I'm starting a new journey on X 🚀

I'll be exploring fascinating topics and breaking them down into:

→ What they are

→ Why they matter

→ When to apply them

→ How they work

Join me as I decode the interesting, one post at a time.

Based in India 🇮🇳 | Let's learn together!

RBI just handed the rupee a lifeline most people haven't fully digested yet 💪

FCNR(B) to private banks = $50-60B potential inflow. That's not just a deposit story, it's a CAD buffer, a rupee stabilizer, and a quiet signal that RBI is managing external account stress proactively.

Strong rupee = lower imported inflation = more room for rate cuts 📉

Near-term rupee bulls have real fundamental backing now, not just sentiment.

Watch: IT exporters like TCS, Infosys face mild headwinds on repatriation margins. But import-heavy plays — oil OMCs like HPCL, BPCL — get a quiet tailwind if rupee firms up.

The multiplier here goes beyond forex. Cheaper money, easier CD ratios, softer rates ⏩ it's a chain reaction.

RBI played this one well. 🎯

#RupeeRally #RBIPolicy

More on @IQDecoded | Not SEBI Registered, DYOR

FCNR(B) opening to private banks is a bigger deal than markets are pricing in 🔥

$50–60B inflow = ₹5L Cr added to deposit base. That's a 2% jump in a single policy move, easing the CD ratio and taking rate-cut pressure off RBI's shoulders.

Watchlist👀 : HDFC Bank, Axis Bank, ICICI Bank (direct FCNR beneficiaries sincemore forex deposit mobilisation capacity) 📈 | Kotak Mahindra Bank (lean liability franchise — disproportionate benefit if inflows are strong)

Rate-sensitives like home finance & NBFCs breathe easier too. Lower domestic rates = cheaper cost of funds for Bajaj Finance, LIC Housing. ⚡

This is quiet monetary easing without touching the repo rate. Smart policy.

#BankingIndia #RBI

More on @IQDecoded | Not SEBI Registered, DYOR

Rupee sitting at ₹95.4 to a dollar is nearly a 6% slide in 2026 alone, and the market has felt every bit of it 📉

If these RBI moves ⏩ zero tax on G-Sec gains for foreigners, FCNR(B) sweeteners pulling NRI dollars home — actually pull USD/INR back towards 90, the macro picture shifts completely. Lower import bills, cooler inflation, and suddenly RBI has real room to cut rates further. That's a triple tailwind hitting equities at the same time 🔥

Rupee strength isn't just sentiment, it's the foundation everything else is built on. Watching this very closely too. 👀

More on @IQDecoded

*Not SEBI Registered, DYOR*

#IndianMarkets #Rupee

India's window is NOW and it's closing faster than most realize.

🇮🇳 FIIs pulled out ₹1.7L Cr+ from Indian equities in just 6 months (Oct '24–Mar '25). Meanwhile, AI-driven US tech correction is forcing global capital to hunt for the next high-growth story.

India could BE that story but only if:

📌 STT rationalization happens

📌 LTCG parity with real estate is addressed

📌 Derivatives reform builds institutional depth, not just retail FOMO

Stocks for watching the reform narrative closely:

🔹 BSE — exchange volumes directly tied to market structure changes

🔹 CDSL — depository gains as FII participation deepens

🔹 Angel One/Groww — broker ecosystem re-rates on STT cuts

India has demographics. India has growth. What it needs is a signal that the rules won't shift mid-game.

The AI crash gave us a window. Reform decides whether FIIs walk through it or keep walking past us. 🚪📈

More on @IQDecoded

#FIIFlows #MarketReforms

*Not SEBI Registered, DYOR*

📊 LTCM lost $4.6B in weeks. Retail F&O traders lost ₹1.81L Cr in FY24 alone (SEBI data). Leverage amplifies both sides but the downside hits faster than the upside ever built. 📉

When TQQQ inflows spike and put/call ratios collapse, that's not confidence 👇

That's complacency 👀

Leveraged ETF euphoria is historically one of the loudest risk bells 🔔

Stay curious about the downside. It keeps you alive for the next bull run. 📉➡️📈

More on @IQDecoded

#BehaviouralFinance #RiskManagement

This is a genuinely sharp observation and the data actually makes it more damning for IT services 🧵

Anthropic alone went from $87M run rate in Jan 2024 to $30B by April 2026. 300,000+ enterprise customers. 80% of revenue from businesses. No TCS. No Infosys. No Accenture holding their hand.

