BofA: Global Memory

> Super-Cycle Intact: The BofA memory indicator remains near record highs (reaching 183 in May, well above past peaks of 120–130). High-end memory demand (HBM4, SOCAMM, etc.) continues to drive exceptional strength.

> Massive Revenue Growth Forecasted for 2026: Global DRAM revenue is expected to nearly quadruple (+325% YoY) in 2026, primarily driven by a sharp rebound in Average Selling Prices (ASPs). NAND revenue is similarly projected to jump nearly fourfold (+299% YoY) in 2026.

> Servers & AI Dominating DRAM: Servers—especially AI systems utilizing High Bandwidth Memory (HBM)—now account for over half of total global DRAM demand due to high memory density per system.

> SSDs Fueling NAND: Enterprise and data center Solid State Drives (SSDs) utilized in AI applications now make up more than 50% of total NAND demand and sales, commanding a price premium over standard IT applications.

> Sizable Share of AI Hardware Budgets: High-bandwidth memory (HBM) and advanced data center memory now command a massive 35% to 40% of total cloud AI infrastructure spending. Big Tech's cloud and AI capex is projected to push close to $1.5 trillion by 2027.

> HBM Supply Cannibalization: Producing an HBM chip requires 3x to 4x more silicon wafer capacity than traditional DRAM. Because they share the same production lines, manufacturers are prioritizing high-margin HBM, starving the market of standard capacity.

> DDR5 Premium Disappears: The rapid exit of tier-one manufacturers from mature products has triggered a severe, structural shortage in legacy DDR4. BofA notes that spot prices for 16Gb DDR4 and DDR5 have essentially converged into the $35–$40 range. The traditional technology premium of DDR5 over DDR4 has largely vanished because manufacturers are dropping DDR4 production faster than PC and server customers can physically transition their setups.

Massive Revenue Surge Forecasts (2026E)

> Total Market Expansion: Combined DRAM and NAND revenue is projected to nearly quadruple to $891.8 billion in 2026E (up from $214.8 billion in 2025).

> DRAM Performance: DRAM revenue alone is expected to increase by +325% YoY to $568.8 billion in 2026E. This hyper-growth is heavily back-loaded, with quarterly revenue ramping up aggressively from $83.9 billion in 1Q26E to $182.6 billion by 4Q26E.

> NAND Performance: NAND revenue is forecast to surge +299% YoY to $323.1 billion in 2026E, climbing from $45.3 billion in 1Q26E up to $102.4 billion in 4Q26E.

High-Bandwidth Memory (HBM) Deep Dive

> TAM Scaling: The Total Addressable Market (TAM) for HBM is projected to hit $76.8 billion in 2026E (+122% YoY) and skyrocket to $134.6 billion by 2027E.

> Astounding Profitability: The industry average Operating Profit Margin (OPM) for HBM is sitting near a massive 49% for 2026E, climbing even higher to 54% in 2027E.

The Technology Shift (HBM Mix):

2026E: Mainstream volume is dominated by HBM3e (60%) and HBM4 (32%).

2027E: The mix flips heavily into HBM4 (64%), while the next-gen HBM4e begins its entry at 19%.

2028E–2030E: The long-term horizon shows rapid transition into HBM5+, which is expected to command 79% of the market mix by 2030E.

> Server Intensity: AI+HBM server units are scaling to 4.5 million systems in 2026E, with memory intensity per server jumping to 1,413 GB per AI server.

Pricing (ASP) & Shipment Dynamics

> The Rebound Driver: The entire super-cycle is pricing-driven. Blended DRAM Average Selling Prices (ASPs) are modeling a +249% YoY expansion in 2026E ($13.0 per 8Gb equiv. unit vs. $3.7 in 2025). Blended NAND ASPs are modeling a +238% YoY increase.

> Quarterly Pricing Velocity: The fastest pricing momentum occurs in the first half of the year, with DRAM ASP growth showing a massive +73% QoQ spike in 1Q26E and +53% QoQ in 2Q26E, before cooling down to normal levels (+21% in 3Q, +7% in 4Q).

Capex & Capacity Expansions

> Massive Investment Outlays: Total industry Capex spending (DRAM + NAND) is projected to jump +62% YoY to $118.7 billion in 2026E.

> DRAM vs. NAND Split: Manufacturers are funneling the vast majority of cash into DRAM, ramping DRAM capex by +65% YoY to $88.6 billion. NAND capex is expanding much more modestly at +55% to $30.1 billion.

> Wafer Capacity: Total DRAM wafer capacity is expanding to 2,066k wafers per month in 2026E, out of which 23% of all global DRAM wafer capacity is being swallowed up solely by HBM production.

$MU $SNDK

$MU vs. $SKHY on fundamentals:

$SKHY will report Q2 earnings on July 23, so these numbers are currently skewed in favor of $MU, which has already reported Q2.

$SKHY’s fundamentals will likely improve materially across all key metrics in Q2.

