WARREN BUFFETT JUST SENT WHAT COULD BE HIS LAST MESSAGE TO BERKSHIRE HATHAWAY $BRK.B SHAREHOLDERS AS CEO OF THE COMPANY

Here is the full and entire 8 page press release Warren Buffett just released ⬇️⬇️

To My Fellow Shareholders:

I will no longer be writing Berkshire’s annual report or talking endlessly at the annual meeting. As the British would say, I’m “going quiet.”

Sort of.

Greg Abel will become the boss at yearend. He is a great manager, a tireless worker and an honest communicator. Wish him an extended tenure.

I will continue talking to you and my children about Berkshire via my annual Thanksgiving message. Berkshire’s individual shareholders are a very special group who are unusually generous in sharing their gains with others less fortunate. I enjoy the chance to keep in touch with you. Indulge me this year as I first reminisce a bit. After that, I will discuss the plans for distribution of my Berkshire shares. Finally, I will offer a few business and personal observations.

* * * * * * * * * * * *

As Thanksgiving approaches, I’m grateful and surprised by my luck in being alive at 95. When I was young, this outcome did not look like a good bet. Early on, I nearly died.

It was 1938 and Omaha hospitals were then thought of by its citizens as either Catholic or Protestant, a classification that seemed natural at the time.

Our family doctor, Harley Hotz, was a friendly Catholic who made house calls toting a black bag. Dr. Hotz called me Skipper and never charged much for his visits. When I experienced a bad bellyache in 1938, Dr. Hotz came by and, after probing a bit, told me I would be OK in the morning.

He then went home, had dinner and played a little bridge. Dr. Hotz couldn’t, however, get my somewhat peculiar symptoms out of his mind and later that night he dispatched me to St. Catherine’s Hospital for an emergency appendectomy. During the next three weeks, I felt like I was in a nunnery, and began enjoying my new “podium.” I liked to talk – yes, even then – and the nuns embraced me.

To top things off, Miss Madsen, my third-grade teacher, told my 30 classmates to each write me a letter. I probably threw away the letters from the boys but read and reread those from the girls; hospitalization had its rewards.

The highlight of my recovery – which actually was dicey for much of the first week – was a gift from my wonderful Aunt Edie. She brought me a very professional-looking fingerprinting set, and I promptly fingerprinted all of my attending nuns. (I was probably the first Protestant kid they had seen at St. Catherine’s and they didn’t know what to expect.)

My theory – totally nutty, of course – was that someday a nun would go bad and the FBI would find that they had neglected to fingerprint nuns. The FBI and its director, J. Edgar Hoover, had become revered by Americans in the 1930s, and I envisioned Mr. Hoover, himself, coming to Omaha to inspect my invaluable collection. I further fantasized that J. Edgar and I would quickly identify and apprehend the wayward nun. National fame seemed certain.

Obviously, my fantasy never materialized. But, ironically, some years later it became clear that I should have fingerprinted J. Edgar himself as he became disgraced for misusing his post.

Well, that was Omaha in the 1930s, when a sled, a bicycle, a baseball glove and an electric train were coveted by me and my friends. Let’s look at a few other kids from that era, who grew up very nearby and greatly influenced my life but of whom I was for long unaware.

I’ll begin with Charlie Munger, my best pal for 64 years. In the 1930s, Charlie lived a block away from the house I have owned and occupied since 1958.

Early on, I missed befriending Charlie by a whisker. Charlie, 6 ⅔ years older than I, worked in the summer of 1940 at my grandfather’s grocery store, earning $2 for a 10-hour day. (Thrift runs deep in Buffett blood.) The following year I did similar work at the store, but I never met Charlie until 1959 when he was 35 and I was 28.

After serving in World War II, Charlie graduated from Harvard Law and then moved permanently to California. Charlie, however, forever talked of his early years in Omaha as formative. For more than 60 years, Charlie had a huge impact on me and could not have been a better teacher and protective “big brother.” We had differences but never had an argument. “I told you so” was not in his vocabulary.

In 1958, I bought my first and only home. Of course, it was in Omaha, located about two miles from where I grew up (loosely defined), less than two blocks from my in-laws, about six blocks from the Buffett grocery store and a 6-7-minute drive from the office building where I have worked for 64 years.

Let’s move on to another Omahan, Stan Lipsey. Stan sold the Omaha Sun Newspapers (weeklies) to Berkshire in 1968 and a decade later moved to Buffalo at my request. The Buffalo Evening News, owned by a Berkshire affiliate, was then locked in a battle to the death with its morning competitor who published Buffalo’s only Sunday paper. And we were losing.

Stan eventually built our new Sunday product, and for some years our paper – formerly hemorrhaging cash – earned over 100% annually (pre-tax) on our $33 million investment. This was important money to Berkshire in the early 1980s.

