Mesh network stress test running in the Mediterranean 🌊

Testing autonomous routing optimization across 10 nodes with adaptive duty-cycle balancing. The fleet maintains

GSM/WiFi-grade resilience while respecting regional duty-cycle constraints critical for long-range oceanic deployments.

Key focus: battery performance vs. radio duty-cycle trade-offs. Each node dynamically adjusts transmission power and hop-count routing based on real-time mesh topology.

Current run: 25 messages routed through up to 5-hop paths, with autonomous low-battery escalation protocols kicking in when needed.

The goal? Keep the mesh alive for weeks, not hours. Deep ocean operations demand extreme power efficiency every milliwatt counts when you're 50km from shore.

Real-time telemetry, multi-hop routing, and self-healing topology. This is the unglamorous engineering work that makes ocean cleanup actually scalable.

I know many of you want frequent updates and I appreciate the enthusiasm. But as you can see, this is a robotics project with extreme constraints. We can't push daily updates while maintaining quality and safety standards.

That said, a proper logbook will be maintained throughout deployment. Engineering takes time. We're building for reliability, not hype.

And thank you for all your messages. I genuinely enjoy exchanging with you all. Your support keeps the project moving forward.

$AVICI casually disrupting how banks work today by bringing mortgages on-chain.

up ~50% today > outperforming the majority of the market.

One of the few projects (would rather call it a business) out there that’s really building.

Top 100 project trading sub 100m.

@AviciMoney

My top picks: 🚀

$CLANKER: AI launcher, $34M fees, Farcaster-owned – https://t.co/mOB1UvyeTI on steroids 🔥

$AVICI: Solana neobank, Visa cards, $1.2M spend, no team tokens – $11M steal 💳

$PREDI: AI agent predix on Base, live odds trading, $100K+ vol boom – +35% beast 📈

Avici on dip after running 300% in a day

I think anything under 100m for AVICI is cheap

It's the first real neobank in crypto, your app is your bank, you control everything

You can spend unlimited money from the Avici card, no limits

They will integrate SEPA transfer coming weeks

Compared to competitors on the market, XPL at 3.5B mcap

NEXO 1.3B

AVICI 23m mcap and it had the best product

CT is sleeping on this one

Much higher

“The padre token will no longer have utility on the platform”

