This clip with @AndrewBaileyMO on @TheRobbCarter is very important, it recognition of the problem, the SEC. When i call @DLHoskins and @AGCHanaway office and leave a message that i would like a call back. Crickets! Why is Missouri dropping the ball on financial fraud? #MMTLP

🙈🙉 DO NOTHING HESTER 🙊🙊

Hester Peirce finally leaving the SEC.

Quick question Hester before you go.

HOW MANY LETTERS DOES THE SEC NEED TO RECEIVE TO TAKE ACTION❓️❓️

MMTLP sent in over 50k letters

over 70 Congressional signatures and it has been over 3 years.

Many investors in many tickers have sent letters, FOIA requests and made Whistleblower reports.

ZERO ACTION TAKEN

SEC DOESN'T PROTECT INVESTORS IT'S COVERS UP CRIME‼️

The financial reset is happening.

There are many aspects to this reset:

1. Accountability in actual share counts.

2. Legal and financial title reconcilable in a court of law.

3. Real World Assets (RWA) are replacing financial instruments as people want to take delivery of “the real thing” versus trade the paper facsimile of said asset.

4. Commodities are rising while naked short selling of stocks are being exposed.

#MMTLP has stood in the gap exposed by the greed of the Wolves of Wall Street.

The below referenced lawsuit is the canary in the coal mine that will result in a seismic shift in accountability.

Investors will find faith renewed as Wall Street will no longer be able to trade and sell financial instruments/stocks they don’t own.

It’s all about tangible assets. Whether it be a stock like MMAT or an exchange like @abaxx_exchange , the world is waking up to the financial fraud perpetrated by the banking overlords whose system is collapsing while the business of RWA is rising.

The sun is rising and a new dawn is illuminating what’s real and what’s fake.

And the people who stood beside real will reap the rewards of their sacrifice and perseverance.