Stan grew up about five blocks from my home. One of Stan’s neighbors was Walter Scott, Jr. Walter, you will remember, brought MidAmerican Energy to Berkshire in 1999. He was also a valued Berkshire director until his death in 2021 and a very close friend. Walter was Nebraska’s philanthropic leader for decades and both Omaha and the state carries his imprint.

Walter attended Benson High School, which I was scheduled to attend as well – until my dad surprised everyone in 1942 by beating a four-term incumbent in a Congressional race. Life is full of surprises.

Wait, there’s more.

In 1959, Don Keough and his young family lived in a home located directly across the street from my house and about 100 yards away from where the Munger family had lived. Don was then a coffee salesman but was destined to become president of Coca-Cola as well as a devoted director of Berkshire.

When I met Don, he was earning $12,000 a year while he and his wife Mickie were raising five children, all destined for Catholic schools (with tuition requirements).

Our families became fast friends. Don came from a farm in northwest Iowa and graduated from Omaha’s Creighton University. Early on, he married Mickie, an Omaha girl. After joining Coke, Don went on to become legendary around the globe.

In 1985, when Don was president of Coke, the company launched its ill-fated New Coke. Don made a famous speech in which he apologized to the public and reinstated “Old” Coke. This change of heart took place after Don explained that Coke incoming mail addressed to “Supreme Idiot” was promptly delivered to his desk. His “withdrawal” speech is a classic and can be viewed on YouTube. He cheerfully acknowledged that, in truth, the Coca-Cola product belonged to the public and not to the company. Sales subsequently soared.

You can watch Don on CharlieRose(.)com in a wonderful interview. (Tom Murphy and Kay Graham have a couple of gems as well.) Like Charlie Munger, Don forever remained a Midwestern boy, enthusiastic, friendly and American to the core.

Finally, Ajit Jain, born and raised in India, as well as Greg Abel, our Canadian CEO-to-be, each lived in Omaha for several years late in the 20th Century. Indeed, in the 1990s, Greg lived only a few blocks away from me on Farnam Street, though we never met at the time.

Can it be that there is some magic ingredient in Omaha’s water?

* * * * * * * * * * * *

I lived a few teenage years in Washington, DC (when my dad was in Congress) and in 1954 I took what I thought would be a permanent job in Manhattan. There I was treated wonderfully by Ben Graham and Jerry Newman and made many life-long friends. New York had unique assets – and still does. Nevertheless, in 1956, after only 1½ years, I returned to Omaha, never to wander again.

Subsequently, my three children, as well as several grandchildren, were raised in Omaha. My children always attended public schools (graduating from the same high school that educated my dad (class of 1921), my first wife, Susie (class of 1950) as well as Charlie, Stan Lipsey, Irv and Ron Blumkin, who were key to growing Nebraska Furniture Mart, and Jack Ringwalt (class of 1923), who founded National Indemnity and sold it to Berkshire in 1967 where it became the base upon which our huge P/C operation was constructed.

* * * * * * * * * * * *

Our country has many great companies, great schools, great medical facilities and each definitely has its own special advantages along with talented people. But I feel very lucky to have had the good fortune to make many lifelong friends, to meet both of my wives, to receive a great start in education at public schools, to meet many interesting and friendly adult Omahans when I was very young, and to make a wide variety of friends in the Nebraska National Guard. In short, Nebraska has been home.

Looking back I feel that both Berkshire and I did better because of our base in Omaha than if I had resided anywhere else. The center of the United States was a very good place to be born, to raise a family, and to build a business. Through dumb luck, I drew a ridiculously long straw at birth.

* * * * * * * * * * * *

Now let’s move on to my advanced age. My genes haven’t been particularly helpful – the family’s all-time record for longevity (admittedly family records get fuzzy as you work backwards) was 92 until I came along. But I have had wise, friendly and dedicated Omaha doctors, starting with Harley Hotz, and continuing to this day. At least three times, my life has been saved, each with doctors based within a few miles from my home. (I have given up fingerprinting nurses, however. You can get away with many eccentricities at 95 . . . . . but there are limits.)

* * * * * * * * * * * *

Those who reach old age need a huge dose of good luck, daily escaping banana peels, natural disasters, drunk or distracted drivers, lightning strikes, you name it.

But Lady Luck is fickle and – no other term fits – wildly unfair. In many cases, our leaders and the rich have received far more than their share of luck – which, too often, the recipients prefer not to acknowledge. Dynastic inheritors have achieved lifetime financial independence the moment they emerged from the womb, while others have arrived, facing a hell-hole during their early life or, worse, disabling physical or mental infirmities that rob them of what I have taken for granted. In many heavily-populated parts of the world, I would likely have had a miserable life and my sisters would have had one even worse.

