BRIDGE HYDROCARBONS RELEASES PR ANNOUNCING THE EFFECTIVENESS AND AVAILABILITY OF UP TO 40 MILLIONS SHARES OF NBH COMMON SHARES @ $15/SH.

MMTLP MMAT TRCH NBH

@nbhydrocarbons

https://t.co/df52HGhBtS

Signed up for $EBAY account, received the following welcome email.

*******

Your account has been suspended

Hello XXXXX,

We wanted to let you know that your eBay account has been permanently suspended because of activity that we believe was putting the eBay community at risk.

⚖️ WHAT THIS MEANS PRACTICALLY

The trustee now gains access to a significant amount of trading data that the Court believes may help determine:

🧩 Whether viable claims exist

🧩 Whether wrongdoing occurred

🧩 Whether the estate suffered damages

🧩 Whether litigation should be filed before limitation deadlines

This does NOT mean:

❌ Anyone has been found liable

❌ Manipulation has been proven

❌ The trustee automatically wins anything

BUT…

✅ The investigation survived.

✅ Discovery survived.

✅ The Court largely sided with allowing investigation over shutting it down.

https://t.co/zBQuOHWqxE

🦋⚖️ $MMAT / $MMTLP — Meta Materials Inc.

⚖️ U.S. Bankruptcy Court, District of Nevada

📄 ORDER ON MOTION TO QUASH

📅 Filed: May 27, 2026

⚠️NLA

🚨 BIG PICTURE — WHAT JUST HAPPENED?

Judge Gary Spraker just issued a MAJOR ruling against:

🏢 Citadel Securities

🏢 Virtu Financial

🏢 Anson Funds

These firms tried to QUASH (block) the bankruptcy trustee’s subpoenas seeking trading data tied to:

📈 $MMAT

📈 $TRCH

📈 $MMTLP

The Judge said:

❌ The subpoenas are NOT being fully thrown out.

✅ The trustee CAN obtain important trading records.

⚠️ BUT there will be strict protective-order limitations.

⸻

🧠 LAYMAN’S TERMS

The trustee believes there MAY have been market manipulation or wrongful conduct connected to Meta Materials trading activity.

The trustee is trying to determine:

🔍 Was trading activity harming the company?

🔍 Did it impact fundraising?

🔍 Did it damage the bankruptcy estate?

🔍 Are there potential legal claims worth pursuing before statutes expire?

The Judge basically said:

“The trustee has the right to investigate.” ⚖️

⸻

📌 THE COURT EMPHASIZED RULE 2004 IS VERY BROAD

The Court repeated that Rule 2004 examinations are basically:

🎣 “Fishing expeditions”

📂 Broad investigative tools

🔎 Used to uncover wrongdoing or estate assets

The Judge cited multiple cases saying trustees can investigate third parties to determine whether wrongdoing occurred.

⸻

🚨 HUGE PART — THE COURT ACCEPTED THE TRUSTEE’S THEORY ENOUGH TO ALLOW DISCOVERY

The trustee identified:

📊 11 separate “events”

where Meta or Torchlight allegedly:

💰 Sold treasury shares

📉 Issued dilution

📈 Raised capital

📄 Issued warrants/acquisition stock

during periods where the trustee claims trading manipulation may have affected pricing.

The Non-Parties argued:

❌ “Meta wasn’t actually selling into the manipulated market.”

❌ “The trustee lacks standing.”

❌ “This is too speculative.”

Judge Spraker was NOT persuaded enough to stop discovery. 👀

⸻

⚠️ VERY IMPORTANT — THE JUDGE DREW A LINE

The Court said:

🛑 This is NOT the stage where the Court decides whether Citadel/Virtu/Anson actually committed wrongdoing.

Instead:

✅ The trustee only needs enough justification to INVESTIGATE whether viable claims might exist.

That distinction matters A LOT.

⸻

👀 THE JUDGE ALSO SHOWED SOME CONCERN

This part is important.

The Court acknowledged concerns that:

⚠️ The trustee’s special counsel is involved in OTHER securities litigation against Citadel and Virtu.

⚠️ Rule 2004 discovery cannot simply become a shortcut for outside litigation.

⚠️ Discovery should benefit the bankruptcy estate — not unrelated lawsuits.

So the Judge imposed guardrails.

⸻

🔒 PROTECTIVE ORDER INCOMING

The Court ordered the parties to negotiate a STRICT protective order.