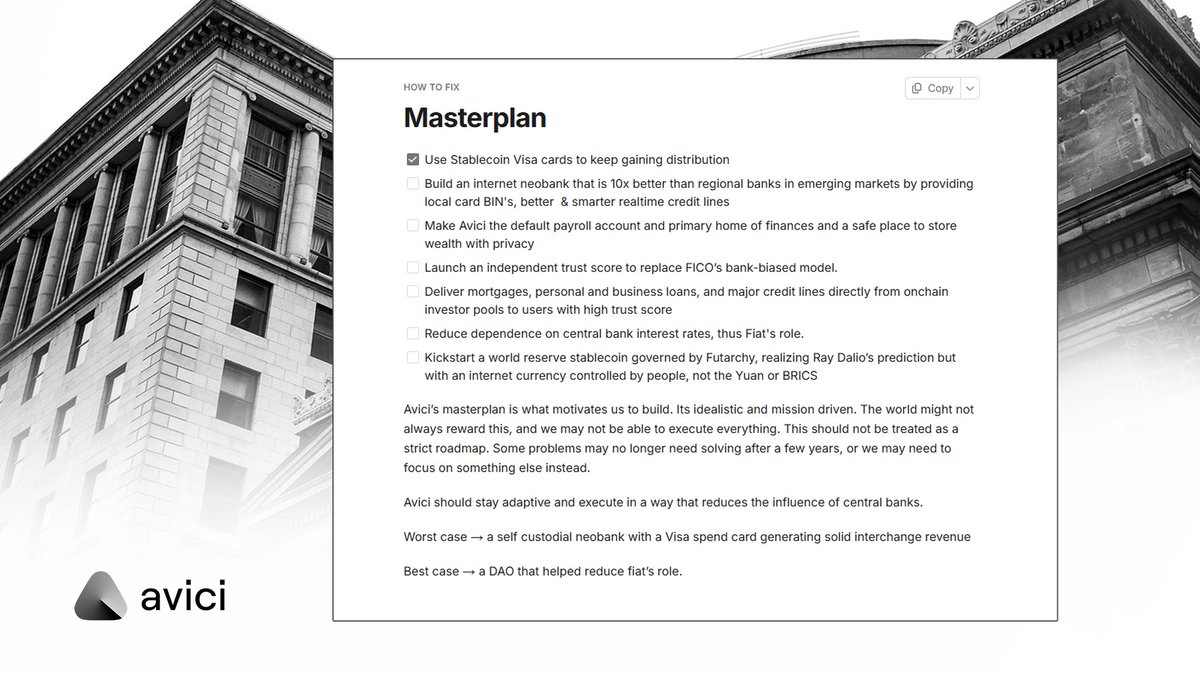

first best decision we made at Avici, build an internet bank as a DAO.

second, launch it as an ownership coin.

tokens are very broken, we just showed how it should be done.

study ownership coins. Study metadao.

Yes, there is a coin on Solana too.

- ownership coin powered by @MetaDAOProject

$AVICI (4h)

$11m FDV.

Competitors worth billions.

Founder’s a Chad, raised big, took only what he needed. Never even wanted to launch a coin… got convinced. Complete opposite of Plasma.

I’m invested in the coin, but what really interests me is the app’s potential.

Tip: Follow @game_for_one for consistent alpha and solid market insights.

https://t.co/77qLzrMIac

$AVICI | @AviciMoney

Built a position over the last few days, feels like a free money < $10M fdv.

Actually, what excites me most isn’t the token, it’s the product. Long time I don't feel this, and I'd consider this as a good signal, there is PMF.

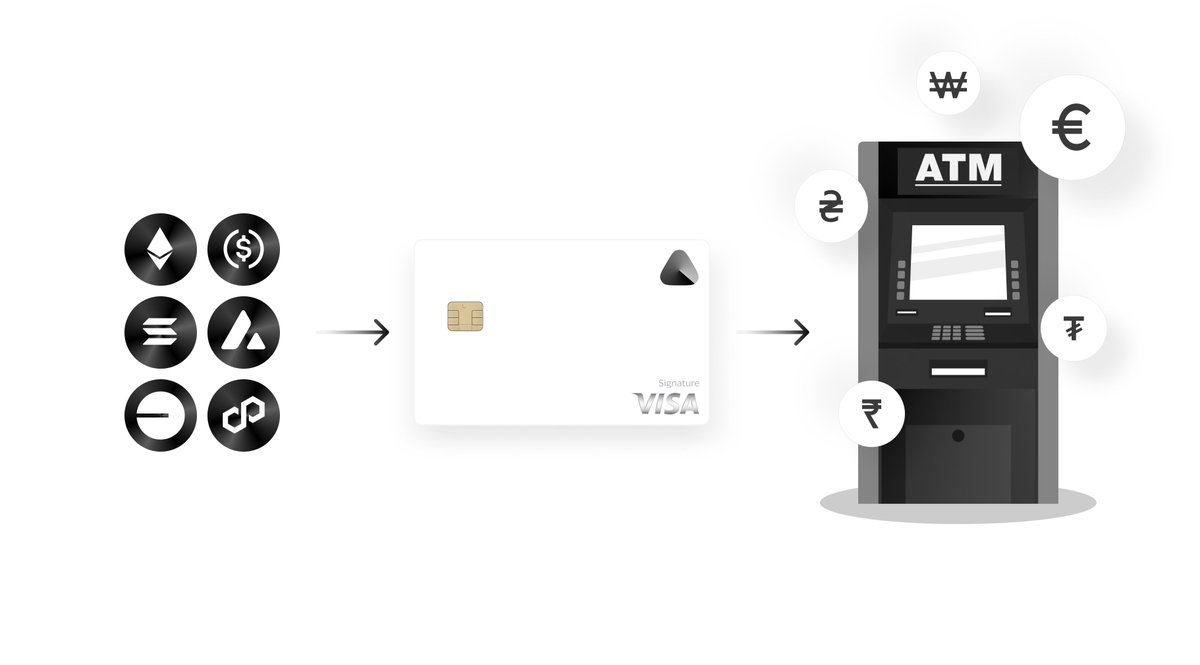

Avici is a self-custodial neobank with a Visa spend card (Apple Pay compatible).