🚨🚢 Iran has declared the Strait of Hormuz closed "until further notice." The AIS tape shows the flow was already collapsing before the announcement.

Latest 24h commercial crossings: 11 total — 8 tankers / 3 dry cargo. Down from 12 yesterday, a fraction of the 57 at the June 24 rebound high, and only ~10% of the Jan–Feb run-rate.

Two versions of the same incident: Iran's navy says it fired a warning shot at a vessel on an "unapproved route" and will bar all transit until the end of US "interference." CENTCOM says the IRGC attacked M/V GFS Galaxy — a Cyprus-flagged container ship — leaving a civilian crewman missing and the vessel ablaze, then launched a third round of strikes on Iran at 7:15pm ET Saturday.

The closure landed hours after inconclusive Iran–Oman talks on safe passage, with Oman floating a plan to jointly run the strait for transit tolls. Diplomacy didn't buy flow. It bought a warning shot.

ICE Brent settled near $76 Friday, up ~5% on the week — the risk premium is returning. Those futures are dark for the weekend, but the 24/7 tape isn't: Brent is up ~3% over the past 6 hours on Hyperliquid, pricing the closure in real time and previewing the gap into Monday's open.

Powered by our commercial crossing index — AIS refreshed every 30 mins. Major real-time chokepoint trackers available on @TheTerminal.

The Q2 earnings season (referred to as Q2 as this is when firms report Q2 results) kicks off on Tuesday the 14th when we'll hear from $JPM, $BAC, $GS, $WFC, $C and more. Things ramp up quickly with the busiest week slated for the start of August. Who are you keeping an eye on this quarter? Watch for: $AAPL, $MSFT, $TSM, $GOOGL, $TSLA, $MA, $V, $NFLX, $ARM and many more. Data as of July 9, 2026, $AMZN, $META, and $WDC are currently unconfirmed. #stockmarket #earnings #investing #trading #stocks

The United States 🇺🇸, Japan 🇯🇵, and South Korea 🇰🇷 just signed a new pact around working together to accelerate

Small Modular Nuclear Reactor Development

America is running out of places to gather:

Bars and clubs per capita have fallen over 60% since the late 1970s, and since 2001 a fifth of movie theaters have shut their doors.

Over the past two decades, the country has lost roughly 2,000 golf courses and 7,000 bars and nightclubs.

Catching live music now costs a pretty penny: top-tour concert tickets averaged $134 last year, up +42% from 2019.

So Americans stay in. Nearly 80% see friends and family less than three times a week.

Read that again.

America has traded their community for their couch.

10 repositorios de GitHub para scrapear todo internet

Guárdalos todos. Cada uno extrae datos limpios de cualquier web. Ese nivel de acceso normalmente exige llamadas de ventas y contratos.

J.P. Morgan: Eye on the Market

> Hyperscalers developing their own in-house silicon are seeing 30% to 40% reductions in Total Cost of Ownership (TCO) compared to using merchant GPU fleets.

> Specifically, Amazon $AMZN claims its AWS Trainium3 UltraServers deliver 30% lower TCO (at FP8 precision) than NVIDIA’s $NVDA GB300 NVL72 systems.

> Anthropic has committed to running its Claude models on AWS Trainium for the next ten years. This serves as the most powerful third-party endorsement of ASICs to date.

> Driven by this rise in custom silicon, NVIDIA’s dominant share of AI accelerator revenue is experiencing a gradual decline, dropping from 85% in 2023 to an estimated 75% in 2026.

> Total tokens per day are skyrocketing toward 10 Quad by 2030, with inference taking up an increasingly dominant share of AI compute over training. This shift heavily incentivizes cost-optimized custom silicon.

> As of June 2026, Anthropic has committed to roughly 10.8 GW of compute (heavily utilizing AWS and Google/Broadcom ASICs), driving billions of dollars into Amazon and Google's revenue backlogs.

> US might be 30%-35% self-sufficient in advance node production by the end of the decade.

🚨 The BIS has just reminded us that AI is probably a major economic revolution but the current investment boom is also starting to become a source of financial fragility.

➡️ We should not confuse AI’s technological potential with the immediate financial profitability of every investment made in the name of AI. AI can generate significant productivity gains but turning these task-level gains into a lasting increase in productivity across the whole economy is much more complicated. Companies need to redesign processes, train teams, integrate tools, adapt systems and rethink business models. Historically, this kind of transformation takes time.

📊 The problem is that the market is already pricing in an almost perfect scenario with rapid adoption, massive productivity gains, high margins and sustained earnings growth. It is possible but not guaranteed. AI may well be a real revolution but that does not mean every investment being made today will be profitable, nor that all current valuations are justified.

📚 The major hyperscalers are investing enormous amounts in data centers, semiconductors, energy, cloud infrastructure and computing power. However, this race is also defensive as everyone is investing aggressively out of fear of missing the wave. Individually, that is rational but collectively it can create overcapacity. A classic pattern in major technological revolutions where a technology can be revolutionary while capital can still be misallocated.

