Our CEO @aprilloong breaks down why remittance companies aren't solving Africa trade payments, and what the real gap is.

If you care about where Africa cross-border payments is actually headed, read this 👇

If you're in Singapore and work anywhere near cross-border payments, stablecoins, or emerging markets — come hang out Thursday evening.

Waka Night. No slides, no panels. Just operators, builders, and good conversations.

Details in replies 👇

Waka is hiring. Three remote roles building cross-border payment infrastructure for emerging markets:

→ Junior Trading Operations

→ Payments Compliance Operations

→ Full-Stack Engineer

Full roles and how to apply in the articles👇

Monday read: A short guide to why paying into China is harder than it looks. 🧐📖

If stablecoins help aggregate liquidity for cross-border trade, the real question becomes: how do you actually settle on the China side?

Three things make it different.

🤝Trust is institutional, not contractual.

A Chinese bank receiving a payment from Lagos has no relationship with the African counterparty, and limited visibility into the market. Compliance is outcome-based: the bank is liable if a payment turns out fraudulent. The default response to anything unfamiliar is to slow down.

💴 Renminbi is a bifurcated currency.

Offshore CNH trades freely in Hong Kong and Singapore. Onshore CNY is accessible only through approved channels, with a daily band set by PBOC. Most Africa-China payments today settle in offshore CNH or USD because mainland compliance is heavier. The trade-off: FX spreads, slower working capital, and a more cumbersome process for the Chinese supplier.

📩Every payment must be verifiable against the trade.

SAFE and PBOC require invoice values to match customs declarations, and counterparty details to match the original contract. The data traveling with the payment is what makes it legitimate. Without it, the payment clears eventually, but only after delays compound.

The corridor's problem is not just a rail problem. It's a trust problem, a compliance problem, and a documentation problem at the same time. Anyone solving for only one will eventually find the other two waiting. 🧐

Congrats on the fast growth of direct China-Africa port-to-port routes! The shipping side is being rebuilt.

That naturally makes you think about the other side of the trade: payments.Most of these transactions still go through old correspondent banking routes via New York or London: multiple conversions, delays, and fees.Ships are now going direct. Money hasn’t caught up yet.

Waka is working to close this gap using stablecoins for local-to-local settlement. We're curious to hear thoughts from trade, logistics, and finance folks — how do you see settlement rails evolving in the coming years?

Leave your comments👇

Fast growth of direct port-to-port routes between China and Africa, after the introduction by China of total zero-tariff for African imports. The increase in air links between the 2 is led by African carriers while the new maritime surge is led by Chinese shipping companies.

https://t.co/dHYqVY7vpc

The "stablecoins are just a crypto thing" narrative is getting harder to hold.

@Visa just hit $ 7B annualized stablecoin settlement volume across 9 chains and 50+ countries.

This isn't hype. 🚀

Stablecoins are moving from idea to infrastructure—powering real settlement. Visa has hit a $7B annualized run rate, + 50% QoQ.

We have expanded our global stablecoin settlement program to @Arc, @Base, @CantonNetwork, @0xPolygon and @Tempo, bringing us to nine chains.

Stablecoins are multi‑chain. Settlement has to be seamless across it.

Cross-border trade never clocks out.

Neither do the people behind it.

To every seller, operator, and builder moving money and goods across borders: happy Labor Day!

