Stock Portfolio manager for Sharek's Stock Portfolios. Averaged 18% a year for 22 years including 7 years of 40%-plus. Author of The School of Hard Stocks. 🏫

I'm from Buffalo and am a wing connoisseur. I'm not aware of a good chicken wing place here in Miami, especially downtown. I see growth opportunity.

I'm also a stock portfolio manager, who's owned $WING for clients for years. Here's proof: https://t.co/WfqQA6gCcZ

I think this is a one-year downturn for the company. The chicken sandwich rollout was a HUGE catalyst for the company, in previous years, and now things are back to normal. So year-over-year comparisons might be tough. But soon, we will be looking at easier yoy comparisons.

My Fair Value is 55x earnings or $257 a share. Before you say the P/E is too high, note the P/E was 55 two quarters ago.

@25YearsAgoLive Steve Buschemi should star in a movie called Pip Squeak where he gets picked on, rebels back, is about to say good night when Vince Vaughn steps in as the hero and saves the day.

Retatrutide trial results are insane:

- 86% liver fat reduction

- 72% prediabetes reversal

- 41% stopped needing BP meds

- 14 mmHg blood pressure drop

- Increases metabolic rate at rest

It also makes you eat less and burn more calories at rest. Truly an incredible compound.

someone made the most ADDICTIVE game to learn DATA CENTER networking

its called Data Center, $6 game, you start with bare floors, buy racks, mount servers, route every cable by hand

the INSANE part, every customers traffic shows as colored balls rolling through your cables... you literally see bottlenecks in real time

180 reviews in 48 hours, people with RTX 4090 rigs are HOOKED on a $6 cabling sim

As of March 30, 2026

The AI Photonics and Optical Infrastructure sector is getting hammered across the board today, with $AAOI leading the collapse at -13.26%. The catalyst is tariff risk: under the January 14 Section 232 semiconductor proclamation, Commerce and USTR are required to deliver a report to President Trump by April 14 on the outcome of semiconductor tariff negotiations, and traders are front-running potential escalation before that deadline hits names with heavy Taiwan and China manufacturing exposure. (https://t.co/hAQbGhopK9) Finviz

The selloff is indiscriminate across every layer of the photonics value chain, from 1.6T transceivers down to substrates and equipment. The lone exception is $ALMU, bucking the tape on its US-based large-diameter InGaAs platform and lighter direct tariff exposure versus Asia-heavy peers.

$ALMU: +3.85%

$SIVE: +0.86%

$SPX: -0.39%

$NDX: -0.78%

$BESIY: -1.84%

$POET: -2.12%

$KEYS: -3.46%

$GFS: -3.63%

$SOI: -3.68%

$IQE: -5.71%

$GLW: -6.04%

$FORM: -6.66%

$LITE: -6.82%

$AEHR: -7.40%

$MRVL: -7.45%

$TSEM: -7.76%

$LWLG: -8.91%

$CIEN: -9.12%

$FPLSF: -9.68%

$COHR: -9.79%

$FN: -10.89%

$AXTI: -13.03%

$AAOI: -13.26%

1. Optical Transceivers & Active Networking

$AAOI, $CIEN, $COHR, $LITE, $FN: The frontline 800G/1.6T transceiver cluster is absorbing the most damage. AAOI's dual exposure through Taiwan foundry relationships and China assembly makes it the clearest tariff target in the watchlist. CIEN and COHR don't get a pass either given their global supply chain footprints.

$MRVL: Networking silicon with deep TSMC dependency. Any tariff escalation on advanced node imports pressures the margin story directly, and the stock is pricing that in at -7.45%.

2. Compound Semiconductor Substrates & Foundries

$AXTI, $IQE, $TSEM, $GFS, $SOI, $FPLSF: The substrate and foundry tier is getting hit almost as hard as the transceiver names. AXTI at -13.03% reflects direct InP substrate tariff risk tied to its China operations, making it the picks-and-shovels casualty of the day. TSEM at -7.76% carries heat as a key foundry for the sector, while SOI and FPLSF compound the damage on thin OTC float.

3. Early-Stage Photonic Materials & PICs

$POET, $LWLG, $SIVE, $BESIY: Pre-revenue names selling off in sympathy but holding up relatively better than the large-cap transceiver cluster. BESIY at -1.84% and POET at -2.12% see limited direct supply chain exposure since they aren't shipping at volume yet.

