Meta probably won't actually sign this $10 billion Anthropic deal (Save this).

Anthropic is in early talks to lease AI computing power from Meta, in a deal reportedly worth up to $10 billion over roughly two years.

Meta shares initially fell as much as 5% on the report before paring losses to around 2% once the market processed it as revenue, not a cost overrun.

Wells Fargo's model shows why the math is attractive even if this specific deal never closes.

If Meta allocates just 1 gigawatt to external resale at roughly $20 billion in revenue per gigawatt, that segment alone could generate $17 billion in operating income at an 85% margin.

That translates to $14.6 billion in net income and $5.69 in incremental EPS, a 16.3% accretion to current FY27 consensus.

That is an extraordinary margin profile, well above what Meta's core ad business typically generates on incremental revenue.

Meta's capacity buildout supports the broader thesis.

Internal-use capacity grows from 6.0 gigawatts in 2025 to 8.0 gigawatts by 2028, while AI focused capacity available for resale jumps from 1.5 gigawatts to 13.2 gigawatts over the same window.

Now here's why Anthropic likely won't get unconstrained access, and why the deal is still early talks rather than signed.

First, Meta's own demand keeps eating into the pool.

CFO Susan Li has said Meta has continued to underestimate its own compute needs, and the company stays capacity constrained through much of 2026.

Every gigawatt leased externally is one Meta chose not to use on its own frontier programs and that tradeoff gets harder to justify the closer negotiations get to a real signature.

Second, the custom chip transition creates a hard ceiling.

Meta plans volume production of its in house accelerator, Iris, starting September 2026, as part of doubling AI capacity from roughly 7 to 14 gigawatts by 2027.

Silicon ramps rarely go perfectly on schedule, and any slippage cuts into spare Nvidia capacity that would otherwise back this lease.

Third, the deal structure itself limits how much gets committed.

Reports suggest 90-day cancellation options on both sides, mirroring the flexible SpaceX-style compute deals.

That clause exists so Meta can reclaim capacity fast if internal demand spikes, which makes any signed deal inherently smaller and more conditional than the $10 billion headline suggests.

Fourth, Meta's own Muse program is why this compute is scarce in the first place.

Meta trained Muse Spark using over 10 times less compute than Llama 4 Maverick while still landing top-five globally on benchmarks.

That efficiency win also reflects how compute hungry Meta's next frontier ambitions remain, raw compute is still the binding constraint, not a surplus sitting idle waiting to be leased to a direct AI competitor.

Either way bullish on Meta!

Morgan Stanley: Apple $AAPL

> Anticipated iPhone Price Hike: Following recent price increases across non-iPhone products, Morgan Stanley now expects a $200 like-for-like starting price increase for the upcoming iPhone 18 lineup (particularly Pro models) in September, up from their previous estimate of $100–$150.

> Protecting Against Inflation: Non-iPhone pricing actions taken on June 25, 2026, indicate that Apple is aggressively prioritizing gross margin preservation to offset sharply rising memory costs (DRAM and NAND inflation).

> Incremental Margins: A $200 price hike on the iPhone 18 Pro (256GB) is estimated to keep its gross margin stable at ~40%. Similarly, the recent $100 increase on the iPad (2025) and $200 increase on the MacBook Air imply internal incremental gross margins of 40% and 27%, respectively.

Consumer Demand & Inelasticity

> Resilient Consumer Behavior: Supply chain checks and steady device lead times suggest that recent price hikes have not negatively affected consumer demand or modified Apple's manufacturing volume strategies.

> Product Elasticity Breakdown: Historical analysis shows Apple's core products possess relatively inelastic demand:

iPhone: The most inelastic product with an estimated elasticity of 0.2–0.5.

Mac: Exhibiting an elasticity of 0.8.

iPad: Demonstrating a roughly unitary price elasticity of 1.0.

SemiAnalysis는 올해 연초부터 같은 패턴을 반복하고 있다.

1. Micron HBM4 배제론

연초에는 Micron이 NVIDIA Rubin HBM4에서 사실상 배제됐다는 식의 이야기가 돌았다.