I was born in 1930 healthy, reasonably intelligent, white, male and in America. Wow! Thank you, Lady Luck. My sisters had equal intelligence and better personalities than I but faced a much different outlook. Lady Luck continued to drop by during much of my life, but she has better things to do than work with those in their 90s. Luck has its limits.

Father Time, to the contrary, now finds me more interesting as I age. And he is undefeated; for him, everyone ends up on his score card as “wins.” When balance, sight, hearing and memory are all on a persistently downward slope, you know Father Time is in the neighborhood.

I was late in becoming old – its onset materially varies – but once it appears, it is not to be

denied.

To my surprise, I generally feel good. Though I move slowly and read with increasing difficulty, I am at the office five days a week where I work with wonderful people. Occasionally, I get a useful idea or am approached with an offer we might not otherwise have received. Because of Berkshire’s size and because of market levels, ideas are few – but not zero.

* * * * * * * * * * * *

My unexpected longevity, however, has unavoidable consequences of major importance to my family and the achievement of my charitable objectives.

Let’s explore them.

What Comes Next

My children are all above normal retirement age, having reached 72, 70 and 67. It would be a mistake to wager that all three – now at their peak in many respects – will enjoy my exceptional luck in delayed aging. To improve the probability that they will dispose of what will essentially be my entire estate before alternate trustees replace them, I need to step up the pace of lifetime gifts to their three foundations. My children are now at their prime in respect to experience and wisdom but have

yet to enter old age. That “honeymoon” period will not last forever.

Fortunately, a course correction is easy to execute. There is, however, one additional factor to consider: I would like to keep a significant amount of “A” shares until Berkshire shareholders develop the comfort with Greg that Charlie and I long enjoyed. That level of confidence shouldn’t take long. My children are already 100% behind Greg as are the Berkshire directors.

All three children now have the maturity, brains, energy and instincts to disburse a large fortune. They will also have the advantage of being above ground when I am long gone and, if necessary, can adopt policies both anticipatory and reactive to federal tax policies or other developments affecting philanthropy. They may well need to adapt to a significantly changing world around them. Ruling from the grave does not have a great record, and I have never had an urge to do

Fortunately, all three children received a dominant dosage of their genes from their mother. As the decades have passed, I have also become a better model for their thinking and behavior. I will never, however, achieve parity with their mother.

My children have three alternate trustees in case of any premature deaths or disabilities. The alternates are not ranked or tied to a specific child. All three are exceptional humans and wise in the ways of the world. They have no conflicting motives.

I have assured my children that they do not need to perform miracles nor fear failures or disappointments. These are inevitable, and I have made my share. They simply need to improve somewhat upon what generally is achieved by government activities and/or private philanthropy, recognizing these other methods of redistribution of wealth have shortcomings as well.

Early on, I contemplated various grand philanthropic plans. Though I was stubborn, these did not prove feasible. During my many years, I’ve also watched ill-conceived wealth transfers by political hacks, dynastic choices and, yes, inept or quirky philanthropists.

If my children simply do a decent job, they can be certain that their mother and I would be pleased. Their instincts are good and they each have had years of practice with very small sums initially that have been irregularly increased to more than $500 million annually.

All three like working long hours to help others, each in their own way.

* * * * * * * * * * * *

The acceleration of my lifetime gifts to my children’s foundations in no way reflects any change in my views about Berkshire’s prospects. Greg Abel has more than met the high expectations I had for him when I first thought he should be Berkshire’s next CEO. He understands many of our businesses and personnel far better than I now do, and he is a very fast learner about matters many CEOs don’t even consider. I can’t think of a CEO, a management consultant, an academic, a member of government – you name it – that I would select over Greg to handle your savings and mine.

Greg understands, for example, far more about both the upside potential and the dangers of our P/C insurance business than do a great many long-time P/C executives. My hope is that his health remains good for several decades. With a little luck, Berkshire should require only five or six CEOs over the next century. It should particularly avoid those whose goal is to retire at 65, to become lookat-me rich or to initiate a dynasty

One unpleasant reality: Occasionally, a wonderful and loyal CEO of the parent or a subsidiary will succumb to dementia, Alzheimer’s or another debilitating and long-term disease.

Charlie and I encountered this problem several times and failed to act. This failure can be a huge mistake. The Board must be alert to this possibility at the CEO level and the CEO must be alert to the possibility at subsidiaries. This is easier said than done; I could cite a few examples from the past at major companies. Directors should be alert and speak up is all that I can advise.

During my lifetime, reformers sought to embarrass CEOs by requiring the disclosure of the compensation of the boss compared to what was being paid to the average employee. Proxy statements promptly ballooned to 100-plus pages compared to 20 or less earlier.

But the good intentions didn’t work; instead they backfired. Based on the majority of my observations – the CEO of company “A” looked at his competitor at company “B” and subtly conveyed to his board that he should be worth more. Of course, he also boosted the pay of directors and was careful who he placed on the compensation committee. The new rules produced envy, not moderation.