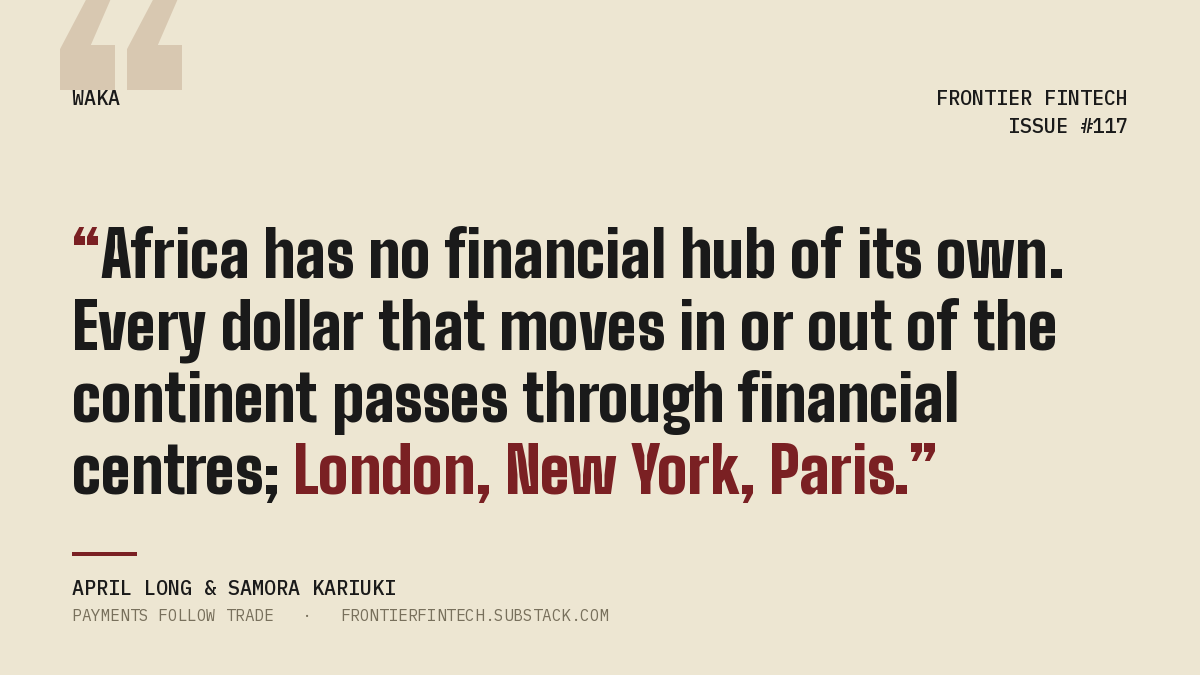

Africa does not have a dollar problem.

The dollars are already there — but fragmented across offshore accounts and routed through financial centres not built for Africa–Asia trade.

Stablecoins change this by aggregating offshore dollar liquidity onto public blockchain rails.

More in the article co-authored by our CEO April Long and @SamoraKariuki 👇

Every year, African businesses move billions of dollars to pay their Asian supply chain partners. Electronics, machinery, solar panels, construction equipment. They pay slowly, expensively, and through infrastructure designed for entirely different corridors.

The correspondent banking system was built to serve trade flows that ran west. Africa's trade increasingly runs east. In 2024, Africa ran a $62 billion trade deficit with China while running surpluses with Europe and the United States. The dollars earned in London and Brussels must eventually reach Shenzhen and Guangzhou. The infrastructure connecting those two realities was never designed for the job.

Stablecoins are changing part of this picture; less as a new currency, more as a mechanism for making existing dollar liquidity move at the speed trade actually requires. But the rail is only one layer. Settling into China carries compliance requirements that have no equivalent in Western payment systems. The data that travels with the payment is what makes the payment legitimate.

Our latest piece on Frontier Fintech examines what it takes to build infrastructure that fits this reality and profiles Waka, the company April Long built after a decade managing the Africa-Asia corridor from inside Standard Chartered Kenya.

Link in Comments. Subscribe to Frontier Fintech.

Waka didn’t choose stablecoins because they became the narrative of the year.

We chose them because the economics changed.

