A reminder: Mike agrees with my analysis, so you should definitely look at $FIGR, and probably at my substack post (it's free!!!!!)

https://t.co/eBwmX1ebov

On a recent podcast I talked more about the comparison between Fannie Mae and Figure. Two points stand out as people look to understand Figure better:

1. Fannie Mae has created liquidity in its capital market that offers homogeneity in the assets / mortgages, regardless of which originator made the loan

2. Fannie Mae is clearly a larger business than any one mortgage company or originator.

We are a version of Fannie Mae on modern, blockchain rails with the ambition to expand across all asset classes.

People will say we don't have the guarantee from the Government, that's true. But credit risk is not the only (or dominant) risk in mortgage. It's prepayment and interest rate. And we do use the blockchain to prevent fraud from double pledging and double sale of loans (a real risk Fannie Mae can't prevent).

We are on the up!

https://t.co/lTYReIHMRx

I give it a year until we see a new breed of AI native private equity firms that acquire companies just so they can move their workflows from Claude to open source Chinese models and flip them.

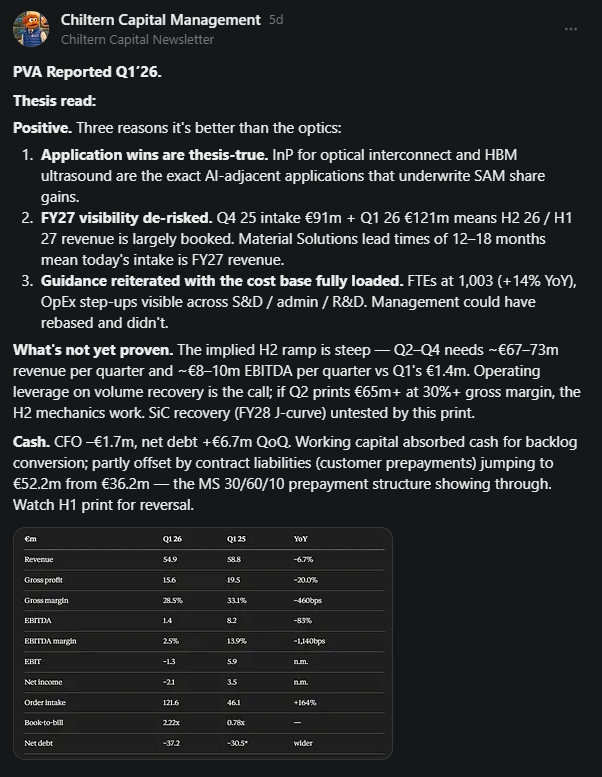

NEW TRADE IDEA. That's right. Chiltern Capital is back baby. I read every filing of a blockchain mortgage company run by crypto people so you don't have to. Verdict: absurdly cheap. $FIGR long thesis 👇

NEW TRADE IDEA. That's right. Chiltern Capital is back baby. I read every filing of a blockchain mortgage company run by crypto people so you don't have to. Verdict: absurdly cheap. $FIGR long thesis 👇

NEW TRADE IDEA. That's right. Chiltern Capital is back baby. I read every filing of a blockchain mortgage company run by crypto people so you don't have to. Verdict: absurdly cheap. $FIGR long thesis 👇

NEW TRADE IDEA. That's right. Chiltern Capital is back baby. I read every filing of a blockchain mortgage company run by crypto people so you don't have to. Verdict: absurdly cheap. $FIGR long thesis 👇

NEW TRADE IDEA. That's right. Chiltern Capital is back baby. I read every filing of a blockchain mortgage company run by crypto people so you don't have to. Verdict: absurdly cheap. $FIGR long thesis 👇

NEW TRADE IDEA. That's right. Chiltern Capital is back baby. I read every filing of a blockchain mortgage company run by crypto people so you don't have to. Verdict: absurdly cheap. $FIGR long thesis 👇

One of the best posts on AI compute I’ve read in a long time. It explains why semis stocks have become 40% of the market index weight from a technical perspective and lays out a roadmap for the tech evolution ahead.

One incredible (and unrelated) fact I learned a couple years ago that stuck with me was that some 90% (could be lower now) of the energy consumed by AI isn’t used on compute at all but by shuttling the model weights back and forth btwn the GPU and memory. This post explains using the analogy of airport shuttles btwn gates and airplanes and the strong complementarity btwn GPU throughput and HBM capacity and bandwidth.

The AI models have become powerful and genuinely useful for most everyday use incl enterprise production that requires high accuracy. We are now witnessing an explosion of “inference” or the actual usage or deployment of the models via AI agents or AI calling AI. The artificial intelligence is finally good enough in most contexts that we are going to see an explosive growth of the consumption of “intelligence”.

As long as we remain in this current architecture of LLM transformers running inference on discrete GPUs + off chip HBMs, AI compute will remain structurally “memory bound”. In fact, barring big architectural changes we can anticipate demand to persistently outstrip supply turning a historically strongly cyclical industry into one that’s well not cyclical anymore, an assertion that has drawn ridicule.

Now, “nature always finds a way”. And shortage is always the mother of innovations. We are now seeing a wide range of attempts to overcome the structural memory bound. Attempts are being made on both the hardware and the software fronts notably on-chip static RAM or SRAM such as the integration of Groq by NVidia, Amazon + Cerebras, and Google’s TPU (and TurboQuant).

Beyond that efforts are being made in adoption of optical interconnects to further disaggregate memory allowing for more efficient compute as well as potentially doing photonic compute directly in memory. These are ofc developments and possibilities that further out. For now the dynamic of heavy memory bound compute that @fi56622380 lays out still strictly dominates.

All of the above relates to the supply side ofc and the implicit key assumptions. There’s also importantly the demand side. There’s a presumption among AI hardware enthusiasts that we are in a paradigm of persistent “supply shortage”. That may well be the case as demand and adoption for machine intelligence grow exponentially while supply is constrained by supply chain bottlenecks.

However, it’s worth considering the ways in which demand may indeed fluctuate. After all oil demand grew secularly but oil prices also fluctuated significantly, notwithstanding the big differences in oil discovery/refining vs GPU/CPU/memory supply. Demand for AI could indeed slow or grow slower than expected if enterprise adoption ran into frictions or if the ROI proved initially elusive esp if the prices of AI inference keep growing to reflect their true economic costs let alone their economic value created. Demand curve slopes downwards. That logic hasn’t been tested yet. That’ll have to be for another Ackman-esque long post on a different sleepless morning. I hate pollens.

@QuartzResearch Thanks! Feel free to check this one out too!

https://t.co/Gsgydd7WZg

EU company that is in the middle of the AI bottleneck for compute!!

Every AI chip stacks memory 12 layers high. Next gen goes to 32. Every single layer needs to be inspected for invisible defects before the next one goes on top.

This is the next AI bottleneck nobody's talking about ↓