⚠️ The BIS also highlights the opaque financing of the entire AI ecosystem with cross-shareholdings, long-term contracts, data centers built by third parties and leased back to tech giants, private debt, off-balance-sheet commitments, and so on. If the investment cycle slows abruptly, the shock will not only affect a few technology stocks, but it could spread to suppliers, data center developers, utilities, private credit funds and, more broadly, financial conditions.

*Link: https://t.co/1YeEQ0uChH

AI is reshaping how institutional investors work:

~52% of institutional investors now primarily use AI for research, according to a Barclays survey of 410 fixed-income investors.

This is followed by hedge funds, at ~44%, which primarily use AI to process and analyze large volumes of market data.

By comparison, ~27% of hedge funds use AI for modelling and risk analysis, versus ~22% of long-only managers and ~17% of asset owners.

Operations, compliance and reporting, and investment decisions each account for just 10% to 15% across these groups.

AI is changing how investment decisions are made.

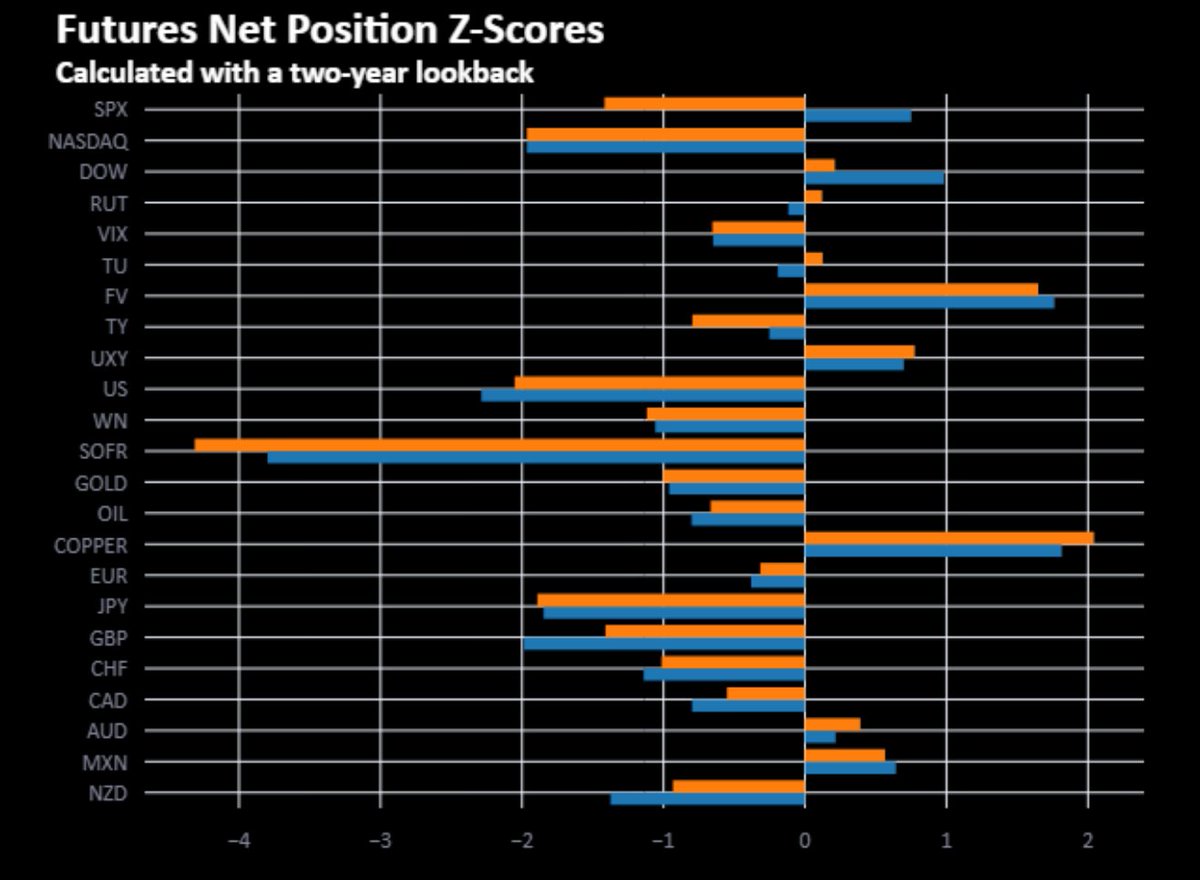

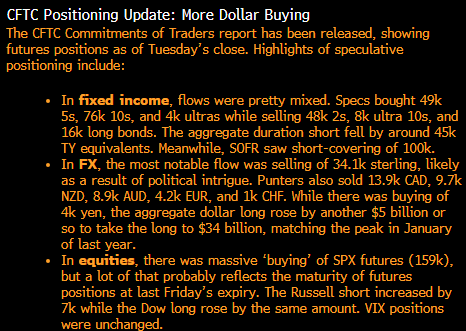

Extreme positioning from COTs data... its a very helpful tool of telling you what happened, however very little signal looking at the present or future