The ratcheting took on a life of its own. What often bothers very wealthy CEOs – they are human, after all – is that other CEOs are getting even richer. Envy and greed walk hand in hand. And what consultant ever recommended a serious cut in CEO compensation or board payments?

* * * * * * * * * * * *

In aggregate, Berkshire’s businesses have moderately better-than-average prospects, led by a few non-correlated and sizable gems. However, a decade or two from now, there will be many companies that have done better than Berkshire; our size takes its toll.

Berkshire has less chance of a devastating disaster than any business I know. And, Berkshire has a more shareholder-conscious management and board than almost any company with which I am familiar (and I’ve seen a lot). Finally, Berkshire will always be managed in a manner that will make its existence an asset to the United States and eschew activities that would lead it to become a supplicant. Over time, our managers should grow quite wealthy – they have important responsibilities – but do not have the desire for dynastic or look-at-me wealth.

Our stock price will move capriciously, occasionally falling 50% or so as has happened three times in 60 years under present management. Don’t despair; America will come back and so will Berkshire shares.

A Few Final Thoughts

One perhaps self-serving observation. I’m happy to say I feel better about the second half of my life than the first. My advice: Don’t beat yourself up over past mistakes – learn at least a little from them and move on. It is never too late to improve. Get the right heroes and copy them. You can start with Tom Murphy; he was the best.

Remember Alfred Nobel, later of Nobel Prize fame, who – reportedly – read his own obituary that was mistakenly printed when his brother died and a newspaper got mixed up. He was horrified at what he read and realized he should change his behavior.

Don’t count on a newsroom mix-up: Decide what you would like your obituary to say and live the life to deserve it.

Greatness does not come about through accumulating great amounts of money, great amounts of publicity or great power in government. When you help someone in any of thousands of ways, you help the world. Kindness is costless but also priceless. Whether you are religious or not, it’s hard to beat The Golden Rule as a guide to behavior.

I write this as one who has been thoughtless countless times and made many mistakes but also became very lucky in learning from some wonderful friends how to behave better (still a long way from perfect, however). Keep in mind that the cleaning lady is as much a human being as the Chairman.

* * * * * * * * * * * *

I wish all who read this a very happy Thanksgiving. Yes, even the jerks; it’s never too late to change. Remember to thank America for maximizing your opportunities. But it is – inevitably – capricious and sometimes venal in distributing its rewards.

Choose your heroes very carefully and then emulate them. You will never be perfect, but you can always be better.

I am particularly excited by the new mechanism by @_Dave__White_ & @danrobinson because we can now build & deploy a Reth-based L2 Sequencer that enables L2 appchains to capture their own MEV.

Want to implement the MEV taxes on Reth? Reach out?

If you want to understand Asian geopolitics today, this is an absolute must-watch.

This is George Yeo, who was a Singaporean cabinet minister during 21 years, including Minister for Foreign Affairs during 7 years. In my humble opinion, very few people out there have such a subtle understanding of geopolitics in Asia as he does.

Here's a quick summary of what he says:

The US has little knowledge of China

He says that "the US political system is decentralized and because of the need to win votes, it goes through emotional phases and is entering such a phase now where China is demonized out of mass emotion. There's some manipulation behind the scenes, but it's not based on knowledge."

To him, the US "don't understand the nature of China", the fact that China "is constantly building walls around itself because it is happy in its own homogeneity". He says it is wrong for the US to believe that "China wants to displace them as the top dog in the world" and "trying to contain China, even pull it down" as a result. Not only is this a wrong understanding of China's objectives but the US "may exhaust itself in the process and I don't think it will succeed". He says that with its tariffs and sanctions the US risks making the same mistake as China's Qing dynasty and "become very weak".

He believes the primacy of the US dollar will break, and that US actions are "bringing forward that day"

He says that "the key event will be when the primacy of the US dollar breaks. We all know it's going to break sometime or other because it's abnormal. If it is 30 years from now, well, let's drink and be merry. But if it's five years, well, we've got to calculate, right? Do we know when the cookie will crumble? We don't know. But the way the US is moving is bringing forward that day."

It's "bringing forward that day" because "they try to control countries by sanctions" and as a result more and more countries put counter-measures in place, putting themselves out of the grasp of the US.

China is not in trouble and "overcapacity" is "information warfare"

He says "there's information warfare against China" and that he "doesn't think" China is in trouble. "Look at the factories, look at the EVs, look at how terrified the Europeans are, accusing China of having overcapacity. I mean, how can you blame China for overcapacity when you have, when you're taking liberties with yourself, having long summers and working short hours and you say no, no, no, no, no, you are working too hard! There are consequences. If families take liberties with their children, with themselves, there's consequences."