That's the uncomfortable truth hiding in plain sight.

Enterprises figured out API calls, Bedrock, Azure AI Foundry — largely on their own, with internal dev teams. The "transformation bridge" IT companies keep selling ⏩ Enterprises apparently didn't need it to write the first $50B+ cheque.

The IT services thesis rests on complexity at scale — governance, integration, legacy modernisation. That may still come. But the timeline is clearly not what Wipro's earnings calls implied. And worse — the adoption curve is inverting. Enterprises got comfortable *before* the handholding arrived.

More on @IQDecoded

#AIDisruption #IndianIT

*Not SEBI Registered, DYOR*

Add Iran striking US bases in Kuwait → Brent could spike → India's CAD widens → INR pressure returns.

Stocks to watch:

- 🔴 HPCL, BPCL, IOC — crude spike = marketing margin squeeze

- 🔴 IndiGo (INDIGO) — fuel costs re-escalate

- 🟡 Reliance (RIL) — oil-to-chemicals offsets partially

- 🟡 SBI, HDFC Bank — fiscal slippage = higher govt borrowing = yield pressure on bond portfolios

- 🟢 ONGC, Oil India — upstream gains on higher crude

Fiscal deficit creeping toward 4.7% in FY27 means less room for capex stimulus — the one lever markets were counting on 📊

More on @IQDecoded

#Nifty50 #IndianMarkets

*Not SEBI Registered, DYOR*

Here is the list of names on my radar:

🏆 POWERGRID — Transmits 50%+ of India's electricity via 1.75 lakh km network. Boring? Yes. Compounding machine? Absolutely.

⚡ Adani Energy Solutions — India's largest private T&D player with 20,000+ km of lines. High growth, high conviction.

🌞 Tata Power — Solar, EVs, storage — fully integrated play on India's energy transition.

💡 Torrent Power — Best-managed DISCOM in India with lowest AT&C losses. Efficiency = margins.

India crossed 505 GW installed capacity in Oct 2025 — world's 3rd largest. The grid has to keep pace. That's the T&D story.

#PowerSector #IndianMarkets

*Not SEBI Registered, DYOR*

The Nifty of 2030 won't look like the Nifty of today and that gap is where the real alpha hides. Banking + O&G + IT = ~55% of index weight right now. All mature, low-double-digit growth businesses.

🚀 Stocks that could earn index weight: 👀👇

⚡ Zomato — Profitability inflection + quick commerce scale. Revenue CAGR 60%+ last 2 years. Index inclusion already happened, weight will grow.

⚡ Dixon Technologies — PLI beneficiary, electronics manufacturing at scale. Revenues doubling every 2 years. Still under-owned institutionally.

⚡ Kaynes Technology — Aerospace + EV electronics. Niche but high-margin. Early-stage compounder.

⚡ Waaree Energies — Solar manufacturing at scale, export orders building. Renewable energy barely represented in current index.

⚡ Mankind Pharma — Consumer healthcare + domestic formulations. Consistent grower, index weight will rise with earnings.

⚡ Bharat Electronics (BEL) — Defence indigenisation is a decade-long theme. Order book at record ₹75k+ cr, revenue visibility is exceptional. Still under-represented vs earnings trajectory.

⚡ Polycab India — Wires, cables, FMEG. Infra + real estate upcycle plays directly into their order pipeline. Consistent 20%+ earnings growth, index weight hasn't caught up.

⚡ Cholamandalam Finance — NBFC with rural + vehicle financing dominance. ROE ~20%+, growing faster than most large private banks yet priced cheaper.

⚡ Persistent Systems — Mid-cap IT but AI-native revenue mix unlike TCS/Infy. Revenue CAGR ~35% last 3 years. Will graduate to large-cap index as market cap compounds.

