We have been discovering hyper-performing stocks for 30 years.

Consistent 2x - 30x returns. Unbiased, no ads ever.

TSX ● TSXV ● CSE ● OTCQB ● OTCQX ● Nasdaq

$KCLI.c $APCOF

Agapito are the global gold standard for evaporite mineral evaluation. Same firm that prepared $MLP.v's PEA

Agapito prepared KCLI's 2012 #potash 43-101 establishing the 600 million to 1 billion tonne exploration target.

Now they are doing #lithium 👇

Things just got a lot more interesting for $KCLI.c

American Critical Minerals, with NYSE: $IPI's 60+ year #potash mine just 20km away, brings on board a former $IPI executive and salt minerals expert, Kenneth Taylor.

IMO the $12M market cap is going to massively rerate, soon. (ps. They also have a significant amount of #lithium in the brines)

$KCLI.c NEWS: Kenneth Taylor, former senior executive with NYSE: $IPI (Intrepid #Potash) joins KCLI as a strategic advisor; positioning their $12M market cap for a major re-rating

I just published my breakdown in this article - you'll want to read it 👇

https://t.co/Y65AgEWyB3

An $MLP.v style move is coming for $KCLI.c

They've just added a former senior ex-Intrepid Potash (NYSE: $IPI) exec as an advisor - setting up the blueprint to take it from brownfield to production.

$12m market cap for what they are planning? Incredible setup.

#potash#lithium

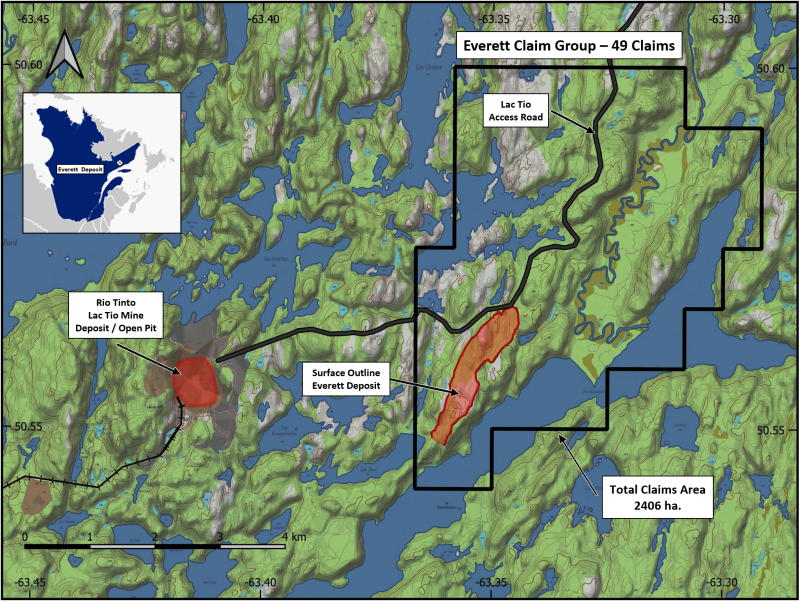

What have I found here? $MUZU.cn

42.5m shares outstanding, last @ 0.08

Advanced stage, drill ready @ $3.4m CAD m/c

Muzhu Enters Into a LOI to Drill and Develop the Everett V-Ti-Fe-P Deposit, Quebec

The Everett deposit is a "globally significant ilmenite source", spans 2,406 ha in Quebec, near the world-class Lac Tio mine, with historical data showing high Ti, Fe, and P recoveries.

Drill-ready with 34 historical drill holes and 71 surface samples; one-year program planned to verify and define resources by July 2026.

40 km from Havre-Saint-Pierre port, with road access, hydroelectric power, and proximity to mining infrastructure

50% option for $800,000 cash, 3M shares, and $10M exploration by 2029; 3.5% royalty buyable at $500,000 (0.5%) and $2.5M (1.0%)

#criticalminerals #titanium #vanadium #fertilizer #phosphate #mintwit

District Copper $DCOP.v is targeting BC’s next big #copper discovery in the Quesnel Trough, Canada's largest mineral belt.

Copper Keg, 20 km from Teck’s Highland Valley (~300M lbs Cu/year), shows a gossan zone with significant discovery potential.

Exploration is underway.

$RAMP.v was trading at 0.145, exploring for #nickel in a #uranium district, June 2024. They struck #gold, literally. A high grade intercept (73.55 g/t Au) sent the stock soaring to 0.90 in a week.