That order must:

🔒 Limit use of produced data -THIS bankruptcy

🔒 Limit use to trustee-related litigation

🔒 Restrict dissemination of data

🔒 Restrict access to trustee + approved professionals only

🚨 RESPONSE DEADLINE:

📅 June 18, 2026 — Protective order must be submitted to the Court.

⸻

🚨 BIGGEST DEADLINE OF ALL

📅 JUNE 25, 2026

The Judge ordered Citadel, Virtu, and Anson to PRODUCE:

📊 Market-wide trading data

📈 For the 161-day schedule identified by the trustee

📂 Under the Rule 45 subpoenas

unless modified by the protective order.

That is the MAJOR headline here. 🚨🚨

⚖️ WHAT THIS MEANS PRACTICALLY

The trustee now gains access to a significant amount of trading data that the Court believes may help determine:

🧩 Whether viable claims exist

🧩 Whether wrongdoing occurred

🧩 Whether the estate suffered damages

🧩 Whether litigation should be filed before limitation deadlines

This does NOT mean:

❌ Anyone has been found liable

❌ Manipulation has been proven

❌ The trustee automatically wins anything

BUT…

✅ The investigation survived.

✅ Discovery survived.

✅ The Court largely sided with allowing investigation over shutting it down.

SIGNIFICANT legal victory for the trustee!

MMAT | In re Meta Materials Inc. | Case No. 24-50792-gs | Doc 2820 | Filed May 27, 2026

Order Granting in Part and Denying in Part FINRA’s Motion to Quash Trustee Subpoenas

⚠️ Not Legal Advice

The big picture

This is a major discovery win for the Chapter 7 Trustee.

Judge Spraker basically said:

“FINRA, you do have to turn over important trading/manipulation-related data. But there are limits, and the trustee has to pay certain production costs.”

This order is directly tied to the trustee’s investigation into potential manipulation of Meta stock (MMAT / TRCH / MMTLP).

⸻

What happened in plain English

FINRA tried to block the subpoenas

FINRA asked the court to either:

Kill the subpoenas entirely (motion to quash) OR

Narrow them significantly via protective order.

The judge said:

Not entirely. Some yes. Some no.

Hence:

“Granted in part, denied in part.”

⸻

What the Trustee WON 🥇

1) Short Interest Data — PRODUCE IT

FINRA must turn over reported short interest data.

That includes:

TRCH + MMAT

Sept. 21, 2020 → Aug. 21, 2024

MMTLP

June 28, 2021 → Dec. 14, 2022

Layman’s meaning:

This shows what broker-dealers were reporting as short positions.

This helps answer:

Was short interest unusually elevated?

Did reported short positions match actual market behavior?

Were there anomalies around key events?

⸻

2) TRF Data — HUGE 🧨

FINRA must produce Trade Reporting Facility (TRF) data.

Same date ranges.

This is likely one of the most important parts of the order.

Why?

TRF captures off-exchange / OTC reported trades, often associated with internalized trading / market maker activity.

Layman’s translation:

If the trustee is investigating alleged manipulation, this is where some of the most meaningful footprints could live.

Judge even ordered:

FINRA must expedite production due to time pressure.

That’s important.

⸻

3) Reg SHO Daily Short Sale Volume Data

FINRA must produce this too.

Same date ranges.

This helps show:

Daily short sale activity

Short-sale patterns

Whether activity spiked during sensitive periods

Not proof of wrongdoing by itself.

But valuable puzzle pieces.

⸻

Timing priority (important) 👀

📆FINRA agreed to prioritize production in this order:

MMAT 2023

MMAT 2024

MMAT 2022

MMAT 2021

Then TRCH

Then MMTLP

Why that matters:

The trustee likely wants the most actionable data first given statute/time pressure.

⸻

Judge explicitly referenced manipulation investigation

This is a key line.

Judge ordered FINRA to move quickly because of:

“potential manipulation of Meta stock.”

That’s notable.

This is not a finding that manipulation occurred.

But it confirms the court recognizes the trustee’s investigation as legitimate and time-sensitive.