⚡ JSW Energy — Renewable capacity addition at aggressive pace. Clean energy transition needs a large-cap anchor stock — JSW Energy is best positioned among pure plays.

🚀 All of these have earnings growth structurally above index average + underpenetrated institutional ownership. That's the combination that drives index rebalancing decisions. 🔥

More on @IQDecoded

Not SEBI Registered, DYOR

#Nifty50 #IndianMarkets

Rural demand held up even in the 2023 patchy monsoon ⚡

Stocks worth watching at current valuations 👀 👇

🚗 M&M — Rural + UV dominance, exports accelerating. PE ~20x vs 5yr avg of 18x. Barely stretched for the growth on offer.

🚗 Bajaj Auto — Export engine firing hard. 3-wheeler EV pivot underway. Trading at ~22x vs peers at 28x+. Undervalued on global franchise strength.

🚗 Maruti — CNG + entry-level demand structurally resilient to monsoon cycles. ~25x PE, reasonable for market share dominance.

🚗 Sona BLW — Auto components play, export-heavy, EV-agnostic revenue mix. Correction has made valuations attractive vs growth trajectory.

🚗 Endurance Technologies — Underfollowed. Strong 2W component exposure, clean balance sheet, ~20x PE.

Monsoon risk is real but already in the price. Sales data isn't lying. 👀

More on @IQDecoded

Not SEBI Registered, DYOR

#AutoSector #IndianMarkets

💯

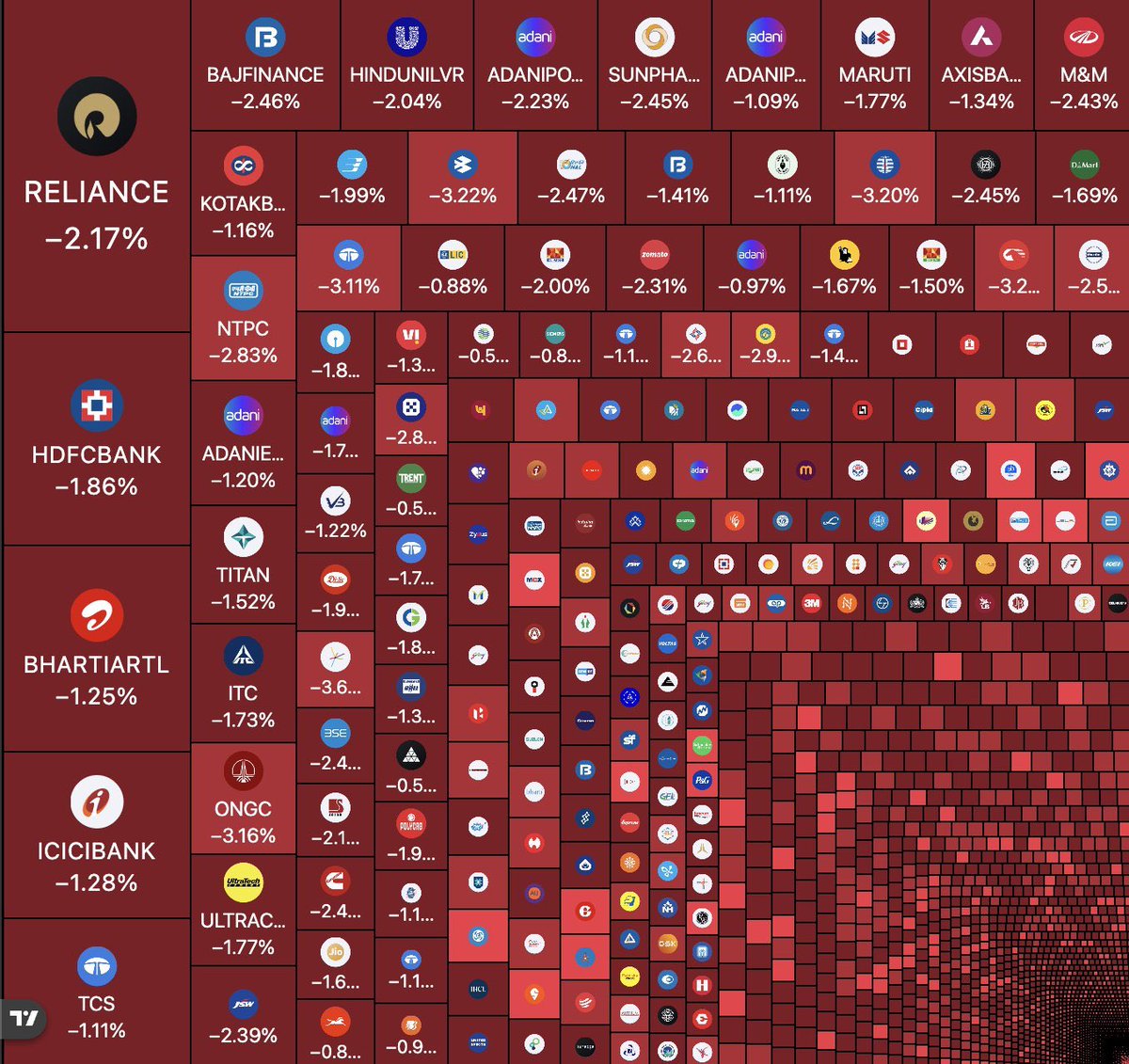

🔹 The velocity has changed completely. Faster global rebalancing, US rate differentials, and China re-rating pulled the trigger simultaneously. ⚡

🔹 But here's what the panic misses ⏩ DII absorption has never been stronger. SIP inflows at ₹26k+ cr/month means domestic money is catching every knife FIIs throw.

🔹 Stocks feeling the FII heat most: HDFC Bank, Reliance, Infosys ⏩ the index heavyweights where FII ownership is highest and selling pressure concentrates first.

🔹 ICICI Bank relatively more resilient given stronger domestic institutional support. ⬆️