He believes that Asian societies' "wholesomeness" is an advantage versus the West

"Look at Asia, look at China, look at Southeast Asia, look at India. There are people who are hardworking, who are obsessed over their children, who want to have of them a higher education, in order that the kids will have a better education, better health, a better life. [...] They'll do well and we're lucky to be in the part of the world where strange values have not taken over societies. [...] Why is America such a big market for drugs today? And I was watching the Eurovision contest... [...] Parts of it, almost satanic. But it's now part of the fashion in most of Europe. What is happening?

PM Lee talked about how we should keep all these woke things away from us as much as possible. I fully agree with him. Keep our societies wholesome. Keep our families intact. I mean, AI is very important, but AI cannot answer moral questions for us. In the end, it is every individual, every child who must make the choice. Be immersed in technology. Make use of it. But have our own sense of what it means to be a human being. So if we use that as a template to judge human society, I say we are very lucky to be in a part of the world where society is by and large wholesome and will do well."

It's critical for ASEAN to stick together and not be balkanized, which is what the US is trying to do with the Philippines

"If we [ASEAN] don't stick together, we'll be balkanized and instead of becoming neighbours, become clients of big powers. Instead of using them, they make use of us. There's always a threat.

Look at the Philippines now. The Philippines have legitimate disputes with China. Both sides have their cases. The Americans see an opportunity there. And jump in, and bring in the Japanese. And now Philippine politics is caught up in this [...]

[China and the Philippines] had an agreement, a gentleman's agreement with Duterte, which Marcos has repudiated. So OK, so they must find a new way to equilibrium. And make use of the Americans and not be made use of by the Americans. But it's very difficult when you try to make use of a big power, you end up being made use of by them."

Most countries in ASEAN do not want China to be an enemy

For instance he says "Vietnam has made a very important decision to go with China": "it was not well reported, but Vietnam has agreed that Hanoi will be linked to Kunming and Nanning by high-speed rail. This is big because each connection is tens of billions of dollars. And will change the topological configuration of logistics and supply chain and human movement for decades to come."

Same with Indonesia, noting that "Prabowo's first visit [was] to China" and that when he met Xi Jinping "it was Xiao Di talking to Da Ge. A little brother talking to big brother. But when we went to Japan, then it's brother talking to brother."

He adds: "Look at the other countries, Laos, Cambodia, Thailand, Malaysia, Brunei. No one wants China to be an enemy. And the Americans don't understand this, yet. That because China is getting bigger and bigger for us, all of us want the Americans to be in the room. But if the Americans say no, you have to choose between China and us, then they say no, we can't. How can we choose? I mean, China is where our bread is buttered, you know."