⸻

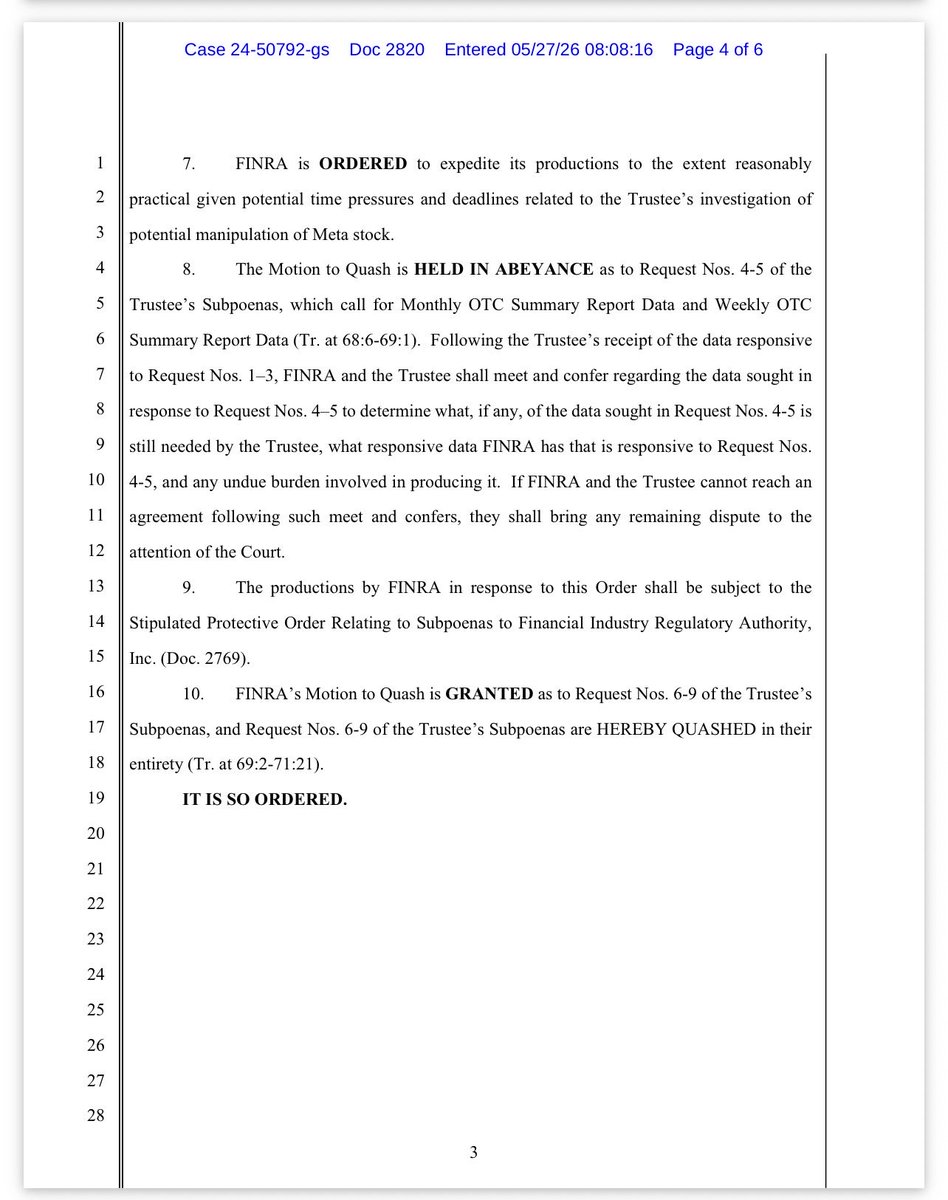

Requests put on HOLD (not denied yet)

Requests 4–5:

Monthly OTC Summary Report Data

Weekly OTC Summary Report Data

Judge said:

Let’s wait.

Reason:

The trustee may get enough from Requests 1–3 first.

If more is still needed, the parties must meet and confer.

If they still fight, they can come back to court.

Translation:

This door is still open.

⸻

What FINRA WON

Requests 6–9 were QUASHED entirely.

Meaning:

FINRA does NOT have to produce whatever those categories were seeking.

So this was not a total trustee sweep.

⸻

Costs — trustee pays

Because FINRA is a nonparty, Rule 45 cost protections apply.

Meaning:

If producing the data is expensive or burdensome:

the trustee pays the production costs.

This matters because FINRA had argued massive burden.

The judge basically said:

“Produce it—but the estate can shoulder the cost.”

⸻

Protective order remains in place

Anything produced stays under the existing protective order.

Meaning:

This data is not automatically public.

It’s controlled discovery material.

So no—this does not mean shareholders get to immediately see raw trading records.