You can deposit fiat (USD/EUR) via IBAN, it converts into USDC, and you spend directly from your wallet. No custody, no middlemen, no bs..

If you’ve ever tried to move between fiat and crypto using a traditional bank, you know the pain.

On top, every other crypto neobank is custodial, while on Avici you hold your funds.

Over the next few months, the team will focus on growing their product offering and revenue streams. I'm especially bullish on the unsecured lending feature they plan to add and business accounts, that's gonna be massive.

Product is good, but tokenomics too

- 12.9M supply,

- FDV = mcap = $9.7M @ $0.8,

- Launched at $0.35 (best entries are still only 2.3x up).

- 77.5% went to ICO, 22.5% to liquidity.

They launched with MetaDAO as a ICM, raised $3.5M out of $34M commitments, and stayed fully community-driven, no VCs.

Governance runs through futarchy, where decisions aren’t voted on but bet on, which means participants are incentivized to bet on outcomes that actually benefit the protocol.

The team has a $100K/month spending cap, making sure they don't waste money on stupid shit and any increase must go through the DAO.

Finally, revenues flow back to the DAO treasury = transparent accounting

No hidden deals, no inflated marketing budgets, no nonsense...

That’s probably why you don’t see the usual Solana KOLs pushing this, there are no hidden deals. Just people who understand what they’re building and why it matters.

It says a lot about a team if they commit to launch this way, you know they are serious and here to build. They were also publicly supported by one of their main competitors, Kast founder.

Finally, the product speaks for itself..

Their beta version has an app in the AppStore, $800k+ on-ramped, 5k+ signups, 4k+ active cards, ~70% retention rate, +35% MoM spending growth.

It's funny seeing Plasma offering "neobanking" with barely a product and massive emissions, while Avici is doing it with a working app, and no emissions.

Here’s what you need to know about $AVICI:

• It’s a non-custodial crypto bank.

• That means you hold your own keys. Not them.

Most “crypto banks” still act like banks.

They can freeze funds without reason. Keep YOUR money hostage. Then make you create support tickets to unfreeze your card or transfer.

But here's the kicker:

$AVICI lets you keep custody, but you still get:

✅ Real IBAN accounts

✅ Visa cards (no top-up fees, no limits)

✅ Direct salary deposits converted to USDC

Already live and generating revenue.

It’s banking rebuilt. But without the bank.

Do with this info what you will. 🤝

🚀 $AVICI is ready to soar!** 💥

Imagine a DeFi neobank: spend stablecoins anywhere with a Visa card, no banks, no KYC hassle. Self-custody wallet, 0-fee swaps, and a token with REAL DAO ownership. 0 team tokens—100% fair! Launched at $0.35, already up ~150%... next stop $5?

$AVICI: @AviciMoney

> Non-custodial you hold your own keys, not the project. NOBODY can touch or freeze your funds (unlike many other competitors)

> You’ll have an IBAN account, simply put, users can receive (and send) salaries in fiat (same for businesses with their income) directly, which will be auto-converted to USDC.

> It offers a VISA Card with no top-up fees, no FX markups, no transaction fees, no payment limits, if you want to spend millions in a day, you can.

> Avici BIZ will be launching soon —> business accounts for startups, DAOs, institutions etc.

> DAO-owned: 0 VC or team allocation, a treasury spending cap (unless the DAO decides otherwise), and 100% circulating supply.

> Revenue model is sustainable: Visa interchange fees + FX spread + Premium tiers, and future lending yield (already live & generating revenue).

> 3.5M was raised out of 34.2m committed, many people got refunded, shows that the team is here to last.