THIS WEEK’S HIGHLIGHTS⚠️

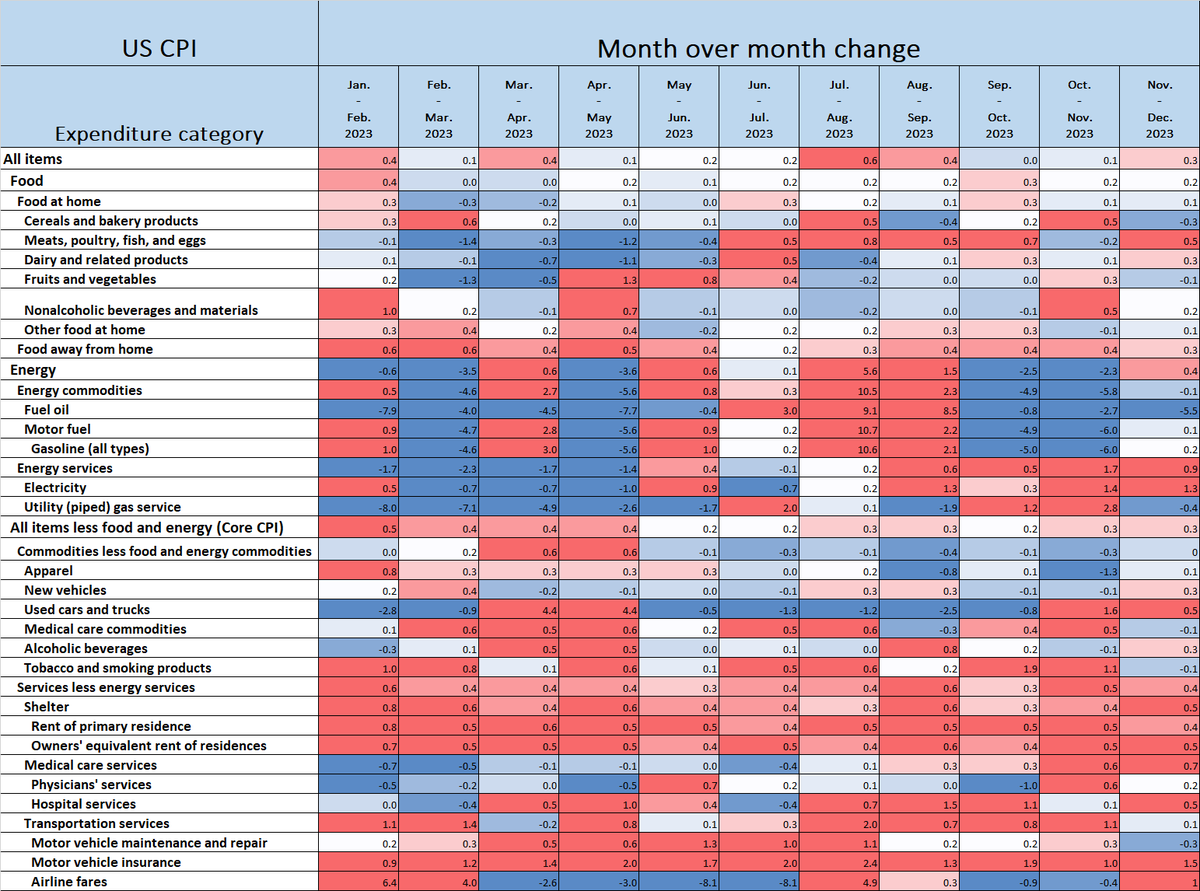

1. Headline CPI came hotter than anticipated at 3.4% YoY (Exp. 3.2%, Prev. 3.1%), 0.3% MoM (Exp. 0.2%, Prev. 0.1%). Core CPI came in at 3.9% YoY (Exp. 3.8%, Prev. 4%) and 0.3% MoM (Exp. 0.3%, Prev. 0.3%).

Deeper dive

3 month annualized CPI is now running at 3.3% while 6 month annualized consumer prices are rising at 3.2%, still well above the Federal Reserve’s 2% target.

Energy prices rose 0.4% MoM (-2% YoY) in December after months of deflation. Electricity and gasoline accelerated with gasoline up 0.2% MoM (Prev. 6%). Core services remain hot at 0.4% MoM (annualized 4.9%) and core goods were flat after 6 months of price declines.

Shelter contributions accelerated to 0.5% MoM (Prev. 0.4%) and contributed over half of the monthly increase in total CPI. Shelter is up 6.2% YoY. Used cars and trucks rose 0.5% MoM (Prev 1.5%). Motor vehicle insurance continues full steam ahead up 20.3% YoY and increasing 1.5% MoM. It's 6 month annualized pace is increasing at a staggering 22.2%.

US CPI 2023 Heatmap (MoM)

Simply explained

CPI measures the change in prices for consumers in a fixed basket of good and services. It is not the Federal Reserve’s preferred measure of inflation (which is PCE).

Core CPI strips out energy and food components of CPI which are more volatile and is preferred by the Fed as it provides a better idea of underlying inflation.

Annualized readings are what year over year inflation would be if the current monthly rate of inflation was applied over a 12 month period. 3 month annualized would take the average rate over 3 months and apply this over 12.

2. Offsetting the hotter than expected CPI print, US PPI declined in December for the third consecutive month, coming in at -0.1% MoM (Exp. +0.1%, Prev. -0.1%). This firmed up market expectations of a Fed rate cut in March. On a year over year basis PPI came in at 1% (Exp. 1.3%, Prev. 0.8%) while core PPI (excluding energy and food) came in at 1.8% (Exp. 1.9%, Prev. 2%) YoY. On a monthly basis, core producer prices remained unchanged (0% MoM).

Simply explained

The producer price index measures price changes for producers of goods and services. As this is an observation earlier in the supply chain it is said to lead consumer prices as price changes faced by producers tend to then be passed on to consumers.

Furthermore, some metrics of the PPI report feed directly into PCE (the Fed’s preferred inflation measure) and make it more likely that this may come in on the softer side.

3. The US and UK fired missiles at Houthi rebels in Yemen over recent attacks on ships in the Red Sea, an escalation of conflict in the Middle East.

Simply explained

The Red Sea sees over 10% of global marine trade and is thus a vital part of the world’s economy continuing to function. While, hopefully, the conflict does not escalate further it has the possibility to increase shipping costs (and already is doing so) as ships divert their course to prevent the possibility of an attack. The alternative is rerouting round the Cape of Good Hope in Africa, a substantially longer and more expensive journey for ships travelling between Asia and Europe.

Cape of Good Hope vs Suez Canal (Red Sea)

4. The US fiscal deficit for the first quarter of the fiscal year 2024 (the fiscal year runs from October) came in at $509 billion, substantially (21%) more than the prior year Oct-Dec period that clocked in at $421 billion. This means that the US fiscal deficit is running at a rate of over $2 trillion per year and should the pace of the current deficit accumulation continue 2024 will see largest (excluding COVID stimulus) fiscal deficit ever. At a time when the US economy has been expanding at a robust pace this is difficult to justify.

