@ShawarmaCapital $MRLN having to give away deeply out of the money warrants (at $6.67) is a clear sign of distress. Business is a high school science project hemorrhaging cash with zero commercial value. Those warrants will be out of the money soon.

$LYTS Customer Texaco announced a large rebrand of signage and lighting. $20-26M opportunity for LYTS (typically costs $15-20k per location, Texaco has 1,300 US stations). https://t.co/DQCSqxSTeb

@thudderwicks It would make a lot of strategic sense for both parties. $WH is trading at substantial discount to $CHH despite very similar business profiles, end-market exposure and growth prospects.

$DCGO Management guidance assumes $180M NYC contract will be fully-ramped in Q3 is very ambitious given how such municipal contracts are almost always delayed. Regardless the margin structure of this work and that of the ongoing business is much lower w lucrative covid work ended

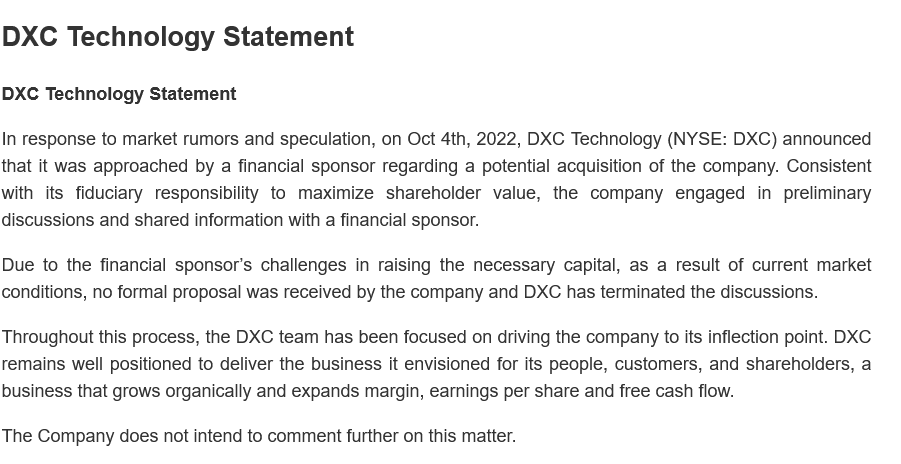

@Turnaround_MD Sales dropping double digits. Pulled forward sales in the first place so getting worse. Noted "no formal proposal received." Total con management. This is the 2nd failed go-private attempt. No more levers to pull or assets to sell.

$DXC Fundamentals falling apart so management claimed someone was trying to acquire them but never provided any details. Now owning up to this fiction. It's amazing these games still go on. Stock should be down 20%.

$KBR Very favorable development missed by the market during this slow week--protest period to dispute the $20B HomeSafe program just passed. This removes any further delays, ramping next year, equating to >10% annual rev growth to KBR over next 10 years.

https://t.co/PJJv8o2ihx

@KatzCapital Thank you for the note. Still own it and believe it remains quite compelling here at nearly a 10% FCF yield with a growing backlog and expanding margins. Management is executing well with favorable industry tailwinds.

$HGTY Taking on State Farm's low margin old car policies to show topline growth. The market for low-end vintage cars is mature and unprofitable yet $HGTY trades at over 150x EV/ adj EBITDA. Growth deceleration and losses will likely correct this stock.

$SLVM 15% of sales to Russia but nearly all its European production capacity is located in Russia. Euro accounts for 30% of earnings. Highly levered with large and rising fixed costs = potential disaster for the equity yet stock is only down 10% since invasion.

$TTCF Major declines at largest customers in Q3 ($COST, $WMT). No longer in many $COST and Sam's Club's freezers. You don't get a second shot if you don't perform in mass, particularly in the frozen category. These 3 account for 2/3 of total TTCF sales. An ominous trend.

Agreed. This should definitely help get it on the radar of other funds and provide some trading support. Here's another presentation with additional background on the $TTSH setup. https://t.co/vpREMBOwgF

$REAL Just checked their Glassdoor reviews. Grain of salt but these are the absolute worst I've ever seen. Morale sounds abysmal. These are some snippets from different reviews just over the last 30 days. This is an acute problem for a highly human capital intensive business.