> App is already live on iOS & Android, already showing good functionality even in beta.

> Even the CEO of @KASTcard, a competitor is interested in buying $Avici & helping the Avici team.

Just a fraction of what Avici is building is summed up here. With all the functions they’re planning to add, there simply won’t be much need for individuals to use traditional banks, something the crypto space has waited for, for a long time.

What Avici achieved in their beta so far:

- Total spend with Visa card: $1M+,

- Avg growth of spends: 35% average MoM

- Retention for active users*: 70% MoM (people are satisfied with their product)

- Total onramp volume (USD,EUR): $800k+

- Cards created: 5k+

- Total signups: 9K+

Avici is already generating revenue in its beta. 90% (if not more) of projects never reach this stage, and for $AVICI, it seems like the standard rather than the goal.

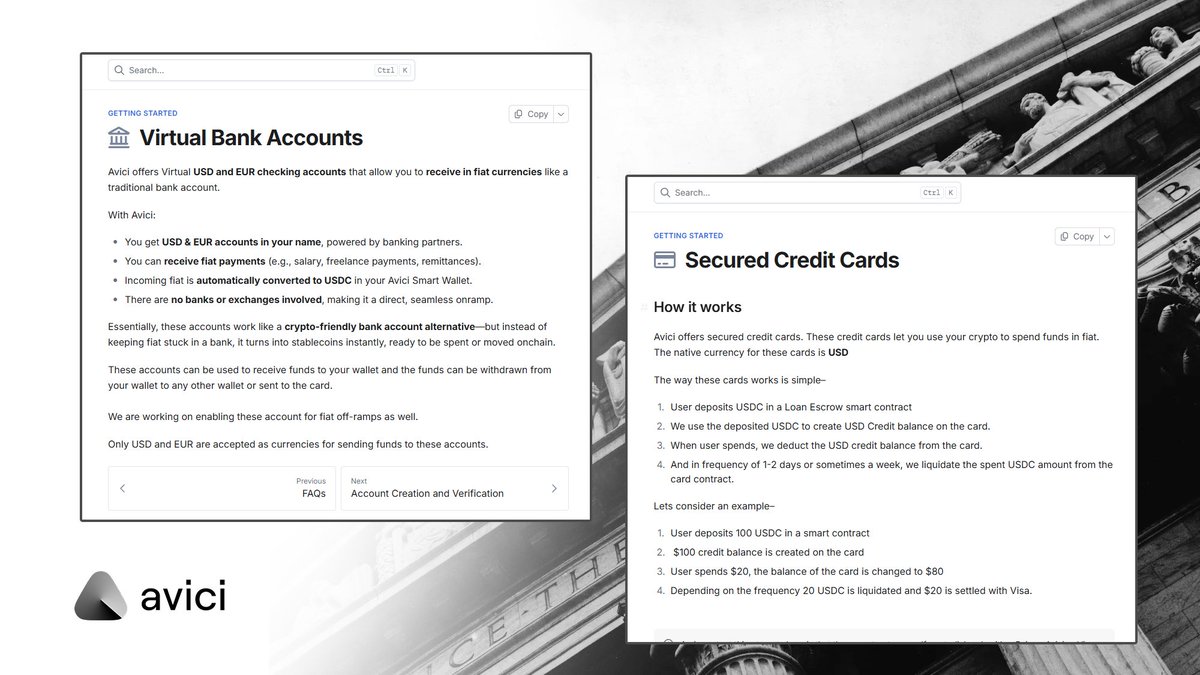

Avici consists of two main products:

1. The credit cards, which let you spend your crypto directly and this card can even be added to Apple Pay, Google Pay, etc.

2. The virtual banks, bank accounts with an IBAN, that allow you to on-ramp fiat to crypto via simple transactions, such as receiving your salary. The fiat is auto-converted to USDC and sent to your Avici wallet.

You can basically see it as a crypto bank that gives you a Visa card (physical + virtual), lets you receive and send money like a normal bank account (thanks to your own IBAN), and lets you hold, swap, and spend crypto directly from your wallet. And because you’ve got a Visa card, you can spend crypto worldwide.