시장은 “Micron은 차세대 NVIDIA HBM 경쟁에서 밀렸다”로 받아들였다.

그런데 이후 Micron은 Vera Rubin용 HBM4 출하를 발표했고, NVIDIA가 SK하이닉스·삼성전자·Micron을 모두 Vera Rubin HBM4 공급사로 인증했다는 보도까지 나왔다.

최소한 이건 너무 단정적으로 전달됐거나, 후속 현실과 맞지 않았다.

2. SOCAMM 수요 붕괴론

그다음은 Vera Rubin rack의 CPU-side SOCAMM 메모리 축소 이슈였다.

55TB에서 28TB로 줄었다는 이야기가 나오자 시장은 바로 “AI memory demand가 식는다”로 받아들였다.

Micron은 급락했다.

그런데 이 역시 단순한 수요 붕괴로 보기 어려웠다.

오히려 공급 제약 때문에 realistic configuration으로 조정됐다는 반론이 나왔다.

수요가 꺾인 게 아니라, 병목과 공급부족 때문에 구성이 조정됐을 가능성도 있었던 것이다.

3. CPO·800VDC 지연론

그다음이 CPO와 800VDC였다.

SemiAnalysis 리포트 이후 optical 관련주가 한꺼번에 박살났다.

AAOI, COHR, LITE, CIEN, MRVL 같은 이름들이 동시에 맞았다.

논리는 CPO 대량 양산이 2028~2029년으로 밀릴 수 있고, 800VDC ramp도 늦어질 수 있다는 것이었다.

기술적으로 어려운 건 맞다.

CPO는 yield, serviceability, optical engine failure, ASIC integration 문제가 있다.

800VDC도 전력 구조 전환, 부품 신뢰성, rack architecture 난이도가 있다.

하지만 “어렵다”와 “끝났다”는 다른 말이다.

CPO adoption이 느려질 수 있다는 말과 optical interconnect chain 전체가 무너진다는 말도 전혀 다르다.

CPO가 늦어진다고 AI 데이터센터의 optical 수요가 사라지는 게 아니다.

오히려 NPO, LPO, pluggable, ELS, laser source 같은 중간 경로가 더 오래 살아남을 수도 있다.

4. Kyber NVL144 지연론

그리고 이번엔 Kyber NVL144다.

SemiAnalysis는 NVIDIA Kyber NVL144 rack architecture가 78-layer PCB midplane 제조 난이도 때문에 2028년으로 12개월 이상 지연됐다고 주장했다.

여기에 NVL72x2 취소, NVL576 저물량 가능성, Rubin Ultra scale-up domain 제한, AMD·Google 기회론까지 붙었다.

즉 이번에도 단순 제조 리스크가 아니라 NVIDIA 차세대 rack-scale roadmap 전체를 흔드는 narrative가 만들어졌다.

문제는 아직 NVIDIA 공식 확인이 아닌데도 시장은 또 “NVIDIA roadmap 차질”로 바로 소비한다는 점이다.

5. 진짜 문제는 반복 패턴이다

올해 흐름을 보면 계속 같다.

강한 단정.

시장 충격.

후속 반론.

그리고 시간이 지나면 실제 산업 흐름은 훨씬 복잡했다.

Micron HBM4 배제론.

SOCAMM 수요 붕괴론.

CPO 지연론.

800VDC 지연론.

Kyber NVL144 지연론.

하나하나 기술적 논점은 있을 수 있다.

하지만 매번 결론이 너무 자극적이다.

복잡한 제조 리스크가 수요 붕괴처럼 소비되고,

타임라인 조정이 사이클 종료처럼 소비되고,

특정 architecture의 병목이 밸류체인 전체 악재처럼 소비된다.

이 정도면 SemiAnalysis를 단순한 기술 리서치로 보면 안 된다.

지속적으로 이런 식의 교묘한 시장 흔들기성 리포트를 내는 것처럼 보인다면, 리서치 기관의 본질인 “리서치 신뢰도”는 사실상 0에 가깝게 봐야 한다.

리서치 기관의 핵심 자산은 예측력이 아니라 신뢰다.

틀릴 수는 있다.