⚡ The real risk isn't the selling, it's if rupee depreciation + FII outflows create a feedback loop that spooks retail SIP continuity.

That's the number to watch. Not the FII figure itself. 👀

More on @IQDecoded

Not SEBI Registered, DYOR

#FIIOutflows #IndianMarkets

🚀 When the market bleeds red, some companies are quietly printing 100%+ PROFIT GROWTH. 🚀

⚡ 15 STOCKS that crushed it in FY26 — and WHY it matters more than you think 🧵👇

These aren't random screener picks. This is full-year FY26 results — and the themes behind the numbers tell a bigger story 📊

The list:

🔥 Cupid +254% | 🏥 Contraceptive exports boom — global health procurement surge

🔥 NACL +264% | 🌾 Agrochemicals revival, better monsoon-led demand

🔥 Diamond Power +192% | ⚡ Power infra capex cycle playing out perfectly

🔥 HBL Engg +184% | 🔋 Defence electronics + EV battery systems — classic dual-theme play

🔥 Quality Power +170% | ⚡ T&D transformation, green energy tailwinds

🔥 Senco Gold +154% | 💍 Jewellery consumption boom + organized retail expansion

🔥 MCX +146% | 📈 Commodity volumes surging — crude & metals volatility = MCX's goldmine

🔥 Puravankara +137% | 🏠 Real estate supercycle in South India, strong pre-sales

🔥 Lloyd Metal +131% | 🏗️ Ferro alloys demand from steel + EV battery material

🔥 Hitachi Energy +107% | ⚡ Power grid modernisation — order book visibility is strong

🔥 GE Vernova +102% | 🌬️ Wind + grid — India's energy transition is real money now

🔥 Navin Fluorine +102% | 🧪 Specialty chemicals recovery — CDMO pipeline kicking in

🔥 Pondy Oxide +101% | ♻️ Lead recycling economics turned favorable

🚀 HBL Engineering is a standout — full-year FY26 net profit rose ~194% with sales up 68%, driven by explosive growth in defence electronics and battery systems.

🔥 One common theme? Capex India — power, defence, real estate, and materials are where the real earnings were made in FY26.

