#tin

Tin is the 49th most abundant element within the Earth and has the chemical symbol Sn, which is derived from the Latin word “Stannum”. Crustal abundance is only 2 parts per million (“ppm”) compared with 75 ppm for zinc, 50 ppm for copper, and 14 ppm for lead.

I have waited 3 years or more for this. #Agnico to become 32.5% shareholder. The Gold Line Belt and Barsele is now all inside a single company.

Tier 1 asset. Tier 1 jurisdiction. Tier 1 backers. Tier 1 management. Tier 1 Agnico as biggest shareholder. 5-10+ Moz camp. 5 Moz ought to be easy peasy.

DYODD I'm super long. $GSKR.V

With the $FNM.V / $FNMCF + $MFL merger set to close early next week, I'm reviewing my notes, refreshing my perspective, and reflecting on where I see opportunity.

While I'm biased (this is my biggest position, after all), and in spite of First Nordic's underperformance this year, I'm incredibly bullish for '26.

I've structured my thoughts as follows:

- New Management

- Location

- Development Targets

- Drill Targets

- Cash Position

- Barselle

+----------------------+

| New Management |

+----------------------+

With the merger comes new management; Russell Bradford is taking the CEO role, leading the transition from explorer to developer.

Russell has a 35 year career building mines:

- In the 90's he worked in operational and project development roles at Anglo American, notably as project metallurgist and concentrator manager at BCL in Botswana.

- In the 2000's he was General Manager and COO at LionOre, where he helped scale operations leading to a $6.8B buyout.

- From 2008 to 2012 he was CEO and General Manager Mantra resources, exiting with a $1.1B sale to Norilk Nickel in 2012.

- From 2016-2019 he served as Project Director and Sr Vice President at Asanko Gold, now Galiano Gold, He oversaw feasibility studies, construction, and expansion. Still in operation generating 100k oz/year.

He's run this playbook before, and he's bringing the team he's run it with.

Russel highlights his history with Peter Breese who is also joining the new org; they worked on LionOre, Mantra, and Asenco together.

Joining the board is Darren Morcombe, former CEO / Exec Chairman of Foran Mining ($2B val), deep involvement in Southern Cross ($2B val).

Importantly, Adam Cegelski (@AdamRCegielski) is staying on. He's been involved since the Barselle Mineral days, and provides deep project expertise.

"We've got all the team behind us. The engineers, the consultants, people we've worked with over 25 years. It's the A team. That's why we've come on board. We're going to develop this. We're in development now, we're not exploring." Russell is replacing management, bringing his experienced development team to execute.

These guys know how to build a mine.

+------------+

| Location |

+------------+

The combined entity hosts deposits in the Gold Line Belt, Sweden, and the Oijarvi belt, Finland.

The Fraiser institute's annual survey '24 ranked Sweden #1 and Finland #6 globally for mining.

Both locations host excellent infrastructure: roads, rail, and power all run alongside and into the prospective mine sites. The region is powered by hydro and nuclear; power runs at $0.03/kWh. Drilling cost $250/m.

Russell described it as "the most unremote place he's been in [his] life".

+-------------------------+

| Development Targets |

+-------------------------+

The two immediate targets are Barselle and Rajapalot.

Barselle hosts 2.4M oz and is Sweden's largest undeveloped gold deposit. It's jointly owned with Agnico Eagle in a 45/55 split (Agnico majority). 175k meters of drilling has gone into the deposit, and it remains open at depth and along strike. Notably, the 2.4M oz was defined at $1300 gold. At $3000 gold, there's a lot more economic metal.

The presumptive pit runs at 1.8g/t and underground 2.5g/t, again calculated at $1300 gold. In a recent interview Russell outlined his thinking (he didn't want to provide exact numbers on their internal models). He envisioned a 2.5M ton mill, and at 1.8g/t that would spit out around 160k oz Au per year.

Russell highlighted that when you model at $1800 to $2500 gold, it becomes even more attractive - less waste, more ounces.

"With our experience and our team, that is a mine. Without a doubt that is a gold mine."

Russell plans to put another 60k meters of drilling into Barselle in 2026.

Rajapalot in Finland is 100% owned and currently hosts 1M oz at $1700 gold spread across 4 deposits.

Mineralization starts a measly 5 meters below surface. The Rompas Trend boasts the best drill hole in Finland, 6m at 617 G/t Au from 7M including 1 meter at 3,540 g/t Au.

Russell again asserts "that is a mine, without a doubt."

Russell stated plans to drill 15k meters at Rajapalot in 2026.

+---------------+

| Drill Targets |

+---------------+

First Nordic spent 2025 exploring the Gold Line belt, identifying a host of multi-km soil anomalies, receiving encouraging ToB/BoT results, and putting drill meters into the Aida (10k meters) and Nippas (5k) targets.