Simply explained

A fiscal deficit is the difference between what a country makes and what it spends. The US government is spending substantially more than it makes and the level at which it is currently doing so is unsustainable.

5. Initial jobless claims came in better than expected at 202K (Exp. 210K, Prev. 203K) and continuing claims also beat expectations at 1834K (Exp. 1871K, Prev. 1868K) showing continued strength in the US labor market. The US is yet to see a meaningful spike in layoffs.

Simply explained

Initial jobless claims tracks those that are filing for unemployment benefits for their first week whereas continuing claims includes those that are filing after previously already having done so. Thus, initial claims gives an idea of how many people are newly becoming unemployed (current layoffs) whereas continuing claims provides insight into how long people are remaining unemployed once they have lost their job (how hard it is to get a new job).

The US labor market remains tight but, nonetheless, it has shown some signs of loosening of late.

6. Discount window (DW) borrowing DECREASED by $53 million, now at $2.1 billion. Borrowing via the Bank Term Funding Program (BTFP) INCREASED by $5.97 billion and now stands at $147.2 billion, a new all-time high.

Deeper dive

We continue to see a clear pattern of increasing use of the BTFP after a period of muted growth/stagnation. This is the sixth consecutive increase in usage of the Bank Term Funding Program, likely due to financial institutions taking advantage of the arbitrage between what interest rates banks can take out BTFP loans at and the interest they can earn on the loan if they just leave it at the Fed, accruing the interest on reserve balance rate, essentially free money.

Simply explained

The DW and the BTFP are both means by which financial institutions can borrow 'emergency liquidity' from the Fed. The DW has been around since 1914 while the BTFP was created in response to the banking crisis in March this year. The DW offers shorter term lending (up to 90 days) than the BTFP (up to 1 year); on top of this, the BTFP is more generous in than the DW, banks can post collateral (usually in the form of US treasury bonds, agency MBS, etc) at the Fed at par value, essentially meaning price fluctuations in bank assets used as collateral are ignored by the Fed when being used as collateral. This was designed so that banks aren’t forced to sell asset portfolios at heavy losses, they can lend against them to meet immediate obligations and continue to hold. To top it off, interest on lending through the BTFP is done at 1 year overnight index swap (OIS) rate + 0.1%.

7. The Bitcoin ETF was approved by the SEC

Deeper dive

The SEC’s X (Twitter) page was hacked the prior day and a premature announcement was made. The approval was subsequently denied by the SEC before they officially announced it the following day. Bitcoin then proceeded to finish the week in the red.

8. German factory orders came in at +0.3% MoM in November, well below expectations but reporting growth nonetheless (Exp. 1.1%, Prev. -3.8%). Moreover, industrial production dropped 0.7% in November (Exp. +0.3%, Prev. -0.3%).

Simply explained

Factory orders report on the volume of orders received by manufacturers. Thus, this is a barometer for demand in the German manufacturing industry.

Industrial production measure the output of the industrial sector. The largest player in this is manufacturing, accounting for almost 80% of German industrial production.

A technical recession is two consecutive quarters of negative GDP growth.

9. Eurozone economic sentiment came in better than expected at 96.4 (Exp. 94.2, Prev. 94), marking the third consecutive monthly improvement, suggesting the Eurozone may on the cusp of a bounce in economic activity, after seeing its GDP contract 0.1% in the third quarter. However, keep in mind economic sentiment still remains more pessimistic than the historical average.

Deeper dive

Industries seeing improvement in sentiment included retail trade, services, and construction. Of the biggest Eurozone economies France and Netherlands saw a deterioration in economic sentiment while Italy, Spain and Germany all saw an improvement.

Simply explained

The economic sentiment index (ESI) is released by the European Commission. It is released on a monthly basis and is a combination of the outlook from businesses and consumers compiled into a composite index. This is done by collecting survey responses from consumers as well as businesses across multiple sectors. A reading of 100 is equal to the long term average sentiment.

10. Eurozone retail sales volumes for November fell 0.3% MoM, as expected (Prev. +0.4%) and are now down 1.1% YoY (Exp. 1.5%, Prev. -0.8%).

Simply explained

Retail sales measure the revenue and volume of sales in retail online and in brick and mortar stores. It is a barometer of consumer spending, a key driver of GDP growth.

The above 0.3% contraction is in sales volumes, this strips out the misleading effect of retail sales turnover increasing when consumers are actually purchasing less. The effects of inflation can be seen in the chart below, while amount of money spent continues to trend upwards, the volume of goods sold decreases as consumers spend more for less.

Eurozone Retail Sales

11. China remained in year-over-year deflation with CPI printing at -0.3% (Exp. -0.4%, Prev. -0.5%), while month over month CPI increased by 0.1%, the first month of price increase since September.