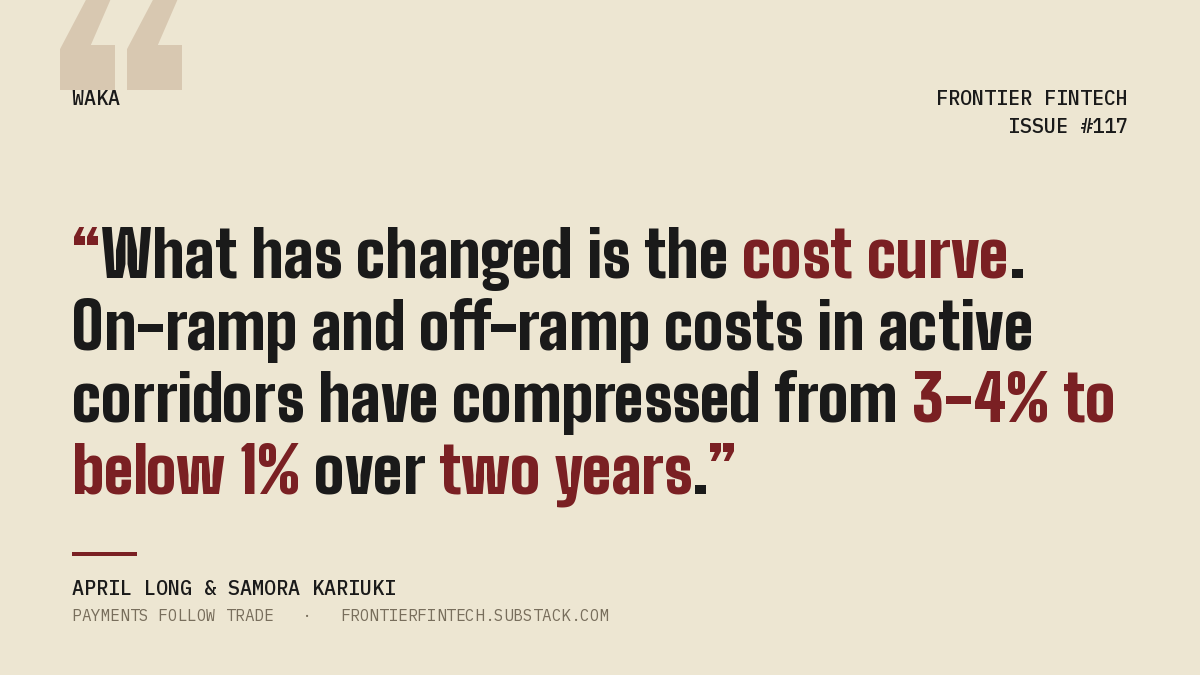

On/off-ramp costs in active Africa–Asia corridors fell from 3–4% to below 1% in two years.

The real story is the cost curve.

Why we keep saying trade finance and stablecoins are converging. Look at what’s happening lately:

→ MoneyGram + NALA: stablecoin payouts in Africa & Asia

→ Tether debuts tether.wallet, self-custodial

→ SocGen lists its MiCA stablecoin on MetaMask

→ Visa, Stripe, Zodia join Tempo as first external validators ...

And this is just one week of headlines. What Waka is building sits inside this great shift.

Keep moving and shipping. 🚀

Kenya just closed public consultation on its draft VASP Regulations 2026, and the details are worth a closer look.

The regulations operationalize the VASP Act that took effect in November 2025. What stands out is how specific they are:

🏛️ Dual-regulator model: Central Bank of Kenya for payments + stablecoins, Capital Markets Authority for exchanges, brokers, and tokenization

💰 Stablecoin issuers face a KSh 500M (~$3.86M) paid-up capital requirement, with other VASP categories at different thresholds

🏦 Licensing applicants must disclose principal bankers and account details. Stablecoin issuers face explicit Kenya-based banking requirements, with at least 30% of reserves in segregated local accounts

🗣️ Public participation forums held across 11 cities, from Mombasa to Garissa

Kenya is writing sector-specific rules with real numbers, at a pace ahead of many larger economies still stuck in consultation loops. A fast-growing African economy treating digital settlement as part of its financial architecture from day one.

The region is strategic for our growth; it serves as an important gateway to Africa and functions as a primary financial innovation hub.

VIRTUAL ASSETS

Kenya moves closer to regulating virtual assets as public participation on the Draft Virtual Asset Service Providers (VASP) Regulations, 2026 concludes.

The Regulations operationalize the Virtual Asset Service Providers Act, 2025, providing a clear legal framework for licensing, regulating, and supervising virtual asset businesses in and from Kenya.

Virtual assets such as cryptocurrencies, tokenized assets, and stablecoins are reshaping global finance.

Kenya is positioning itself to harness innovation while safeguarding financial stability, protecting consumers, and managing emerging risks.

Public value:

The framework establishes a fair, transparent, and competitive market,supporting innovation, strengthening investor confidence, and unlocking new economic opportunities.

Strong safeguards introduced include:

• Fit & proper ownership requirements

• Adequate capital thresholds

• Strong governance frameworks

• Robust risk management and AML/CFT compliance

Consumer protection remains central:

• Clear risk disclosures

• Transparent pricing structures

• Effective complaints handling mechanisms

• Strict segregation and protection of customer assets

Market integrity measures include:

• Fair and orderly trading rules

• Due diligence before listing virtual assets

• Continuous monitoring of markets

• Zero tolerance for manipulation, insider trading, and false trading

Enhanced oversight and resilience measures include:

• Continuous reporting and disclosures

• Onsite and offsite supervision

• Strong cybersecurity and incident reporting frameworks

• Mandatory audits, insurance, and prudential requirements

A whole of

government approach anchors implementation, bringing together The National Treasury, Central Bank of Kenya (@CBKKenya), and Capital Markets Authority (@CMAKenya) for coordinated oversight.

Kenya is building a trusted framework that balances innovation with financial stability.

Next step: review and consolidation of stakeholder submissions ahead of finalization of the Regulations.

Stakeholders are encouraged to follow updates as Kenya advances this regulatory framework.