Note that excepting Barselle, owned jointly with Agnico, First Nordic / NordCo owns 100% of the rest of the belt.

Of the exploration activities, we've received the soil analysis, ToB/BoT, and half of the Aida drill assays. We were waiting on the edge of our chairs for the second half of the Aida drills, and the entirety of the Nippas drills, when the merger announcement quiesced news flow.

Here's highlights from the first batch of Aida drills (14/39):

- Multiple strong gold intercepts returned, including: 1.94 g/t Au over 21.5 m (2025-AID-038), 5.45 g/t Au over 4.6 m (2025-AID-030), and 1.17 g/t Au over 17.5 m (2025-AID-027)

- Gold-mineralized strike of Aida corridor extended from 0.5 km to over 2.1 km, remaining open in all directions

- Several new gold bearing structures identified, including the blind to surface Pharao Zone and the Northern Mafic Zone

- Gold bearing structures intercepted in 12 of 14 drill holes to date with visible gold identified in 5 drill holes

Once the merger closes and news flow resumes, I expect we'll get both sets of results *and* a statement from management about followup drilling.

To add more color to Aida, the best to date are:

- 2.46 g/t Au over 22m from 45m

- 1.94 g/t Au over 21.5m from 65m

- 2.44 g/t Au over 14.55m from 142m

- 5.45 g/t over 4.6m from 170m

As Aida gets more drilling, expanding the footprint and defining the geometry, I expect it will eventually reach the threshold of "this is a mine". This is doubly true in a hub-and-spoke with Barselle, where the shared capex materially reduces the threshold for mineability.

+-----------------+

| Cash Position |

+-----------------+

In conjunction with the merger announcement the team came to the market with a $30M raise.

It was filled within a day, with commitments of over $90m.

So they raised another $50M two days later, also oversubscribed.

Note that Taj, the former CEO, put in $1M of his own cash on his way out the door.

So in a week they raised $80M. Adding the cash balance of First Nordic, and warrants sitting in-the-money, Russell has a war chest of $100M with which to drive development, drilling, and other priorities.

Note this $100M of cash represents about 40% of the combined entity's market cap.

+------------+

| Barselle? |

+------------+

One of the major hangups on First Nordic has been their minority interest in their flagship deposit, Barselle.

While the other targets are promising, and have every indication of being economic deposits, there's still legitimate concerns around execution, exploration cost, and time.

In prior years, management has tried to work out a deal with Agnico to consolidate ownership of Barselle. So far, every attempt has fallen through. Earlier in '25, Taj and Adam spoke optimistically regarding a new deal, so we know there continues to be productive discussion.

With the merger complete, cash in the bank, 60k meters of drill plans, and an experienced development team leading the project, we've never been in a better position to negotiate.

Unlocking Barselle would be a huge step in realizing the total value of First Noridc / NordCo.

But what's great about the current setup is that Rajapalot provides a clear and 100% owned development target.

We can look forward to material progress irrespective of Agnico's timeline, and while development is ongoing we can continue to define Aida, Nippas, and others in preparation for a district scale opportunity in Sweden.

+---------------+

| Conclusion |

+---------------+

All in all, First Nordic, now NordCo, is in an exciting position.

It's under experienced management, has a new 100% owned development target, a backlog of material news, at least 75k meters of drilling in '26, and $100M of cash with which to execute.

Stack on top a hot metals market, the fact that thus far FNM has avoided popular attention, and a catalyst-rich 2026... and we're primed and ready for material price discovery.

@rekurencja@TinFormer_News ”Gaining proper access to the site required a 38 Kilometre road be built. This was achieved by recruiting 600 locals who built this road through dense jungle – a truly extraordinary endeavour.”

