@Marczeller Very crazy times.

Next is how they return the funds. Do they return it to kelpDAO or could they use it to almost zero the bad debt on Arbitrum?

@0x_Abdul Arbitrum just recovered ~$70m from the rsETH hacker. It's now up to governance to release the funds.

Think they could use this to push for scenario 1? Alternatively if scenario 2 happens the funds recovered could almost zero the bad debt on Arbitrum...

The ABC Labs team is monitoring the Kelp DAO exploit carefully.

It appears very unlikely that any Reserve DTF holders will be affected.

RSR stakers on USD3 and eUSD could end up performing their function of first-loss capital to protect DTF holders in the event that Aave V3 USDC collateral ends up exposed to bad debt. This is seen as unlikely by many, but cannot yet be ruled out.

More info:

Yesterday, Kelp DAO's LayerZero bridge implementation was exploited, allowing an attacker to withdraw 116,500 rsETH, worth approximately $292 million, from the ETH L1 bridge contract, leaving their bridged rsETH tokens less than 100% collateralized.

The attacker deposited rsETH into onchain lending markets, including Aave on mainnet, and borrowed WETH. At the moment, those borrow positions are still collateralized, but the collateral is rsETH.

So the question is: will rsETH on mainnet be devalued? If so, it appears it would take a 15.5-18.5% haircut. But the attack was on the bridge, not the base protocol; the rsETH circulating on mainnet are still themselves fully backed by restaked ETH. So Kelp DAO may choose to treat the mainnet rsETH tokens as they usually would, and only subject the bridged token holders to the loss.

If rsETH on mainnet is devalued in an effort to socialize the losses across bridged and non-bridged rsETH holders, the collateral the attacker deposited on Aave would lose around 15.5-18.5% of its value, generating bad debt. There are further questions in this scenario around how Aave's backstop capital mechanisms would be deployed and whether losses would make it to lenders.

If Aave lenders took losses, this would affect the Aave V3 USDC collateral within USD3 and eUSD. However, our understanding is that the impact would be small, such that RSR overcollateralization would more than cover the loss.

According to the Aave spokesperson, rsETH on mainnet is fully backed and will not take a haircut at all. See: https://t.co/TMZf5ODnqE

If their analysis is correct, our understanding is that USD3 and eUSD bear no exposure at all.

Out of an abundance of caution, minting and rebalancing of eUSD and USD3, as well as un-staking of RSR from those two RTokens, have been temporarily paused. Redemption remains available to any who wish to redeem, but to receive the benefit of RSR's overcollateralization in the event it is needed, holders would need to continue holding.

ETH+ and bsdETH do not contain any rsETH as collateral and are not exposed.

Markets may see stress and reduced liquidity as the ecosystem reacts. We will continue to monitor for secondary impacts of the situation.

For sure, I enjoy this new update format and would be keen to contribute.

From your reply to Zeb it sounds like an update like would also help update you and the core team on governance flows.

Would you minding pinging me / message the DRF when you're starting to put the next one? I'll link we @postoripriori and we'll get something together for the next one.

