Investors continued to shy away from the tech giants that dominate much of the stock market in favor of a broader category of firms. Renewed volatility among semiconductor giants comes amid broader warnings that the market is about to top out.

While the industry’s long-term outlook remains tied to a flood of spending on artificial intelligence, Wall Street is increasingly questioning that dynamic. “As much as we love to see tech’s leadership, it would be constructive to see this rally broaden out to other sectors,” said Bret Kenwell at eToro. “When leadership is concentrated in one corner of tech, the market’s foundation gets a little wobblier.”

Here comes the sun: Solar overtook coal in US power generation last month, the first time the renewable source bested the fossil fuel. The milestone comes as the US races to meet AI-driven power demand, and despite efforts by the Trump administration to slow the renewable industry’s growth. Clean-power additions are still on track to hit a record this year. This shift underscores not just a symbolic turning point but a structural one: solar’s scalability, declining costs, and rapid deployment timelines make it uniquely suited to meet surging, AI-driven electricity demand faster than traditional generation sources can adapt.

President Trump has renewed calls for an audit of Fort Knox, which reportedly stores 147.3 million troy ounces (4,582 tons) of gold worth about $650 billion today. The vault, built in 1936 and protected on a U.S. Army base, has rarely been accessed by outsiders. The last full audit occurred in 1953, with a partial review in 1974 and an inspection in 2017. An audit could finally address longstanding speculation about the reserves.

Central banks resumed gold buying in April. The resumption of central bank purchases provides a constructive signal for the gold market, as official sector demand has become an increasingly important pillar of support in recent years. Unlike speculative investment flows, central bank buying is typically driven by long-term strategic considerations, helping to reinforce the underlying demand profile for gold and potentially limiting downside price volatility.

Bitcoin is teetering on the edge of another decline, having lost half of its value since reaching its record high in October, Reuters reports. Investor interest in the world's largest cryptocurrency has cooled significantly amid the hype surrounding AI companies and several high-profile upcoming IPOs, including SpaceX, which are attracting substantial amounts of capital. The coin is currently hovering around the psychologically important $60,000 level, and a break below this threshold could trigger both a wave of panic selling and aggressive buying by bargain hunters looking to capitalise on lower prices.

The Nasdaq 100 plummeted about 5%, its deepest dive since April of last year, while a gauge of chipmakers fell twice as much Friday as Wall Street ended the weak on a decidedly sour note. What might be eating at investors (despite the frenzy over SpaceX’s IPO) is a return of that unscratchable itch known as fear of over-valuation. Worries that a tech stock bubble may soon deflate combined with surprisingly big jobs numbers, and thus suspicions the Fed — even with a new chair courtesy of Donald Trump — could raise rates, triggered serious profit-taking.

$XAUH is coming to #BTSE!

🚀@HerculisCoin

🔹 Pair: XAUH/USDT

🔹 Deposits: 9 AM (UTC+0), June 5 📥

🔹 Trading: 8 AM (UTC+0), June 8 🔔

Get ready for the new listing!

#NewListing

Since 1971, the U.S. dollar has lost 99.24% of its value relative to gold. Over the same period, the British pound has declined by 99.57%. Had the euro existed at the time, it would have lost 99.08%.

The long-term depreciation of major currencies against gold reflects the structural consequences of the fiat monetary system that emerged following the abandonment of the gold standard in 1971.

For long-term investors, gold is not merely a speculative asset but a strategic hedge against the systemic debasement of paper currencies and the erosion of the real purchasing power of monetary savings.

Gold has overtaken U.S. Treasuries as the leading reserve asset. According to the Financial Times, by 2025 the share of gold in central bank reserves had increased from 20% to 27%, while the share of U.S. government securities declined from 25% to 22%.

Against the backdrop of rising U.S. public debt, sanctions-related risks, and growing geopolitical fragmentation, central banks are increasingly viewing gold as the most neutral and sovereign-independent reserve asset. For many countries, gold is becoming a strategic tool for reducing dependence on the U.S.-dominated financial infrastructure and enhancing the resilience of reserves in an environment of global uncertainty.