하지만 계속 강한 단정으로 시장을 흔들고, 나중에 보면 실제 산업 흐름과 맞지 않거나 훨씬 복잡했던 사례가 반복된다면 그건 단순 오판이 아니다.

리서치 품질의 문제이고,

표현 방식의 문제이고,

시장 영향력에 대한 책임의 문제다.

누군가는 이미 SEC에 제보했어도 이상하지 않은 사안이다.

핵심은 리포트가 틀렸냐 맞았냐가 아니다.

market-moving 리서치가 반복적으로 섹터 가격을 흔들었고,

그 과정에서 이해상충, 선행 배포, 포지션 노출, 파생상품 거래 여부가 불투명하다면,

규제기관이 들여다볼 영역이 된다.

특히 SemiAnalysis는 AI 반도체, 데이터센터, 네트워킹 모델을 팔고,

기관용 리서치와 컨설팅을 팔고,

이제는 메모리·포토닉스 ETF 파트너십까지 하는 유료 정보사업자다.

그런 주체가 리포트 하나로 섹터 밸류에이션을 흔들 수 있다면 시장은 당연히 물어야 한다.

사실관계는 충분히 검증됐는가?

기술 리스크가 과장돼 전달된 건 아닌가?

기관 고객 배포 구조와 시장 반응 사이에 이해상충은 없는가?

작성자나 관련 주체의 포지션, 파생상품 노출, 거래 패턴은 투명한가?

부정적 리서치는 필요하다.

NVIDIA roadmap에도 리스크는 있다.

CPO도 어렵다.

800VDC도 어렵다.

Kyber도 쉽지 않다.

하지만 어려운 것과 망한 것은 다르다.

지연 가능성과 수요 붕괴도 다르다.

제조 병목과 산업 thesis 훼손도 다르다.

SemiAnalysis 리포트는 기술 자료로 참고할 수 있다.

하지만 그대로 믿고 매매하면 안 된다.

반드시 NVIDIA, Micron, Broadcom, Marvell, GF, Jabil, Coherent, Lumentum, Sivers 같은 primary source와 대조해야 한다.

올해 SemiAnalysis가 보여준 건 기술 통찰만이 아니다.

시장 narrative가 어떻게 만들어지고,

그 narrative가 어떻게 주가를 때리고,

그 과정에서 nuance가 얼마나 쉽게 사라지는지도 보여줬다.

리서치가 시장을 움직이는 순간,

그건 단순한 의견이 아니다.

검증받아야 할 권력이 된다.

$MU Micron is now a top 10 holding in the S&P 500 with a 1.9% weighting.

Nvidia $NVDA used to be closer to 8.5%, it’s now down to 6.99%.

Apple $AAPL used to be 7.5%, it’s now 6.18%.

The old guys have had to make room for the new kid on the block.

South Korean investors have never borrowed this much to buy equities:

Margin loans in South Korea are up to a record ~$26 billion, DOUBLING since the start of 2025.

However, as a % of Korea's free float, the portion of the market value available for public trading, margin loans are down to ~0.8%, the lowest since the 2020 pandemic low.

This comes as the surge in market cap has significantly outpaced the growth in leverage.

Meanwhile, during the recent market pullbacks, the daily forced liquidation ratio spiked to 4-5% of total outstanding margin loans, well above the ~1% seen under normal conditions.

This means brokers were forced to liquidate 4%-5% of all margin-backed positions in a single day because borrowers could not meet their margin calls.

Record leverage is exacerbating South Korea's market volatility.