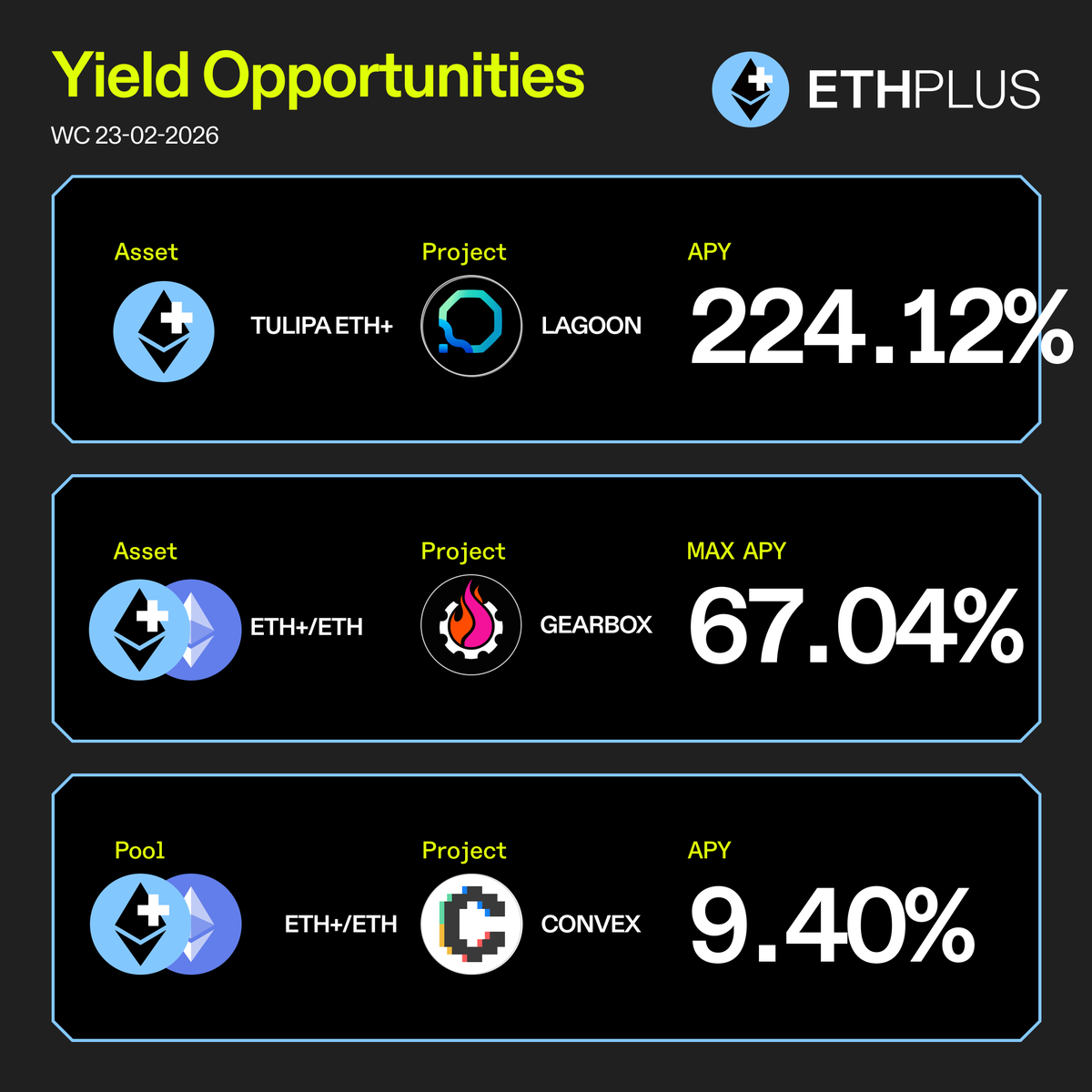

The @tulipacapital ETHplus vault on @lagoonfinance just crossed $5M TVL and is still generating ~12% APY.

A managed strategy deploying ETHplus across curated DeFi opportunities.

More in the latest Reserve News update:

https://t.co/yiA0Y9OMh0

A new $ETH yield opportunity has entered the chat.

Delta-neutral ETHplus DeFi yield with yield so high it's breaking our graphics... Live on @lagoonfinance. Curated by @tulipacapital.

Honourable mention to @GearboxProtocol with their unincentivised looped ETHplus/ETH strategy. A DeFi OG stack using @beefyfinance tech and vault curation from @kpk_io 🚀