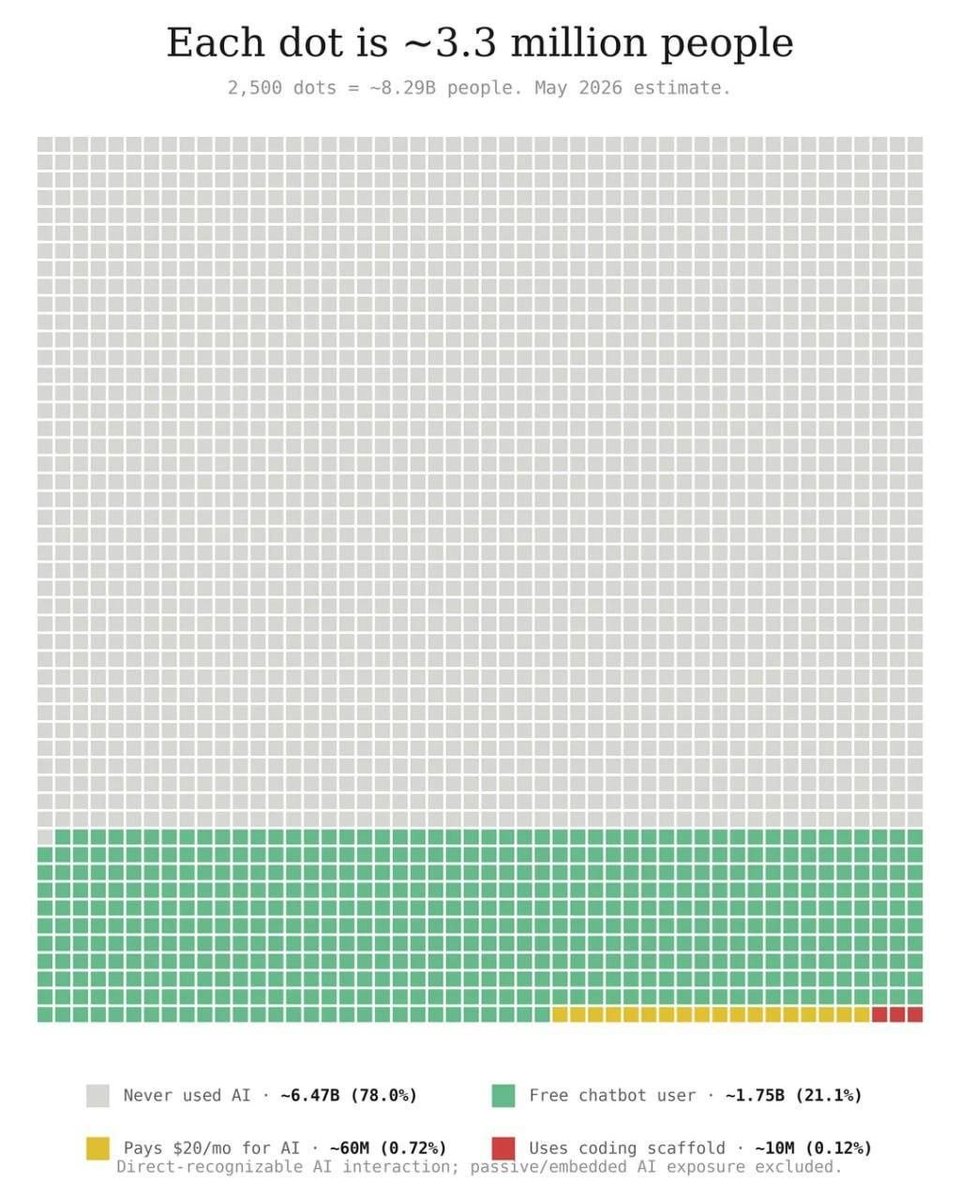

AI adoption remains remarkably early-stage despite the hype. Even with rapid growth in AI awareness, the data suggests that nearly 80% of the global population has never directly interacted with AI tools. This implies that we are still in the very early phase of adoption, comparable to the internet in the late 1990s.

For the time being only around 60 million are estimated to pay for AI services. The industry may therefore face significant pressure to prove sustained productivity gains and differentiated value before subscription-based models become broadly scalable.

The number of users leveraging AI for coding or workflow scaffolding represent only ~0.12% of the global population. This suggests that the most transformative AI use cases — automation, software generation, and productivity augmentation — are currently concentrated among a very small, highly technical user base.

Hong Kong has narrowly overtaken Switzerland to become the world’s largest cross-border wealth hub, driven by an influx of mainland Chinese capital and a resurgent local equity market. The shift comes as global private fortunes expand at their fastest clip since 2021, defying the US trade war and macroeconomic instability to reach a total of $333 trillion. While Hong Kong and Singapore form an expanding ecosystem serving Asian capital, Switzerland, the US and the UK remain primary conduits for European, Middle Eastern and Latin American wealth.