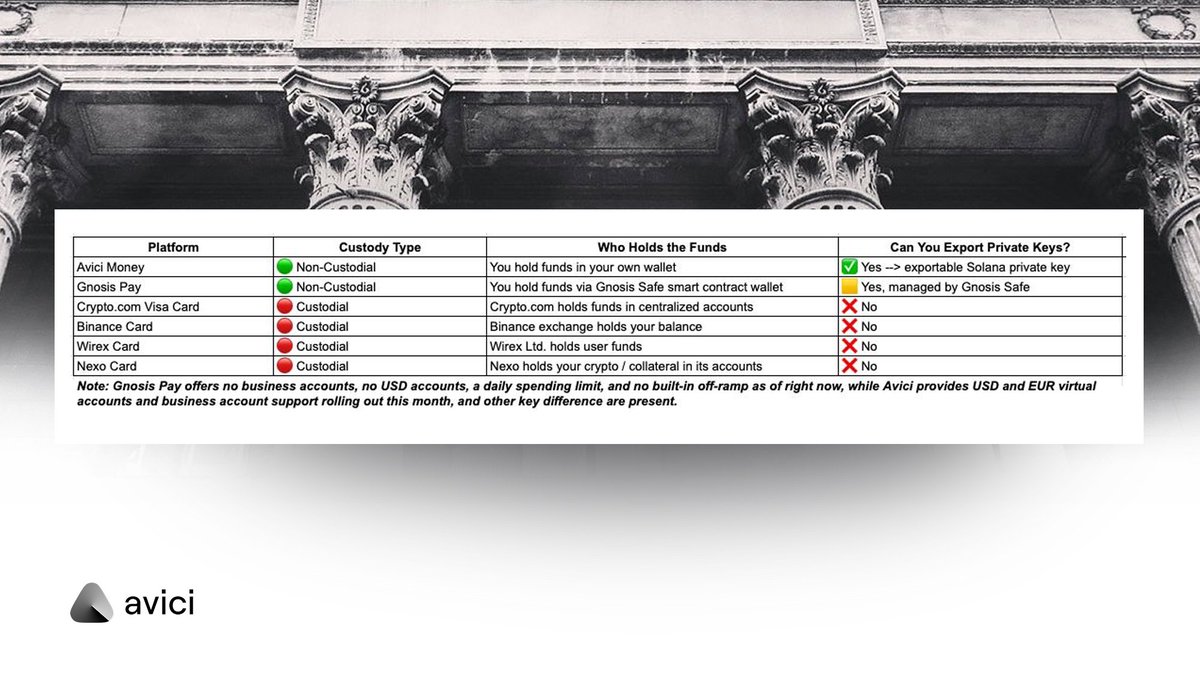

One of the biggest pros here is the safety aspect. Most cards e.g., https://t.co/syA5WAcNul, Wirex, Binance, etc. are custodial, meaning they hold your money. If the company goes bankrupt or freezes your account (like FTX), you simply lose access to your funds, and they could very well be gone. Avici is non-custodial, meaning you own your wallet and private keys. They (and nobody else) can freeze your money or touch your funds in any way.

Fee-wise, it’s also beating competitors + there are no payment limits, you can spend millions if you want.

I’ve seen some questions regarding the card purchase fees, which is between $10 and $30 (and $20 annually for the signature tier) for the virtual cards. However I think every user will prefer a fixed fee in dollars that doesn't increase when you spend more over a high recurring percentage fee that ''eats'' into every transaction and basically scales with your spending because it's a percentage, not a fixed amount of $. If you need a discount or setup help, DM @AviciHelp. They got support on X and TG.

Avici can basically be seen as the crypto bank everyone hoped for > one that’s able to deliver on the promises the crypto space has made to us: real usage of crypto, worldwide, as a means of payment, without any centralized institutions able to touch your funds.

I bought from here. Jup has the best liquidity. https://t.co/9sgxeWFO9A