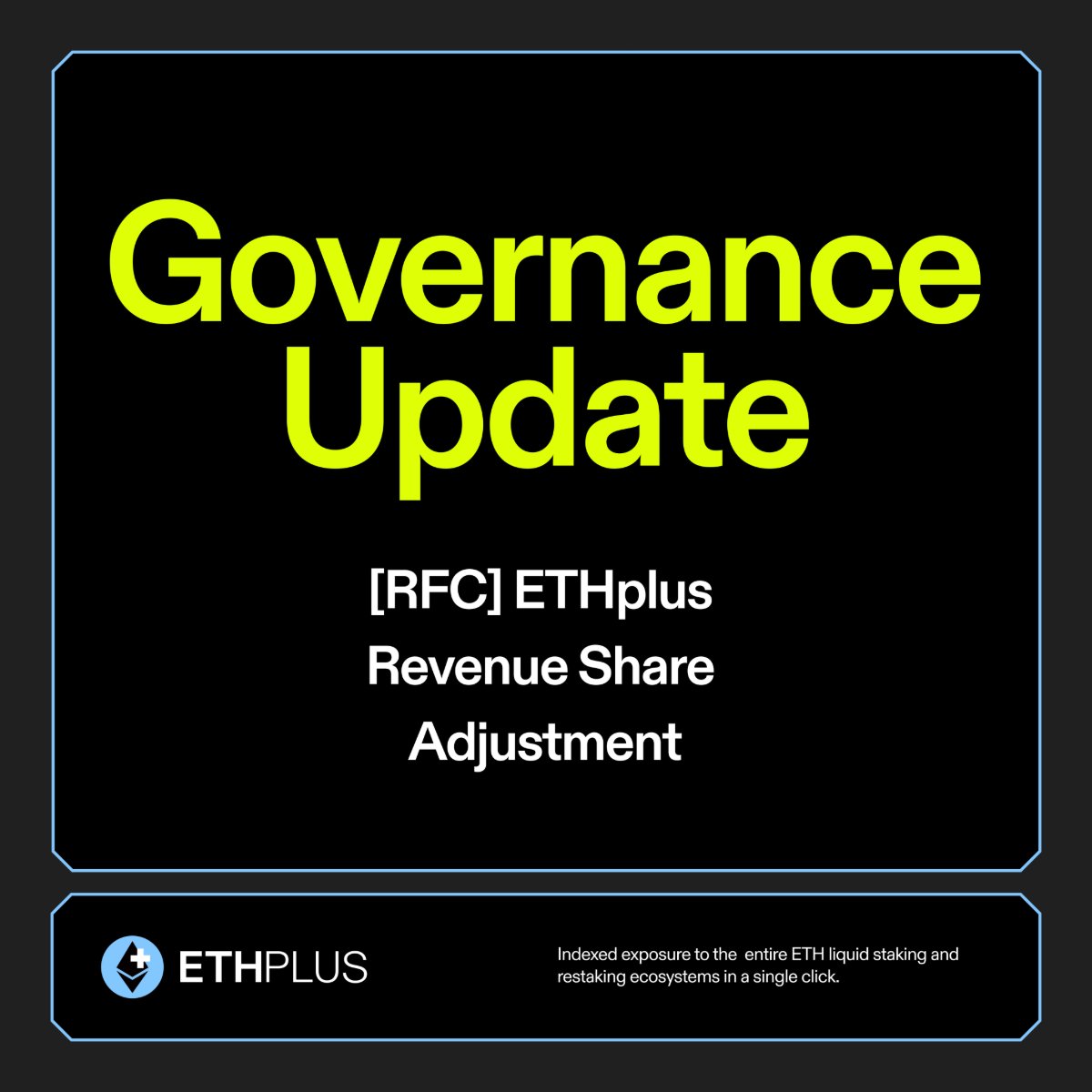

An fresh RFC has just dropped on the forum proposing an adjustment to the ETHplus revenue share model.

The proposal explores;

📈 Increasing the total take rate from 5% to 10%

📉 Decreasing the allocation to RSR stakers from 5% to 3%

🤲 Introducing a 7% protocol fee

Want to know more? 👇

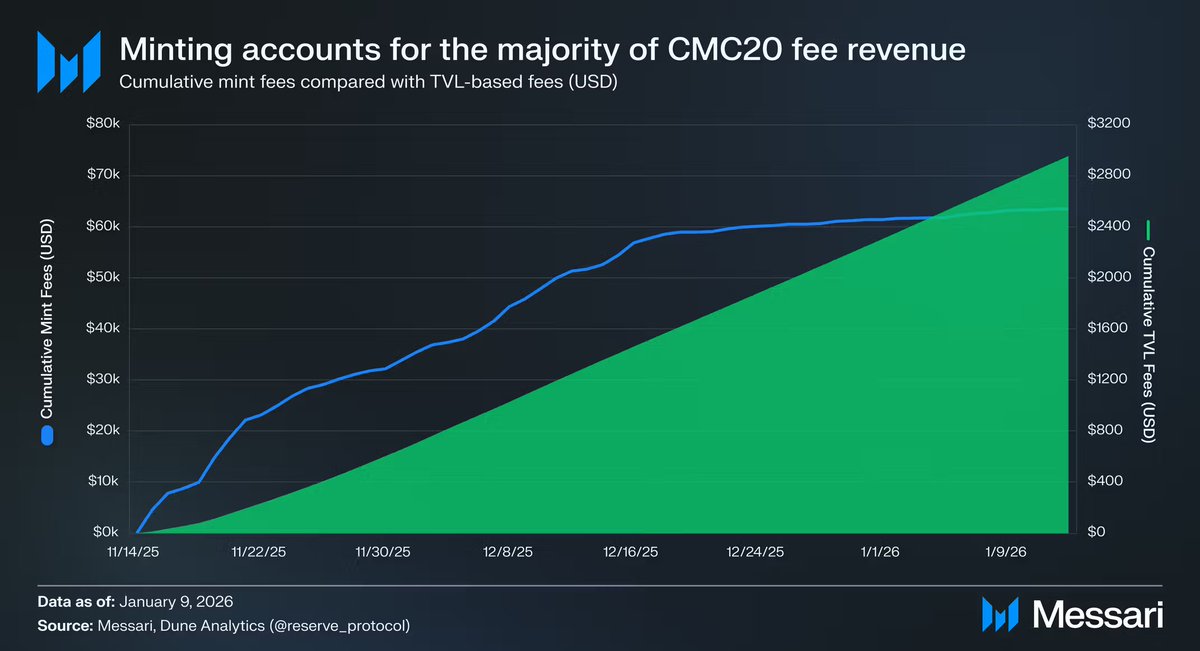

A majority of CMC20 revenue is coming from mint fees

Fees are used to:

Buyback and burn $RSR 🔥

Reward $RSR vote-lockers 🎁

If CMC20 continues to grow, it will be interesting to see at what point TVL fees catch up to mint fees

could not agree more. baby been about that life for years now. product market fit increasing on the market side (rare) as cultural tailwinds funnel users into the tech we’ve already build ( and continue to expand)…👀

Thanks for taking time to read the report. Comments like this make it worth it! :)

Not sure if you're aware but these are released every quarter so the next in the series has just dropped. Check it out below, interesting to see how the balancer hack on 10/10 is still affecting liquidity two months later.

https://t.co/7VPTF0Vlby

Just dropped a new @ETHPlus_ liquidity report, aiming to be the most comprehensive analysis of minting and redemption curves, on-chain liquidity and the liquidity of its constituent collateral assets.

Hoping that it will inform and educate the community on key metrics, guide governance decisions over the next quarter and provide assurances for institutional capital allocators that they can enter and exit large positions safely.

Check it out.

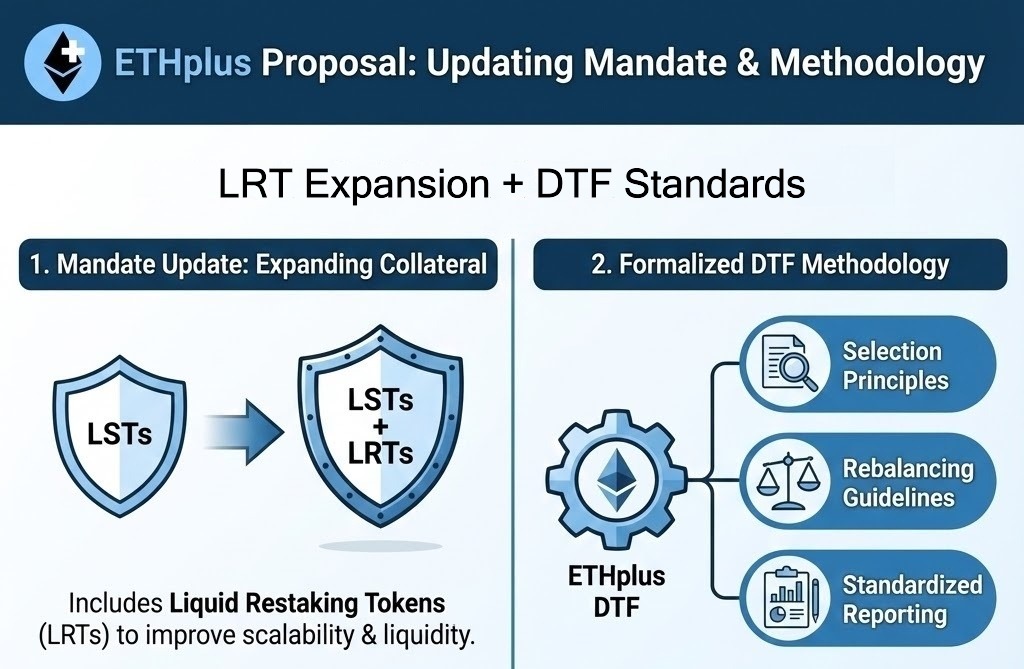

@ETHPlus_ is leveling up ⬆️

New proposal:

1⃣ Update the mandate to include select, safety-first Liquid Restaking Tokens (LRTs) for deeper liquidity + scalability.

2⃣ Codify a formal DTF methodology: eligibility + selection rules, quarterly rebalances, and standardized reporting.

ETH+ is governed by $RSR

Read the full proposal & discuss below 👇

What Founder Mode is to Under Cover Boss is exactly the same as what a Marathon is to a 100m sprint.

Undercover Boss sees senior executives work frontline roles and highlights a simple truth; truth travels faster than hierarchy.

Both discover broken processes, perverse incentives, and cultural issues that never surface in reports but where as Undercover Boss is reactive; episodic and corrective, Founder Mode is proactive; structural and continuous. The key difference is sustainability.

Seen this way, founder mode is not anti-management. It is anti-detachment. By maintaining an ongoing connection to the frontline leaders can stay close to the mess and lead from the front. Undercover Boss makes this insight emotionally obvious in an hour of television. Founder mode makes it operational as a long-term leadership philosophy.

https://t.co/s6hXPHl1Q0

![DTFgov's tweet photo. Governance Alert 📢 [REPORT] ETH+ Liquidity Analysis Q4 2025 https://t.co/FCiKhG2uwU https://t.co/zPHRrdRyzD](https://pbs.twimg.com/media/G1Djar0a4AE1S26.png)