Space and satellite-related stocks soared Tuesday as investor enthusiasm around the industry intensified following last week’s SpaceX initial public offering. Shares of space infrastructure company Redwire jumped 26%, satellite broadband communication company AST SpaceMobile surged 13% and rocket and spacecraft maker Firefly Aerospace rose 19%. Growing excitement around the burgeoning space economy is increasingly favoring companies positioned to benefit not only from SpaceX’s debut, but also from rising enthusiasm for space exploration and increased funding.

$4400 on gold: this support MUST hold

Gold has continued its huge consolidation phase following the violent pukes we saw earlier this year. The shorter-term trend line has survived several tests, but we are now approaching the major $4400 level, with the 200 day moving average coming in just below.

That is the must hold area.

The Turkish Lira has collapsed to another all-time low against the U.S. Dollar — now down nearly 98% since 2010. This is very illustrative example how uncontrolled inflation and currency debasement look like. For generations, people protected their wealth with one asset that governments cannot print: Gold. The smartest long-term strategy is simple: Buy gold bars regularly and preserve purchasing power over time.

Those who saved in fiat lost wealth.

Those who accumulated gold preserved it.

In times of monetary uncertainty, gold is not speculation — it is financial protection.

Start thinking in ounces, not in depreciating currencies.

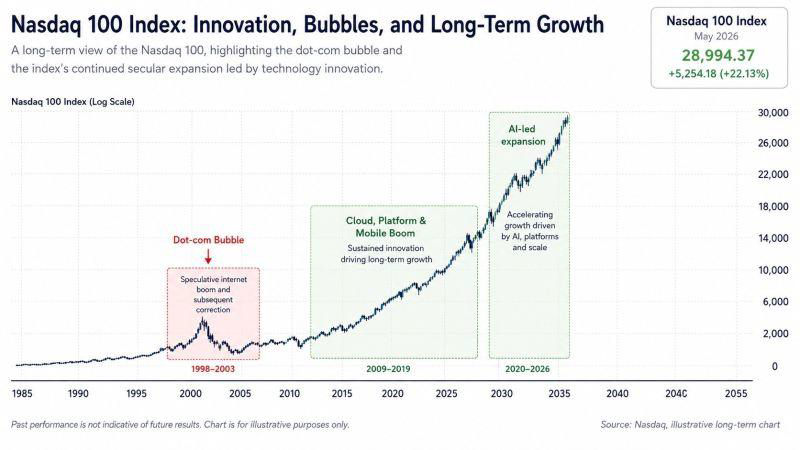

What a journey for the Nasdaq 100...

If you had invested $10,000 in the Nasdaq 100 ETF $QQQ at the PEAK of the dot-com bubble in March 2000, your investment would be worth around $61,650 today — a gain of +516%, or +7.2% annualized. And that’s despite navigating through 9/11, the 2001–2002 recession, the Global Financial Crisis, COVID-19, and major geopolitical conflicts including Russia-Ukraine and tensions in the Middle East. As Warren Buffett famously said: “Never bet against America.”

Miners are currently seeing the strongest margins in the history of the data. Higher realized gold and silver prices, combined with relatively stable operating costs, are driving exceptional free cash flow generation across the mining sector, significantly improving balance sheets and capital return capacity.

Despite record operating margins, many precious metals miners continue to trade at valuation multiples below historical bull-market averages, suggesting the market may not yet be fully pricing in the current profitability environment.

conomists biggest fear… Current US CPI trends have closely mirrored the path from 1966–1982, with a reported correlation of 0.93. Such a high correlation suggests that underlying inflation dynamics—such as wage pressures, persistent services inflation, and policy lags—may again be underestimated, increasing the risk that inflation proves far more stubborn than markets currently price in.

The Chinese central bank remains the most unwavering “buy-the-dip” force in gold.

The consistency of Chinese central bank gold purchases reflects a broader strategic diversification away from US dollar reserve dependence. This trend reinforces gold’s evolving role not only as an inflation hedge, but also as a geopolitical reserve asset.

Persistent sovereign accumulation during price pullbacks provides structural support for the gold market. Unlike speculative flows, central bank demand is typically long-duration and policy-driven, which can materially tighten physical supply dynamics over time.

There is a record $8.19 trillion in money market funds right now. The record level of assets in money market funds suggests that institutional and retail investors remain unusually defensive despite strong equity market performance. Large cash balances often indicate elevated uncertainty around valuations, interest rates, or macroeconomic stability.

From a market structure perspective, $8.19 trillion sitting in money market funds also represents significant “dry powder.” If inflation moderates and monetary policy becomes more accommodative, even a partial rotation of this capital into equities, credit, or real assets could become a powerful driver of asset prices.