HFM, formerly known as HotForex, is an award winning multi asset broker, providing trading services and facilities to both retail and institutional clients.

A number of headwinds continued to pressure sentiment

#FOMC's higher-for-longer stance

#JPMorgan's Dimon noted the potential for a 7% rate as a worst case scenario.

The threat of a US government #shutdown this weekend

#Moody's warning

#Technicals have played a part as well!

The chance of the #BoE raising rates past 5.5% falls to below 20% from around 42% on Tuesday - #Swaps

Traders price a 70% chance of a BoE hike Thursday vs 90% earlier.

BEFORE THE EU OPEN

* #PBoC leaves rates unchanged, says has ample policy room as analysts bet on future rate cuts

* #Japanese Trade Deficit falls by 2/3 y/y as Imports tumble (-17.8%)

* #Yield on 2Y, 5Y, 10Y US push to new multi-year highs hours before the September Fed meeting

* #XAU cannot breach its 200d MA, $1930 now.

* Tonight #FED will stay on hold (99% odds) but Dot Plot, Quarterly economic update will be key

LATER TODAY: DE PPI, US Mortgage applications, EIA Oil Stocks Change, FED INTEREST RATE DECISION, FOMC PROJECTIONS, PRESS CONFERENCE

*CUTS #Eurozone growth forecast to 0.6% in 2023 (0.9% previously) and to 1.1% in 2024 (1.5% previously).

*RAISES #Japanese growth forecast to 1.8% in 2023 (1.3% previously), trims 2024 to 1.0% (1.1% previously).

#OECD

*RAISES #US growth forecast to 2.2% in 2023 (1.6% previously) and to 1.3% in 2024 (1.0% previously).

*CUTS #Chinese growth forecast to 5.1% in 2023 (5.4% previously) and 4.6% in 2024 (5.1% previously). 1/2

into the economy, despite a ''too high inflation''. #AUD little changed, #USD strengthening vs #EUR, #GBP (+0.15%).

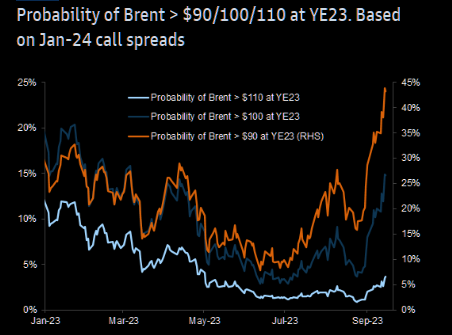

* #Oil keeps pushing its 10m highs

* #GS thinks Fed is done, despite Dot Plot

LATER TODAY: EU HICP, Core HICP, US Housing Starts, Cad CPI

BEFORE THE EU OPEN

* Significant divergence between EU and US indices yesterday, with #Dax, #Cac down >1% while #US ended the day flat.

* #APAC is down this morning, led by #Nikkei. Futures fractionally negative (-0.1%/-0.2%) 1/3

* #Energy, #Tech have been the best performers yesterday: the former one is widening its outperformance over #SP500 in the last 3 months (+14.92% vs +1%).

* #SocGen felt 12% on cutting costs plan

* #RBA minutes show officials want to give time to tightening to flow .. 2/3

MIDDAY UPDATE

*#SNB to raise key policy rate 25 BPS to 2% on September 21st, according to 30 of 37 economists. 7 said no change.

*#Bundesbank monthly report: We expect the German economy to shrink in Q3 on weak industry and muted private consumption. 1/3

*INTERESTING MOVER: #Gold, +0.22% @ $ 1928.09 is trading in a very tight range between its 50d and 200d MAs and close to the upper bound of a descending channel.

BEFORE THE EU OPEN

* US Futures are fractionally positive this morning (+0.1%/+0.2%) following a lackluster session on Friday.

* A worst than expected Michigan consumer sentiment + news about the UAW strike sent #US500 - 1.22%, #US100 -1.75%, #US30 -0.83%. 1/4

* #USDX at 104.89 with some relative strength from antipodeans.

* #Crude Oil at $91.39, close to 10 months high.

* Rates close to recent highs along the curve, #XAU +0.23% @ $1928.

* LATER TODAY: Canadian Housing starts, US Net Long term TIC Flows.