$ISP.cn (CSE) is adjacent, with a $5.8m market cap, getting ready to drill. 👇

We are starting to buy: CSE: $ISP.cn $ISP

Market cap: C$5.8M

💵$975,000 raise complete

⛏️Adjacent to $RAMP.v's Rottenstone gold discovery, sending $RAMP to a $51 million market cap

🎯Drill program imminent

📢German marketing hired

📈Bullish Price and Volume action

We are starting to buy: CSE: $ISP.cn $ISP

Market cap: C$5.8M

💵$975,000 raise complete

⛏️Adjacent to $RAMP.v's Rottenstone gold discovery, sending $RAMP to a $51 million market cap

🎯Drill program imminent

📢German marketing hired

📈Bullish Price and Volume action

$DCOP.v Good to see District Copper, 20km from Teck, back on the radar.

Trading at 0.075, 27M shares outstanding, well held, with a market cap of ~$2M and in the process of raising $750k.

Should see torque on it on hints of exploration success this summer. #copper

$CD.v is retesting the 0.19 level with heightened buying today. A break through 0.20 should confirm a new bullish cycle with the potential for fresh 52-week highs.

Time to revisit this potential giant in the making.

The company’s 2025 plans are particularly bullish, with a focus on testing high-grade #copper potential following 2024 results of 2.9 meters at 4.54% copper.

Geophysical surveys identified strong conductors, signaling significant copper mineralization to be drill-tested this summer.

Additionally, Cantex will explore #gold and #silver-copper anomalies across the claim block, further enhancing the project’s multi-commodity upside.

With mineralization open along strike and at depth, a market cap still under $25 million, and Fipke’s proven track record, $CD.V remains a prime opportunity for investors seeking exposure to a potential multi-decade mining operation, with striking similarities to the 130 year Broken Hill mining operation in NSW - one of the largest base metals mines in the world.

Cantex Mine Development $CD.V - An opportunity to ride the coattails of a giant mine finder.

Market Capitalization: $17.7 million CAD

Charles Fipke, CEO and founder of Cantex, is a philanthropist, a thoroughbred horse aficionado and has devoted his life to the discovery of giant mineral deposits using sound science, raw experience and a passion that never quits.

In 1991 he and partner Stewart Blusson hit the motherlode: They found the Ekati deposit, which became Canada’s first diamond mine and remains one of the richest diamond discoveries ever made.

The Ekati find made Mr. Fipke a prospecting legend.

Mr. Fipke became a very wealthy man as shares of his company, Dia Met Minerals Ltd., soared through the roof.

Dia Met was sold to mining giant BHP Billiton Ltd in 2001, but Mr. Fipke maintained exposure to Ekati through his 10% direct stake in the mine.

Today, Mr. Fipke has been consumed with the advancement of Cantex's giant North Rackla project - developing a thesis which could support a major mining operation - for over 14 years.

Cantex's North Rackla project in the Yukon, Canada, presents a compelling investment opportunity as a potential modern analogue to Australia’s legendary Broken Hill deposit - the world’s largest silver-lead-zinc mine.

Both Broken Hill and North Rackla are hosted in Proterozoic-aged rocks with manganese-enriched, high-grade silver-lead-zinc sulphide mineralization, aligning with a Sedex or Broken Hill Type (BHT) genesis.

Broken Hill’s massive sulphide lenses averaged 10–15% lead, 10–12% zinc, and 200–300 g/t silver, while North Rackla’s Main Zone boasts intercepts such as 9 meters of 34.08% Pb-Zn and 96 g/t Ag (YKDD24-315), with historical averages exceeding 20% Pb-Zn and 100 g/t Ag over 9-meter widths.

Broken Hill’s 8 km strike length and 2 km depth made it a giant, producing 200 million tonnes of ore over 130+ years.

North Rackla’s current 2.65 km strike length (up 300 meters in 2024) remains open along strike and at depth (intersected at 700 meters), with hypotheses of a copper-rich central feeder zone suggesting it could double in size, approaching Broken Hill’s scale over time.

With 75,000 meters drilled across 260 holes, North Rackla’s Main Zone and GZ Zone already demonstrate exceptional grades and widths (e.g., 25.04 meters of 4.62% Pb-Zn and 18 g/t Ag).

The project’s 14,077-hectare land package offers untapped targets (e.g., Copper and Northern Areas), suggesting significant resource upside.

If exploration continues to expand the deposit - potentially doubling its strike length - it could support a multi-decade operation akin to Broken Hill.