12. UK GDP increased by 0.3% MoM in November after falling 0.3% in the prior month. It remains to be seen if the UK fell into a technical recession in the final quarter of 2023 after the economy contracted by 0.1% in the 3rd.

Simply explained

Considered the most important measure of a country’s economic performance, GDP is the measure of the value of all goods and services produced in a given period of time.

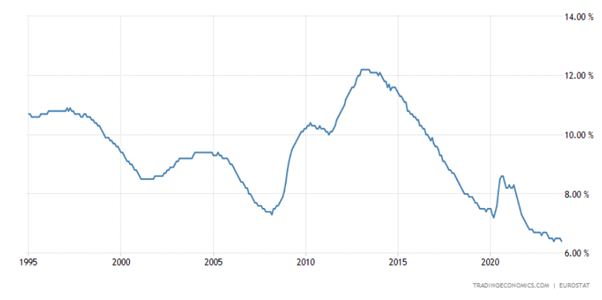

13. Eurozone unemployment fell to 6.4% (Exp. 6.5%, Prev. 6.5%), matching the low seen in June 2023. This is the lowest unemployment rate on record for the economic area.

Simply explained

The unemployment rate is the % of the labor force that are out of work and currently looking for a job. Unemployment tends to rise in recessions, something that is not currently happening in the Eurozone despite clear evidence of economic slowdown, not least a negative GDP print for the third quarter.

A severe recession in the Eurozone would inevitably lead to a rising unemployment rate; it is yet to be seen.

Eurozone unemployment rate

-

Overall a dramatic week, with tensions in the Middle East rising with the potential to further ramp up shipping costs to the SEC being hacked in the lead up to the approval of the Bitcoin ETF.

China remains in deflation as it battles the ongoing crisis stemming from the real estate sector.

The situation in Europe remains tenuous with Germany (responsible for almost 30% of Eurozone GDP) continuing to post weak economic data. The probability of technical recession in the final stretch of 2023 for Germany is substantial after GDP contracted in Q3. The latest GDP data will be released in the coming week.

Despite softening economic data in Europe, the EU labor market remains remarkably strong with unemployment at record lows; economic sentiment also continued to recover despite remaining historically pessimistic.

Markets are still pricing in 7 rate cuts by the Federal Reserve in 2024, starting with a 77% chance of a rate cut in March.

Soft PPI fed into the current narrative of rate cuts galore, despite hotter than expected CPI and the recent substantial loosening of financial conditions.

“So there are only 21 fully diluted million bitcoins, and now some of the biggest asset managers in the world are starting to aggressively compete to get some small fraction of the tens of trillions of dollars of walled garden managed assets into them.”

1/x🧵

THE JAPAN MOMENT IS NOW.

If you think crypto is crazy right now,

watch what's happening to the worlds MOST indebted #g7 country!

Forget FOMC.

Forget 3AC.

Forget Celcius.

Since 2010 I've been closely following this situation... Thanks to @Jkylebass

One of the best ways to learn about the Copper Industry is by studying the Top 10 Global Producers.

I read each of the Top 10 #Copper Producer quarterly reports so you don't have to.

Here's a thread on the most important data and themes from the world's largest players ... 🧵

Bears really coming out of the woodwork on March Philly Fed data…

I think it’s the wrong take.

A lot of people are using the 1970s as the period most similar to today…

Some are using 2000 or 2008…

We’re using 1990.

It’s a near perfect fit. Let me show you…

A thread 🧵

SVB does not deserve a bailout.

A deep look at their financial statement reveals how horrific they were at risk management.

And in my opinion incompetence explains only part of it.

Moral hazard must have been at play.

A thread.

1/

Most people don't realize how crucial Silicon Valley Bank is.

Billions of dollars in venture debt. Untold amounts of warrants and convertible notes in early-stage firms.

If SVB fails, this could be the Lehman moment for the startup world.

This has to be one of most insane parts of this saga. FTX faking an order from the Bahama regulators to sneakily withdraw funds while everything was paused, only to have the Bahama regulator say that FTX was lying!

Cygaar's helpful breakdowns #2:

A beginner's guide to reading NFT smart contracts.

I'm going to show you how to start reading smart contracts even if you don't know how to code.

One of the distinctive features of FTX was their liquidation engine. During rapid market movements, they "internalized" liquidated positions rather than simply dumping them on the market.

You can read more about this approach in their own words here:

https://t.co/cm7KXbL8xA

Scary how close SBF was to getting away with all of it.

- CPI pump to $2k ETH.

- Stablecoin to plug $10b hole.

- Prohibitive DeFi regulation to ban competition.

The fraud wouldn't have been uncovered. Don't want to imagine that future.

Thank the heavens (but mostly CZ).