🚨Breaking news: 🦋

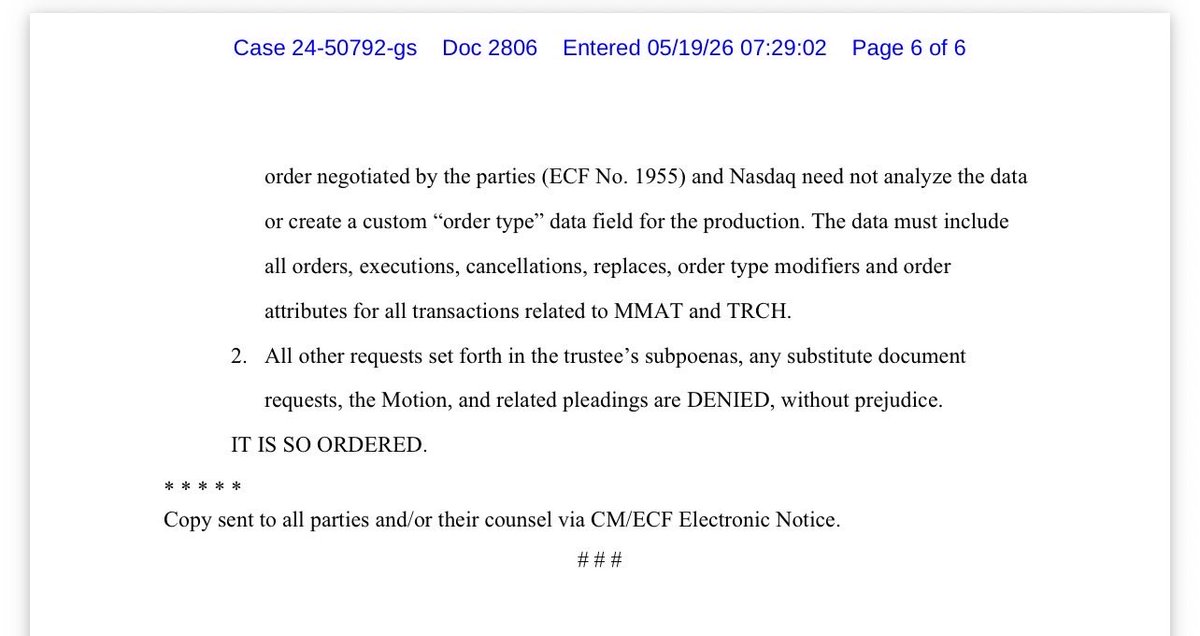

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

@TheTrndisuFrnd@ManOhWeather We’ll see what they do! Also awaiting the rulings on the remaining motions to quash.

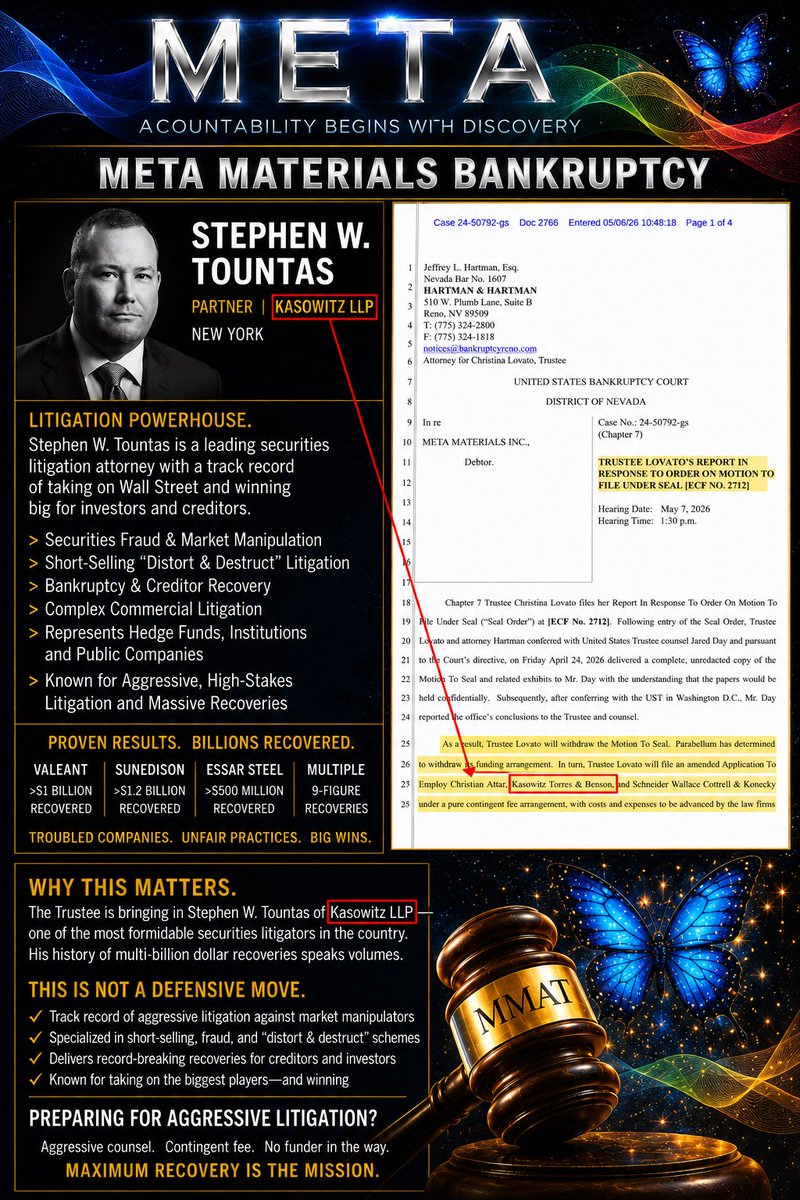

Powerhouse litigators on board who have agreed to work on contingency.