Investors have an opportunity to jump into a story that is well over a decade in the making, as Chuck, and the company, zero in on defining what could be a world class deposit.

At 0.14/share and a market capitalization of under $20 million, we're going to say this looks like a generational opportunity.

Let's follow up on $GOT.v brought to you on May 4th at 0.80. Ran to $2.85 mid-Feb before a premature selloff, hitting $1.30 on April 7th before rebounding to $2.10 on Friday.

FYI ask Grok "how many ounces of gold on Goliath's Surebet property" 😉

https://t.co/1jDR0nffMb

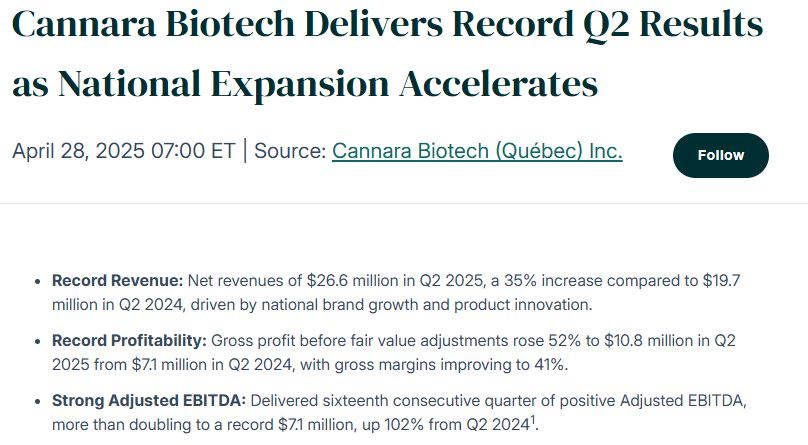

If you think Canadian cannabis is dead, look at these results from Cannara Biotech $LOVE.V

All metrics are up and to the right! Revenue +35%, gross profit +52%, adjusted EBITDA +102%, net income of $3.3M vs a $3.4M loss last year. Impressive execution!

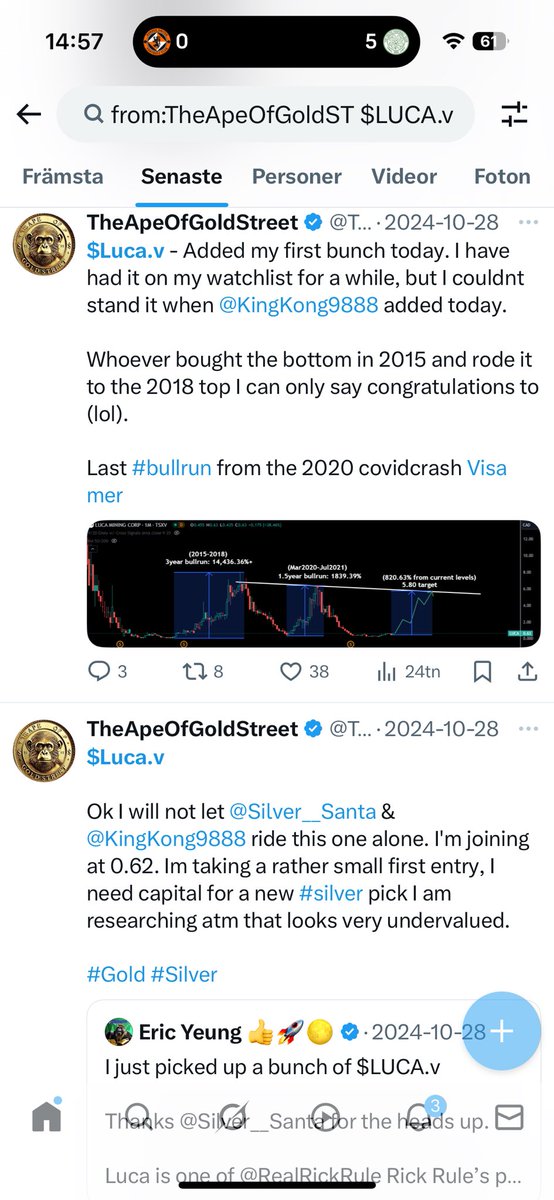

$LUCA.v - Luca Mining

Given to you 150%+ ago.

0.62 to 1.58 in 6months. Still a lot of upside ahead IMO.

