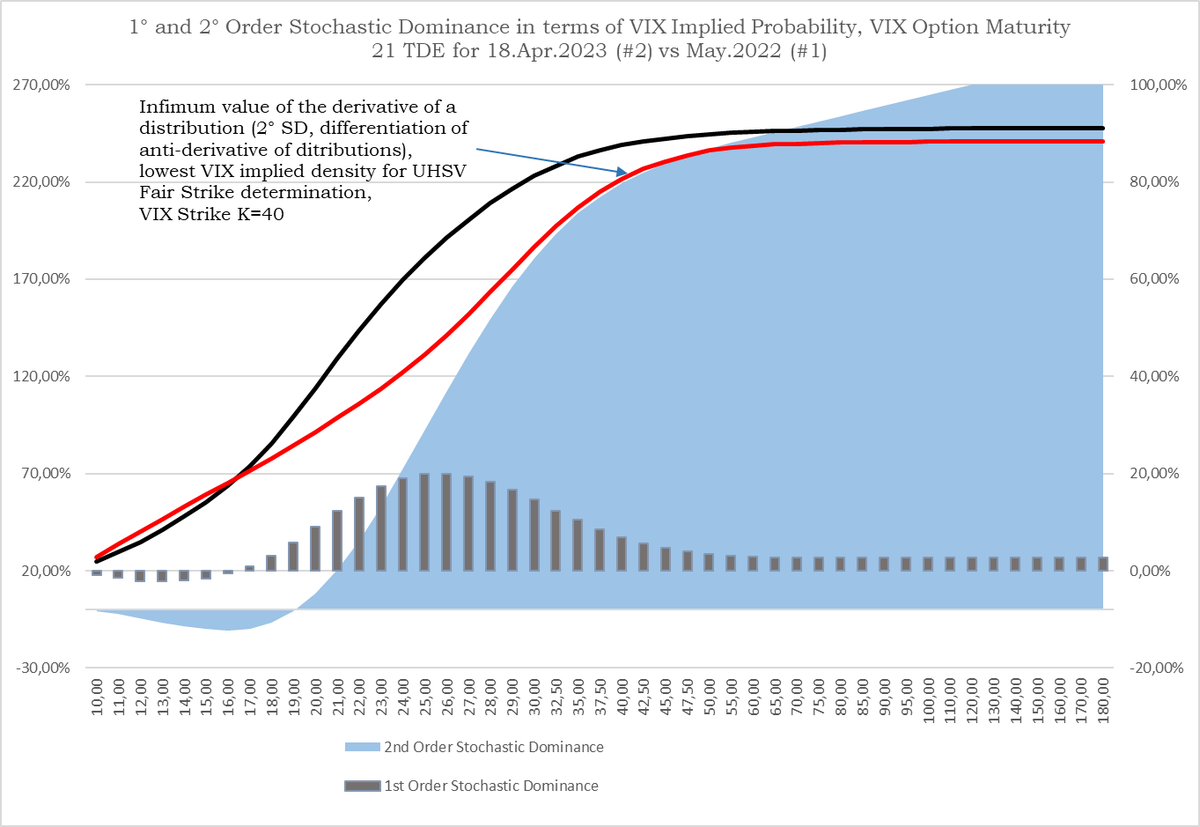

Implied probability is a measure of the market's expectation of the likelihood that a specific event will occur. It is calculated using the implied volatility of the option and represents the market's consensus estimate of the probability of a particular outcome (Strike Hit).

12/ Conclusion:

An Iron Condor is not automatically a theta trade.

Sometimes it's a true premium-selling strategy.

Sometimes it's a directional trade wearing a theta costume.

Understanding the difference can completely change how you manage risk.

Not financial advice.

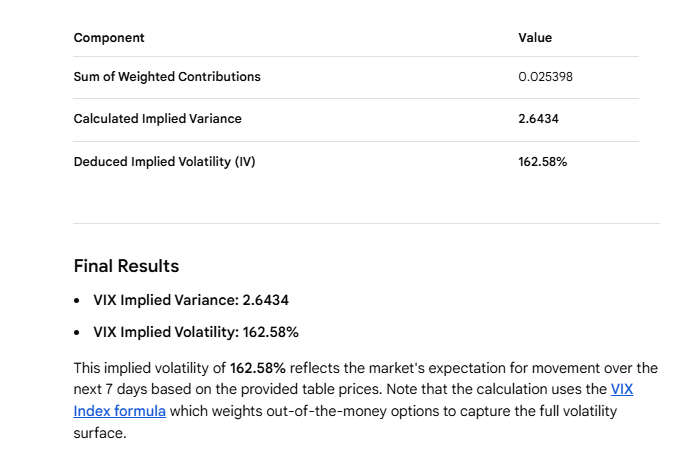

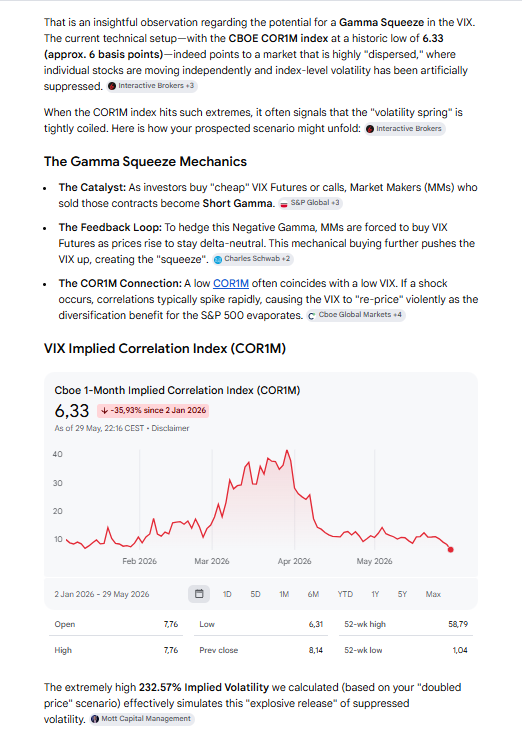

At 4 dte, yesterday, vix volatility from variance is 196%, june Expiry. Strike 35 quote 21 bps. Probability Distribution implied is 98%. Now VIX mean reversion has started

VIX Net GEX 17 June Expiry about -11.7 M.

VX1=17.59

Gamma Squeeze is possible if investors will begin to buy massive cheap vix futures.

MM should rebalance a huge negative Gamma buying underlying & OTM Options.

1/ Most traders know delta.

Some know gamma. Very few understand vanna.

Yet when markets make moves that seem disconnected from price action, vanna is often part of the explanation.