$ALMU: The only green name on the watchlist today. US-based InGaAs compound semiconductor platform with domestic manufacturing sits outside the direct tariff blast radius. Aeluma named a VP of Materials Operations in March 2026 to lead scaling of its large-diameter epitaxial wafers into volume production Stocktitan, and that domestically anchored narrative is working as a relative safe haven in today's tape.

4. Semiconductor Equipment, Test & Infrastructure

$AEHR, $FORM, $KEYS, $GLW: Equipment and test names follow the sector lower but with slightly less severity than the transceiver cluster. GLW at -6.04% reflects the risk of optical fiber capex guidance cuts if hyperscaler build plans get revised under tariff pressure. AEHR and FORM carry GaN/SiC test exposure that bleeds into the optical infrastructure trade.

Elon Musk joined Trump’s call with Modi on Tuesday to discuss the Hormuz crisis. The New York Times confirmed it, citing two US officials. On March 19, Musk posted three words on X about the strait: “We got lazy.”

Those three words are the most honest assessment any major industrialist has offered about what this war exposes. And Musk’s companies sit at the exact intersection of every vulnerability the war has created.

SpaceX uses helium to pressurize Falcon 9 and Starship propellant tanks. Roughly 10,000 to 20,000 liters per Falcon launch. Qatar produced one-third of the world’s helium before Iranian missiles hit Ras Laffan on March 18. That helium is now offline for three to five years per QatarEnergy’s CEO. Spot prices have doubled.

Tesla’s semiconductor supply chain depends on the same helium for wafer cooling and etching at Samsung and SK Hynix fabs. South Korea imports 64.7 percent of its helium from Qatar. xAI’s training infrastructure requires the same chips. Starlink’s constellation deployment depends on SpaceX launch cadence, which depends on helium availability for ground operations.

One element. Four companies. One chokepoint.

But here is what makes the Musk angle different from every other CEO caught in this crisis: he has been building the exit ramps for years.

Starship uses full autogenous pressurization. Instead of helium, it vaporizes a small fraction of its own methane and oxygen propellant through dedicated heat exchangers integrated into the Raptor engine and feeds the vapor back into the tank to maintain pressure. This eliminates roughly 95 percent of external helium use per launch. Falcon 9 partial retrofits are already delivering 70 to 80 percent reduction per Payload and Ars Technica reporting.

Tesla’s Megapack deployments hit record levels in Q1 2026. Every barrel of oil that costs $108 instead of $70 accelerates the economic case for solar, batteries, and EVs. The war that threatens Musk’s supply chain simultaneously validates his energy independence thesis.

And the Trump-Modi call was not just about energy. Starlink India approval has been pending for years. Musk on that call, discussing Hormuz and energy prices with the leaders of the world’s largest democracy and its most powerful economy, is not a courtesy. It is leverage. Foreign Policy reported on March 20 that the “privatization of diplomacy” through Starlink has become a defining feature of American foreign policy.

SpaceX is reportedly filing its IPO prospectus this week or next per Bloomberg, Reuters, and The Information, targeting a mid-to-late June 2026 listing at $1.5 to $1.75 trillion. The largest IPO in history. Filing into a war that simultaneously threatens his supply chains and proves the thesis that built his companies.

The US produces 81 million cubic metres of helium per year, roughly 35 to 40 percent of global supply per the USGS, with 8.5 billion cubic metres of recoverable reserves. America can supply what Musk needs. The question is whether the logistics and refining infrastructure can scale fast enough to bridge the gap while Qatar’s machines are offline and the strait remains contested.

Musk said we got lazy. His companies were not.

https://t.co/32ixeQpfif

@WalesSalesRE@FreightAlley Hey Ben, I cover stocks like a snuggie. I think the best stock in the industry is Old Dominion $ODFL. But its a tricky stock to buy into. You gotta get in on a dip. That dip was late 2025 (and I passed on buying, ugh).

Google just dropped a compression algorithm that makes AI 8x faster while using 6x less memory. Zero accuracy loss.

It's called TurboQuant. Here's why it matters in plain English:

Every time you talk to ChatGPT or any AI, the model has to remember everything you've said in the conversation. That memory is called the "key-value cache." The longer the conversation, the bigger the cache, the more expensive it gets to run.

