A Strategy+Management consultant, I'm a seasoned $TSLA, $PLTR & $ONDS investor for the LT. AI, EVs, Drones, Energy, Robotics & Biotech are my primary interest.

🧨🚀🚨💥 $ONDS 💥🚨🚀🧨

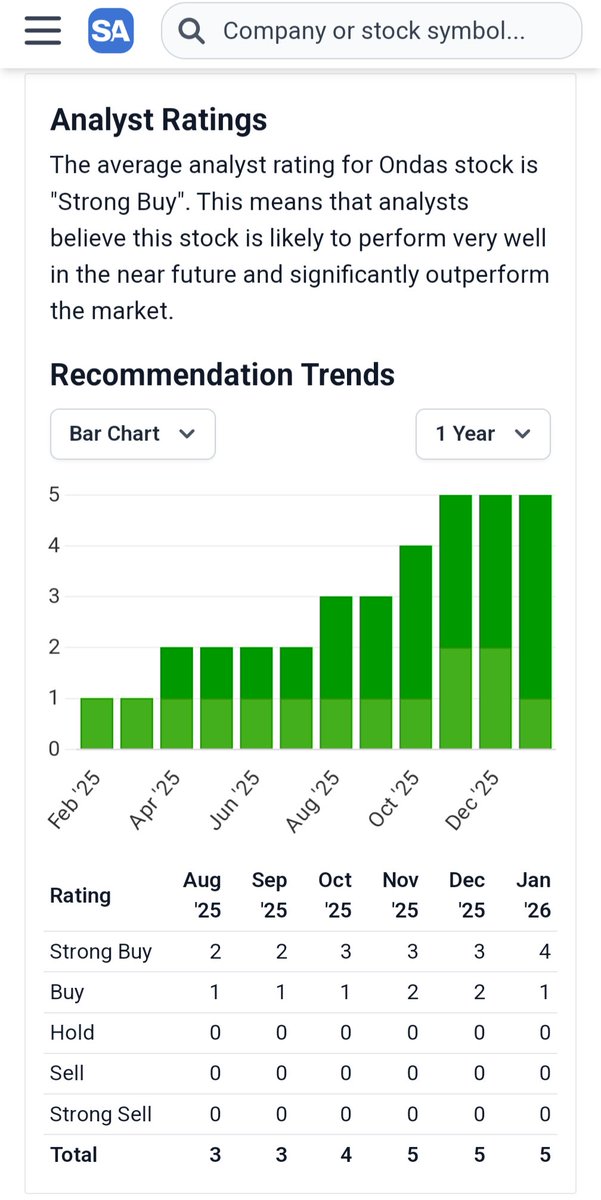

Guys, you might ignore everything else, but how the F*CK can you ignore a crazy-ass Analyst RECOMMENDATIONS TREND like this!

And guess what? This does not even include the massive state of Analyst upgrades from today!

$TSLA $PLTR $INOD $IREN $CLS $CRDO

Fully agree with Chairman on this one.

$ONDS under $8 is a gift.

Same with $IREN under $50.

But read this twice: don't buy something just because someone on X said so, me included.

I'm sharing a view, not handing you a signal.

Everyone here is voicing an opinion.

Do your own work, size your own risk, and own your own decision.

While the broader tape was getting hammered, $ONDS quietly booked over $40 million in new orders this month alone for autonomous defense systems.

That brings second-quarter order activity to more than $150 million.

I’m still holding, and I genuinely have more conviction now than I did a month ago.

This is the ONLY drone company with FAA Type Certification, sitting on $1.5 billion in cash, building both the offense and the defense side of the autonomous systems story at once. Order flow like this, in a week where everything else AI-adjacent is getting sold, is exactly the kind of divergence I look for.

People fear dilution. Right now the order book is outrunning the worry.

-BP

This is not financial advice.

$PLTR

Silence.

No headlines.

No YouTubers.

Just quiet accumulation.

You can feel it —

the wind is quietly changing direction.

Closer to the low.

Patience.

💥💥🚀

$PLTR PEG down to 1.1X.

For context, $NET, $DDOG & $CRWD are other world-class enterprise software companies with PEGs all above 3.0x.

Palantir is expected to outgrow all of them by a wide margin in the years to come. 40%+ 3-year revenue CAGR with sky-high margins is the expectation.

If those margins are sustainable, the lofty sales multiple doesn't matter & this elite company is already very attractively priced.

Considering their immensely attractive app layer value proposition, I think margin durability is a likely outcome. If they're delivering x% better customer outcomes at y% lower costs, that will justify pricing power. Their long list of customer case studies point to this being the case.

This is starting to get very interesting to me.

Palantir attractive here to you? Pouncing? Waiting for a better entry?

A very strong bull case scenario for $ONDS laid out below.

While it may sound overly optimistic, Peter is someone who’s been invested in this company for a while now and knows what he’s talking about.

Worth seeing what perfect execution might look like.

Not financial advice.

Gifts from the "efficient" stock market with Adam Smith's ever-present "invisible hand" are pretty rare!

🚨🚀🧨💥 $PLTR 💥🧨🚀🚨

right now presents one of them!

$TSLA $PLTR $ONDS $IBRX

https://t.co/ny8yenTJ2T

$ONDS The crazy part is… a year from now, you probably won’t even remember this little dip that happened on June 23, 2026.

Unless, of course, you bought it and got yourself a great deal.

Ignore the short-term noise. Keep loading your bags and focus on where the company could be 12 months from now, not 12 hours from now.

Gifts from the "efficient" stock market with Adam Smith's ever-present "invisible hand" are pretty rare!

🚨🚀🧨💥 $PLTR 💥🧨🚀🚨

right now presents one of them!

$TSLA $PLTR $ONDS $IBRX

https://t.co/iCVH1ezVCU