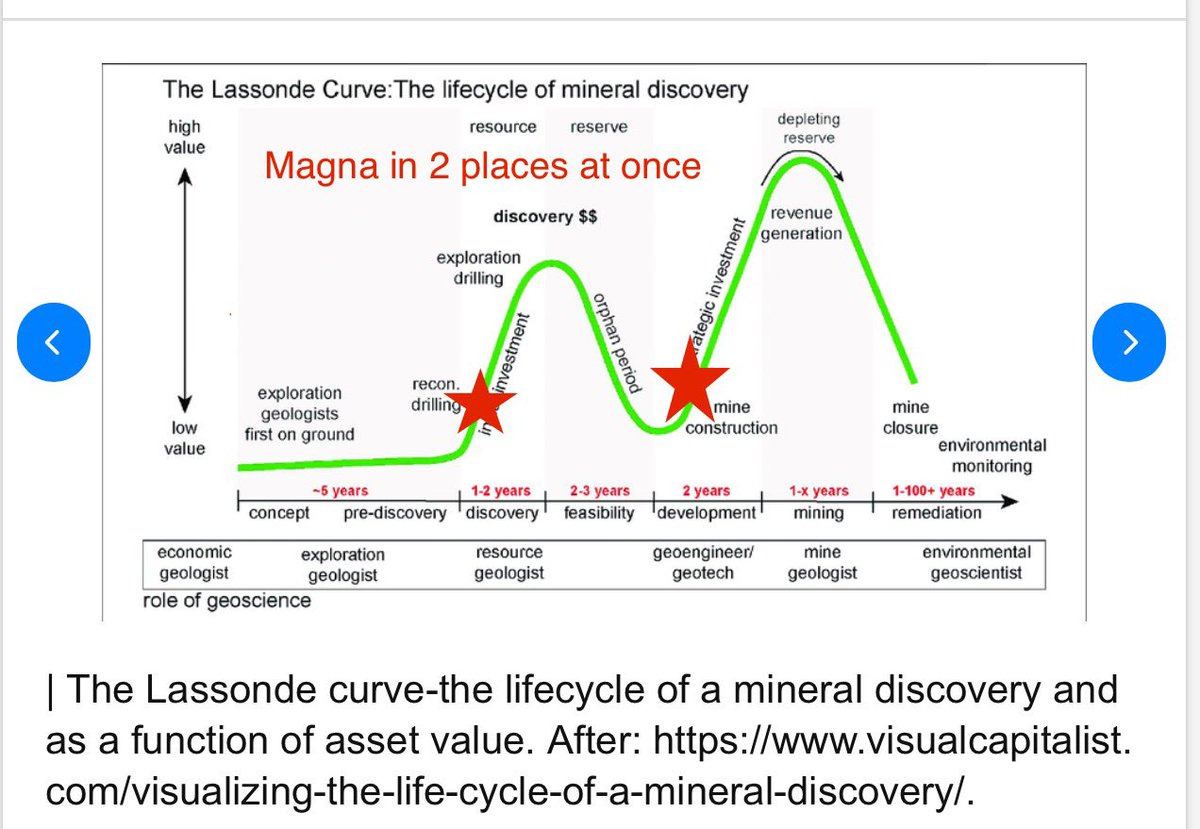

.@MagnaMining $nicu.v $mgmnf

Magna is a rare breed existing at the beginning of curve exploration drilling and discovery: Stumpy Bay Area copper discovery hole and coming step outs, other target in area, footwall drilling Crean Hill, McCreedy, Levack, other properties….

And concurrently on the Second upslope of curve McCreedy production ramp, Crean Hill development into production, Levack and Podolsky restarts…. Then add whatever discoveries and Shakespeare added to production profile… well over a decade of growth in the pipeline.

It’s the “quark effect”

-This phenomenon implies that a quark can exhibit properties consistent with being “in two places at once”

Trust the process. Everything is in place for Magna to grow into a multi-billion dollar company. And that growth will be directing reflected in the share price because of the internally generated cash flow as opposed to The destructive path of constant dilution Most developers undertake.

this is a unicorn once in a generation type of company Because it has every piece of the puzzle needed for a supercharged success:

we have a top team that has done it before with these assets in this jurisdiction these guys and gals literally were part of Fnx,

You have exceptional grade and scale of tonnage and metallurgy that supports high returns.

You have tremendous infrastructure already in place which Insurance extremely low cost to bring these mines back into production that are on care and maintenance.

You have developing discoveries, one of which when proved could add hundreds of millions of dollars to the market cap.

You have a management that is directly aligned with shareholders as they are large owners of the stock and actually live where the mines are and will be producing.

The timing of the depletion of other assets in Sudbury couldn’t be better, giving us a competitive advantage in negotiating ore selling agreements and toll milling arrangements at historically low levels.

The hardest thing for most investors to do is to do nothing, victory is a slow walk it comes from the passage of time passively doing nothing except allowing the company the time it needs to execute, which in this case is a relative the short time.

We have leapfrog the lassonde curve And actually we exist at two places on the curve at once, we’re on the up slope of a developer rerate going into production and then another rerate that comes from being a producer, at the same time like a quark we’re also back on the upswing of the discovery curve having multiple potential discovery Coming our way a couple of which we will know about before year end should they be successful.

Those Shakespeare is not our focus at the moment. Should this new copper discovery prove to carry the tons needed to be satellite deposit those grades super charges the IRR Npv for Shakespeare and pretty much will ensure the mill being built at some point which is a low cap cost operation

And then we could be producing our own and selling or upwards towards 10,000 tons a day and all this accomplished by internally generated cash flow and some project financing for Shakespeare meaning no dilution to the equity and we shareholders enjoy the growth of share price.