Things are getting very interesting! 🌶️

COURT DOCS DRAG ANSON FUNDS INTO THE LIGHT

Wall Street didn’t just break the rules with #MMTLP, they exposed the entire rigged system.

Anson Funds is now being dragged into court under oath… and why?

Because reports show MILLIONS of phantom shares aka naked shorts that were never borrowed, never delivered, and never supposed to exist.

Meanwhile Rretail investors followed the rules.

They bought shares.

They held positions.

And then the system (FINRA) hit the kill switch.

Trading halted.

Positions frozen.

Truth buried.

Meanwhile, hedge funds allegedly played a different game, selling what they didn’t own, flooding the market with synthetic supply, and crushing real investors under counterfeit pressure.

This is what financial fraud looks like.

Even more damning?

Regulators had warnings.

Data trails exist , CAT systems, DTCC records, settlement failures.

And yet… silence.

Or worse, as emails between the SEC and Wall Street would prove, protection.

Anson already settled with the SEC over undisclosed short-selling relationships. Now they’re being forced to explain their MMTLP exposure under oath.

This isn’t just one hedge fund.

This is a systemic operation:

• Phantom shares

• Coordinated short attacks

• Media influence

• Regulatory failure

The American market is supposed to be the gold standard. (What a crock of shit that is)

Instead, it’s looking like a rigged casino where insiders print shares out of thin air and call it “liquidity.”

(Sounds like the Federal Reserve, doesn’t it?)

MMTLP isn’t over.

It’s the thread that unravels everything.

And WHEN the truth comes out , it won’t just be Anson on trial.

It’ll be the entire system.

#MMTLP #NakedShorting #MarketFraud #WallStreet

@stockmannnbroo

President Trump,

FINRA and the SEC are moving to allow deletion of CAT data older than three years. This is not routine. This risks erasing critical evidence of market manipulation, naked shorting, and systemic fraud.

At the very moment Americans are demanding transparency, regulators are preparing to shrink the window of accountability.

You have the authority to act.

Sign this Executive Order. Enforce strict T+1 settlement. Criminalize naked shorting. Hold all participants accountable. Preserve all CAT data.

This is about protecting the financial future of every American and restoring trust in our markets.

Do not let the evidence disappear.

Please sign the order.

@realDonaldTrump #MMTLP #GME #AMC #DJT

@KurtOlsen_USA@LegalBrains@RealTheoWold

EXECUTIVE ORDER (proposed)

Strengthening Securities Settlement Integrity, Reforming Regulation SHO, and Combating Fraudulent Market Practices

By the authority vested in me as President by the Constitution and the laws of the United States of America, including the Securities Exchange Act of 1934, 15 U.S.C. 78a et seq., the Securities Act of 1933, 15 U.S.C. 77a et seq., and 3 U.S.C. 301, it is hereby ordered:

Section 1. Purpose

The integrity, transparency, and lawful operation of the United States securities markets are essential to the national economy, the protection of investors, and the preservation of public trust.

Abusive trading practices, including persistent failures to deliver, manipulative short selling practices, and the creation or circulation of securities interests not backed by valid issuance, undermine market stability and may violate federal law.

This Order directs strengthened enforcement of existing law and mandates regulatory reform to eliminate systemic settlement failures and unlawful short selling practices.

Section 2. Policy

It is the policy of the United States to:

(a) Ensure strict compliance with lawful securities settlement requirements

(b) Eliminate persistent failures to deliver and abusive short selling practices

(c) Prevent manipulative or deceptive conduct prohibited under Sections 9 and 10(b) of the Securities Exchange Act and Rule 10b-5

(d) Promote fair, orderly, and efficient markets pursuant to Section 15(c)

(e) Protect investors and strengthen confidence in United States capital markets

(f) Encourage reporting of violations through whistleblower protections under 15 U.S.C. 78u-6

Section 3. Enforcement of Settlement Requirements

(a) The Securities and Exchange Commission shall, pursuant to its authority under Section 17A of the Securities Exchange Act, ensure strict enforcement of the T plus 1 settlement cycle.