This is the single biggest bottleneck in AI right now. A 128,000-word conversation on a large model eats 40GB of GPU memory just for that one user. Scale that to thousands of users and you're burning millions in compute costs reprocessing the same data over and over.

TurboQuant compresses that memory down to just 3 bits per value (from 32 bits) without losing any quality. Independent developers tested it within hours and got exact matches against full-precision output.

What this actually means:

- AI models that needed a $10,000 workstation could now run on a MacBook

- Always-on AI agents become dramatically cheaper to operate

- Open-source models that were too big for consumer hardware suddenly fit

- The cost curve for every company running AI infrastructure just shifted

Developers are already porting it to Apple Silicon. No retraining required. It drops into existing AI systems without modification.

The AI cost problem isn't being solved by building bigger data centers. It's being solved by mathematicians figuring out how to do more with less.

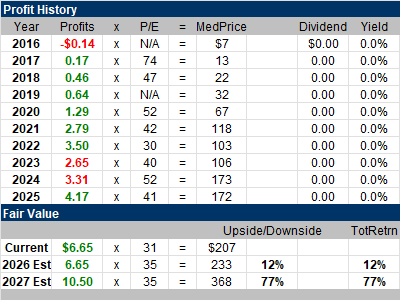

$SMCI was a monster stock, running from a breakout around $80 to $1250 from late 2022 to mid 2024 (prior to a 10-for-1 stock split).

At the time, profit growth was so fast and the P/E was so low that it seemed like the next Dell (from the 1990s).

Here's my one-year chart and Fair Value table from 2022 Q4:

I don’t know how many have caught onto this yet, but this ~$27B $NBIS X $META deal showcased a masterclass in negotiations from the $NBIS team:

“Furthermore, in connection with access to these NVIDIA Vera Rubin deployments, Meta has committed to purchase additional available compute capacity across certain upcoming Nebius clusters up to a total of $15 billion over a five-year period”

Do you understand the implications of this?

H2 2026 Vera Rubin deployment is more than just a “sample” deployment, it’s active negotiation leverage

Listen to the wording: “in connection with access to these NVIDIA Vera Rubin deployments”

Key words: in connection

It means $META (basically) only wanted access to the VRs, and since $NBIS is one of few that received first-to-market orders of VRs from $NVDA, they were able to negotiate an EXTREMELY lucrative deal for themselves:

$12B deal with $META + $META commits to purchase up to $15B in upcoming compute from upcoming clusters (optional for $NBIS)

This deal ensures that upcoming (confirmed) DCs will have a tenant (in $META) no matter what, BUT it also gives $NBIS the option to leverage the $META deal as a “floor value” in future contract negotiations with bare-metal tenants (i.e, any offer would have to exceed $META to win a deal), or they could more aggressively target enterprises with their PaaS offering as they have the $META deal to partially/fully fall back on.

It’s Excellent!

Huge kudos to the whole @nebiusai team on this deal!

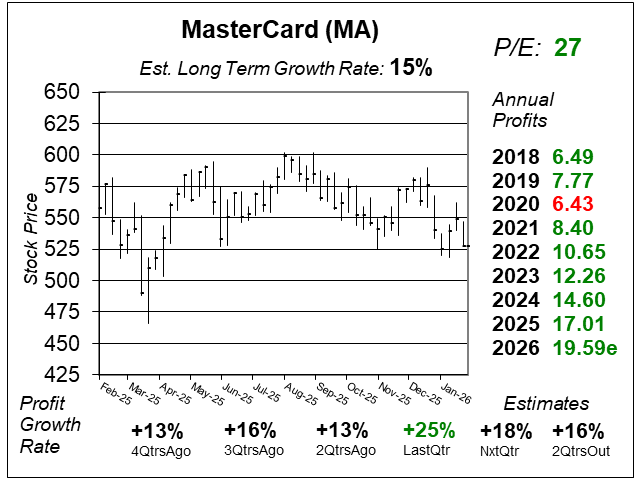

MasterCard $MA with solid profit growth of 25% last qtr. Fastest profit growth since late 2023. Nice upside in my opinion, as the stock has sold off recently. I own MA in all my model portfolios.