Retired PM at multi-billion L/S fund. Sharing career advice and insights to help aspiring analysts break into the hedge fund world. Not Investment Advice

Using a quantitative framework to understand which factors have the greatest impact on valuation multiples

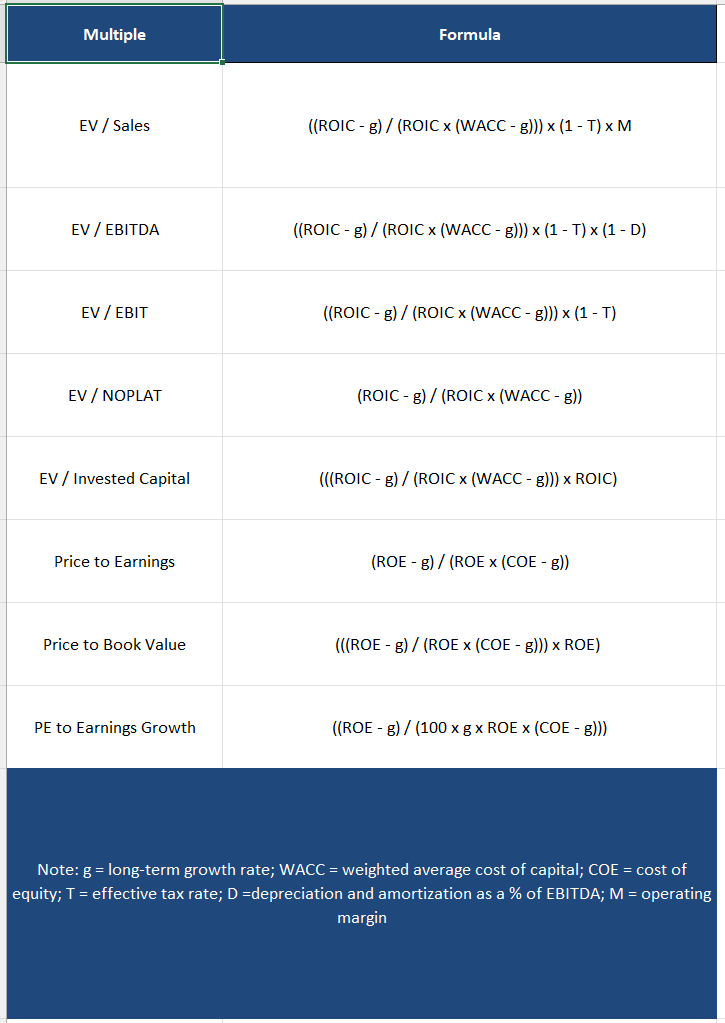

Important quantitative drivers of a valuation multiple are return on capital, cost of capital, growth, and duration of growth. From a quantitative perspective, it is important to understand which factors will have the greatest impact on a company's valuation multiple - What is the impact to the multiple from a 1% change in the return on capital? What is the impact from 2 points of long term growth to the multiple? Target multiples can be derived based on these underlying drivers using the formulas below.

The formulas below assume that value-adding growth will continue perpetually. This is a simplifying assumption but more realistic two-stage versions of the formulas can be used which incorporate an initial growth period followed by a terminal period.

Comment below if you'd like the excel file with the one stage formulas, two stage formulas, and their derivations.

Great podcast with Brian Christiansen from Sands Capital. Insightful discussion regarding the firm's approach to growth investing and the six investment principles that the firm employs:

Sustainable above-average earnings growth

Leadership position in a promising business space

Significant competitive advantages/unique business franchise

Clear mission and value-added focus.

Financial strength

Rational valuation relative to the market and business prospects

https://t.co/TZZ7P79yoc

Time Arbitrage: Is time on their side?

Does time benefit the company by bringing significant opportunities closer (i.e. significant growth in demand, market share gains, cost deflation, margin expansion, etc) ?

OR

Does time work against them and is the business a melting ice cube (i.e. market share losses, declining demand, technological disruption)?

The market is often good at discounting the near term, but greater opportunity often exists in the mid and long term where there is greater variability in earnings estimates

When so much attention is focused on the quarter itself, think through the post-earnings print setup:

Who is the incremental buyer/seller post print and what are they playing for?

Will conditions improve or deteriorate from this point? What does the rate of change and second derivative look like going forward?

Transition / restructuring years can present excellent opportunities, often sooner than expected.

Fast money often sell or short stocks that are in these transition periods, opening up exciting arbitrage opportunities for those who believe the company will emerge stronger

On the flip side, stocks can swiftly rise to price in management’s long-term goals presented at analyst day events. Think of this as a free put option on management’s execution skills. Shorting these situations is especially potent for companies with weak track records or overly optimistic forecasts

Key concepts to understand how L/S equity multi managers think about risk:

$Vol: Rather than thinking of a portfolio solely in terms of gross capital, many L/S PMs think about their portfolio in terms of $Vol. $Vol is the standard deviation of the portfolio's returns in dollar terms (% Annual Vol X Gross Capital). So assuming a $1bn portfolio at 4% vol is $40mm in terms of $Vol. An average PM with a 1.0 Sharpe Ratio thus should be putting up $40mm of P&L on an average year on this portfolio.

Risk Model: Factor models are used to dissect the sources of volatility and limit unintended exposures (style factors like growth, value, momentum, size, etc) and concentrate risk related to the core ideas that cannot be explained by style factors (idiosyncratic volatility). Requirements are typically put in place such that a portfolio's volatility must be sourced from a certain idio threshold (60-85%) to minimize factor risk.

Leverage: More leverage is used on portfolios with lower volatility and less on those with higher volatility all else equal. Typically leverage ranges from 2x to 5x on a given portfolio.

Liquidity: It's crucial to be able to exit positions quickly upon realization of your thesis OR when the facts have changed and your thesis is broken. Rule of thumb: Limiting the size of a position to 30% of one day's ADTV (average daily trading volume) ensures you can exit within ten trading days without significantly impacting the stock price (by being ~3% of volume per day)

Concentration: There are obviously a wide range of concentration limits and investing styles across the industry on how big an individual position can be of a portfolio, but a key rule of thumb: if a position is so large it dictates how your day is going and your focus, then it's too big and you will inevitably take your eyes off the ball from the rest of your portfolio and coverage.

#HedgeFunds #RiskManagement #Volatility #Leverage #Liquidity #Concentration

Hedge fund titan Seth Klarman shakes up Baupost Group: 19% of investing team cut in biggest restructuring in firm history. Layoffs concentrated in the real estate and equities units. Shifting focus to distressed debt, special situations, private investments, and capital solutions