(b) Clearing agencies, broker dealers, and market participants shall be required to implement systems reasonably designed to prevent failures to deliver.

(c) The Commission shall require enhanced, standardized, and public reporting of settlement failures and close out activity.

Section 4. Reform and Strengthening of Regulation SHO

(a) Within 90 days of this Order, the Securities and Exchange Commission shall propose and, as appropriate, adopt amendments to Regulation SHO to strengthen enforcement and eliminate systemic abuse.

(b) Such amendments shall, to the fullest extent permitted by law, include:

1.Mandatory Pre Borrow Requirement

Require that, prior to effecting any short sale, a broker dealer must obtain and document a confirmed borrow of the security, eliminating reliance solely on locate arrangements where such reliance contributes to settlement failures.

2.Accelerated Close Out Requirements

Require immediate or same day close out of failures to deliver for all equity securities, including threshold and non threshold securities, and eliminate extended close out timelines that permit repeated failures.

3.Prohibition on Reset Transactions

Prohibit the use of options, swaps, or other derivative or structured transactions designed to evade close out requirements or mask failures to deliver.

4.Enhanced Threshold Securities Standards

Strengthen the criteria for threshold securities and require automatic trading restrictions where persistent failures occur.

5.Real Time Transparency

Require public disclosure, on a frequent and standardized basis, of aggregate short positions, failures to deliver, and securities lending data sufficient to promote market transparency.

6.Strict Locate Enforcement

Clarify and enforce the requirement that any locate must be based on a bona fide and verifiable source of borrowable securities, with liability for false or unsupported locates.

(c) The Commission shall ensure that Regulation SHO is administered in a manner that prevents the creation of synthetic or unbacked share supply that distorts price discovery.

Section 5. Prevention of Unlawful Short Selling Practices

(a) The Securities and Exchange Commission shall take all lawful measures to prevent and prosecute violations involving:

1.Short sales conducted without a reasonable and verifiable ability to deliver

2.Schemes to evade locate or close out requirements

3.Manipulative conduct that creates artificial market supply

(b) The Department of Justice shall prioritize prosecution of willful violations of federal securities laws, including fraud, market manipulation, and conspiracy offenses under Title 18.

(c) Nothing in this Order shall be construed to create new criminal offenses, but rather to direct enforcement of existing law to the fullest extent.

Section 6. Accountability Across Market Participants

(a) Enforcement shall apply to all participants in the securities transaction chain, including executives, traders, brokers, compliance personnel, clearing agents, and operational staff.

(b) The Securities and Exchange Commission and self regulatory organizations shall strictly enforce supervisory obligations under Section 15(b)(4)(E).

(c) Individuals who knowingly or recklessly participate in violations shall be subject to existing civil and criminal penalties.

Section 7. Industry Bars and Remedial Authority

(a) The Securities and Exchange Commission shall fully utilize its authority to:

1.Suspend or revoke registrations

https://t.co/rFBYNr0u6P individuals from association with broker dealers, investment advisers, and other regulated entities

3.Impose civil penalties and disgorgement

(b) Agencies shall coordinate to ensure that individuals responsible for serious violations are removed from positions of trust in financial markets.

Section 8. Whistleblower Protection and Incentives

(a) The Securities and Exchange Commission shall enhance enforcement of whistleblower protections under 15 U.S.C. 78u-6.

(b) Individuals reporting violations shall be protected from retaliation and may receive financial awards consistent with law.

(c) Priority shall be given to information exposing systemic manipulation or widespread investor harm.

Section 9. Interagency Task Force on Market Integrity

(a) An interagency task force is hereby established, chaired by the Securities and Exchange Commission, with participation from the Department of Justice, the Department of the Treasury, and other relevant agencies.