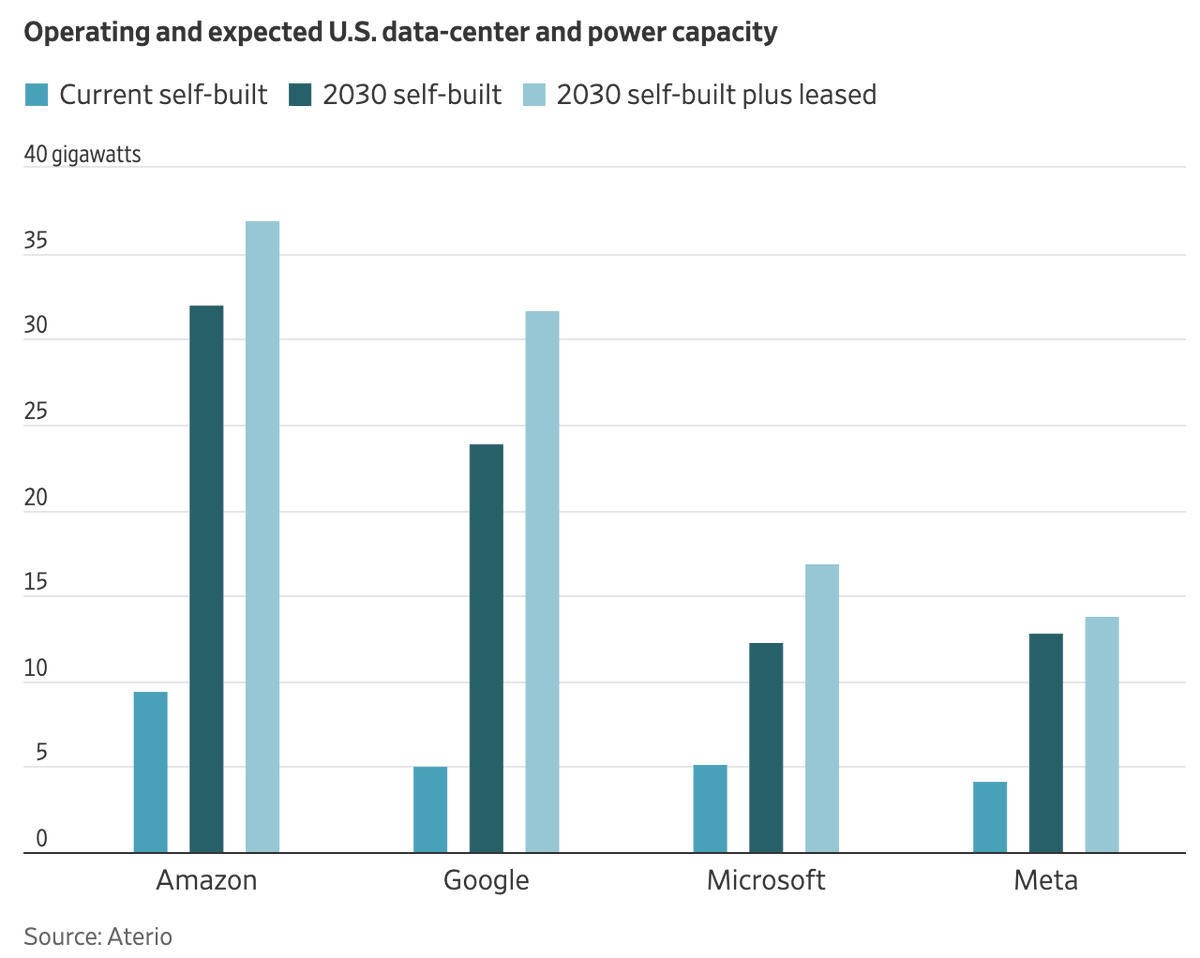

The AI race might come down to energy. Who has the most MW?

Great article in WSJ

Short answer: Amazon. 9 GW today. >35 GW by 2030

Longer answer: Google catching up. 5 GW today. >30 GW by 2030

- Amazon has a “really good understanding of building capacity”. Largest cloud business + 2 decades of data center dev experience

- WSJ: “Thus far, Amazon’s strategy seems to emphasize cost and reliability, while Google appears focused on clean energy”

- Amazon builds most of its own data centers, Google relying also on leases including renting compute from SpaceX, 25% of Google MW by 2030 from leases

- Self built vs leasing? "Self-built can take longer but is the cheaper option over the long term". Obviously other factors too like capital at risk etc

- Expert says Google “doing everything it can” to avoid building data centers that rely on fossil fuels

- Now to 2030, Google adding capacity at the “fastest rate”. Including leased capacity, Google projected to be much closer to Amazon by 2030