I couldn’t ignore the story after @Silver__Santa@AllStreetsWolf@KingKong9888@JulesInvest was snatching shares left and right in this money printing machine. (yea Wolf was first of us all ofcourse)

That’s what we do, we recognize good companies when they arise.

Anyone “guru” that keeps promoting the same old crap no matter priceaction/performance or what’s happening in the sector regarding new diamonds (like LUCA) rising, is just a paid hustler. When a good story comes along you have to jump onboard and LUCA was a no brainer.

Building a portfolio and staying locked into the same stocks no matter what, without adjusting for drilling results, company performance, or recognizing new high-potential players you should be investing in is an expensive mistake.

You need flexibility in this sector, otherwise you’ll end up suffering.

I’ve left so many stocks during the last 24 months. And I’m always open to rotate capital into whatever I believe in. I’m aswell open to leave stocks I believe in if they are not performing.

The only stocks I refuse to leave even though silver jrs is till underperforming are $DEF.v $AAG.v $EQTY.v because I “know “ they will be among the top10 best performance in the sector when #Silver finally runs. (It’s coming this year I’m sure)

Until then I try to have good positions in $HSTR.v $LUCA.v $CERT.v $ITR.v as these quality jr producers is printing money both for themself, and for me as a shareholder thanks to ripping +150-300% the last 12 months on rising #Gold price combined with actual deliverance from them.

I will keep trimming profits after good runs on them and I will keep re-invest that capital into the best #Silver #bullrunners on weakness.

On a side note I have the must own plays in $RDG.v and $MMA.v .. they will grow, just wait and see.

$RDU.v is another ignored good case, I’ve been having stink bids all week at 0.105 but they refuse to fill me. I’m playing a permit NR and expecting their Tierra Roja project to create very surprising upside as soon as they can start drill it asap after permits is in place. R/R down here will most likely give us a fast value-booster all of a sudden imo. Atleast I’m betting on it. Don’t ignore the gold they already have proven 😜

For fun I have $ASHL.cn - Nanopick at $2m that currently seems to swing 50% up and down. I think it should be worth 3-4X current Mcap just by watching their neighbours recent news, they hitting discoveries left and right in that area.

Long journey ahead, but this can be a very fun run up story if the company can deliver and prove their assets sits on the goods. (@AshleyGoldCorp are you sitting on the goods? 🫣)

#Gold #Silver #Copper

Some of my best performing stocks have been special situations.

Spin-offs, an internal pricing increase, turnarounds, activism and regulatory changes.

A new special situation that I am exploring is “delayed financials.”

When a company has an issues filing their financials the stock tends to collapse.

Investors have no idea what is going on. They are in the dark. The company goes silent and you have no idea what is going on financially with an enterprise you bought.

In these situations the stock price tends to fall. Trading liquidity dries up as investors run to the exit.

The interesting part about these situations is that it provides a buying opportunity for savvy investors.

That is the type of situation that I am writing about today.

On November 7th, 2024, this company’s long-time auditor was bought out. The company then employed the buying firm as their new auditor.

On December 17th, 2024, the new auditor identified material weakness in the financials.

Since then the company has not filed their annual report of their Q1 financials.

In addition, the stock dropped from $22 dollars per share to a mere $11 dollars and change today.

Now here is where things get really interesting.

The company has a market cap of $162 million. They have cash and investment securities of $144 million and zero debt.

The enterprise value is a mere $18.4 million.

An $18.4 million enterprise value for a company that has generated $113 million of revenues, $15.1 million of operating income and $22.6 million of free cash flow. These financial figures are in the trailing twelve months before financials were delayed.

What is even more interesting is the amount of cash the company has generated since their financials have gotten delayed.

The last time the company reported was Q3 2024.

On Q3 2024 the company had cash and investment securities of $116.5 million.

The company reported a balance sheet for Q1 2025. In the balance sheet they had $144 million of cash and investment securities.

This means they have generated $27.4 million of cash in two quarters.

What is even more interesting, the company owns two different properties.

In aggregate the properties total 352k sf and 100 acres.

One of the properties in Orlando, Florida is likely worth more than the entire enterprise value of the company.

This company is family controlled. But the executive chairman is 94 years old.

And there is a good chance when he passes away the company is sold off.

Or an even better chance that the younger generation who takes over the company, allocates capital in a more prudential fashion, though dividends and buybacks.

Either way.

The stock is dirt cheap. It has sold off. But still generates significant cash flow.

There is a huge margin of safety here and the catalyst is the company getting current on their financials.

And this appears to be happening as they recently hired a new auditor.

Full article in my bio