(b) The task force shall:

1.Coordinate investigations and enforcement

2.Share intelligence and data

3.Recommend additional regulatory or legislative reforms

(c) Within 120 days, the task force shall report its findings and recommendations to the President.

Section 10. General Provisions

(a) Nothing in this Order shall impair the authority granted by law to any executive department or agency.

(b) This Order shall be implemented consistent with applicable law, including the Administrative Procedure Act.

(c) If any provision of this Order is held invalid, the remainder shall not be affected.

Section 11. Effective Date

This Order shall take effect immediately.

Section 12. Statement of National Commitment

The United States affirms that its markets must operate on truth, transparency, and accountability. The protection of investors and the preservation of fair markets are essential to the strength of the Nation and the future prosperity of its people. This Order advances those principles and reinforces confidence in the American system of free enterprise.

#MMTLP The walls are closing in on these criminals....... Only a matter of time till PAYDAY reckoning cometh ....MFs .....

Thank you @palikaras and @johnbrda for continuing to fight this WAR... 💪😎

Sound HIGH LFGGG!!!!!!!!!!!!!🔊🔊🔊🔊🔉🔊🔊🔊🔊🔊🔊🔊🔊🔊🔊

#MMTLPFIASCO #MMTLPARMY #MMAT mmat mmtlp

FINRA's counsel's reaction on the screen was really something to watch today... (at least to me)

He was visibly distressed, holding his forehead, looking devastated at times and blank at others, not facing directly the screen like everyone else, one time his head was looking down so far that you could only see his hair (hands looked like texting someone profusely), fidgeting on his seat the whole time, head turned to 9/3 o'clock... seemed to not be alone in the room looking at them, and a lot of his narration/answers were rushed... with an unnatura/reading from an AI/live screen. This demeanor is important IMO as it will make sense when i explain the turning point of the hearing...

In contrast on the Trustee side, 2 out of 3 lawyers came and left (Wes and Clay), very relaxed and very very confident, didnt push on the CAT because they got that thet came for... remember folks, they are triangulating. the TRF data plus Nasdaq plus marke makers etc etc... would you bet that the data will show exact consistency and no irregularities across multiple sources?? 🤣😂

I bet FINRA will be very unhappy after today:

Even though FINRA won on Requests 6, 7, 8, 9, at the PRELIMINARY phase, the overall ruling was a disaster for FINRA because:

❌ FINRA Lost the Big One: TRF Data

THIS was the MOST BURDENSOME request (25 MILLION items!!!

- FINRA claimed it would take weeks/months and cost hundreds of thousands

Judge said: "Produce it anyway, trustee will pay" 😂🤣 This is what FINRA REALLY cared about

❌ FINRA also Lost short interest and Reg SHO Data

These were easier but still part of the market-wide data fishing expedition FINRA wanted to STOP

❌ The Judge's tone was against FINRA

What I heard and saw today was the:

- Judge repeatedly criticizing FINRA's approach

- Judge essentially said the trustee was "reasonable" and FINRA wasn't cooperating

- Judge essentially telling FINRA to work with the trustee or face consequences.

LATEST 🚨

MMTLP CASE JUDGE SIDES WITH SHAREHOLDERS IN FIRST EVER RARE HISTORIC WIN. JUDGE IS NOW ASKING FOR THE FINRA DARK POOL EXCHANGE DATA THIS COULD BE A MAJOR WIN FOR RETAIL INVESTORS EXPOSING HOW PRIVATE EQUITY AND HEDGE-FUNDS COLLUDE AGAINST RETAIL SHAREHOLDERS.

Drumroll please... Loading my report within the hour with a FACT-based analysis on today's major court rule 2004 decisions and what was the key turning point in my opinion... stand by.

After over a year by FINRA and others playing hide and seek shamelessly with the a United States Trustee, their time is finally up. #MMAT #MMTLP #Discovery #Rule2004