High profit growth ≠ automatic buy. Valuations, sustainability of margins, and one-time items matter. Always dig deeper 🔍

More on @IQDecoded

Not SEBI Registered, DYOR

#Q4Results #IndianStocks

🚨 MSCI Rebalancing just triggered ₹6,800 Cr of forced selling in Indian markets today. Sensex crashed 1,092 pts. Here's what happened and which stocks got hit hardest 🧵👇

🔹 MSCI is a global index tracked by billions in passive funds worldwide. Every 6 months, it rebalances - adding & removing stocks. Funds that track MSCI *must* buy/sell accordingly. No discretion. Pure mechanical flow.

🔹 Today was the effective date.

🔹 4 stocks got booted from the MSCI Standard Index :

📌 RVNL (₹1,290 Cr outflow)

📌 Kalyan Jewellers (₹1,300 Cr)

📌 Jubilant Food Works (₹1,540 Cr)

📌 Hyundai India (₹2,690 Cr)

triggering ₹6,800+ Cr in concentrated passive selling in a single session. 📉

⚡ RVNL's sharp correction from its 52-week high dropped its free-float-adjusted market cap below the threshold.

⚡ Kalyan Jewellers faces similar pressure — the exit signals no fundamental change, just mechanical selling.

On the flip side,

📌 Adani Power and BPCL are among stocks expected to see inflows from weight increases. ✅

🔹 But MSCI wasn't the only villain today — crude above $104, stalled Iran peace talks, monthly F&O expiry, and FII outflows from financials all hit simultaneously. Six headwinds, one session. 🛢️

⚡ Bottom line: MSCI days are *known* in advance. The smart money positions before. Retail gets caught in the noise.

More on @IQDecoded

Not SEBI Registered, DYOR

#NiftyFalls #MSCIRebalancing

An Nvidia exec put it bluntly: "The cost of compute is far beyond the costs of the employees."

Uber's CTO burned through the *entire* 2026 AI coding budget in just 4 months. 🔥

Agentic AI uses far more tokens per task than standard models and Goldman Sachs projects a 24x surge in token consumption by 2030.

#AIBubble #TechMarkets

1️⃣ PFC (~6.7x PE) — Loan book growing 15%+ YoY. Power infra financing is a decade-long tailwind. Market underprices the growth runway.

2️⃣ *lREC Ltd (~6.5x PE) — Mirror image of PFC. Renewable energy lending is just getting started. Dividend yield kicker too.

3️⃣ Coal India (~7x PE) — ₹40,000 Cr+ cash on books. Earnings yield ~13%. The market treats it like a dying business. Reality? India's power demand says otherwise.

4️⃣ ONGC (~6x PE) — Oil major with massive upstream assets. Every crude upcycle re-rates this. Patient money play.

5️⃣ NMDC (~7x PE) — Near-monopoly on domestic iron ore. Steel demand = NMDC demand. Simple thesis, low valuation.

6️⃣ Bank of Baroda (~5x PE) — NPA cycle largely behind it. ROE recovering. Still priced like it's 2018. Classic mean-reversion candidate.

7️⃣ Canara Bank (~5x PE) — Same PSU banking story. CASA improving, credit costs declining. The re-rating is slow but real.

8️⃣ HPCL (~8x PE) — Refining margins volatile, yes. But ₹80,000 Cr capex plan into petrochemicals changes the earnings mix entirely by FY28.

9️⃣ Vedanta (~7x PE) — Zinc, aluminium, oil — diversified commodity play. Deleveraging progress + demerger optionality = potential re-rating trigger.

🔟 Sail (~8x PE) — Steel demand tied to infra capex. ₹15 lakh Cr govt capex pipeline directly feeds SAIL's order flow. Cyclical but cheap.

⚠️ Most are PSUs or cyclicals — low PE doesn't always mean cheap. Watch for earnings trajectory, not just the ratio.

More on @IQDecoded

#IndianMarkets #ValueInvesting

*Not SEBI Registered, DYOR*

Market cap per employee tells the real story 🧵

Adani Power: ₹12 Cr per employee 💡

Infosys: ₹1.43 Lakh per employee 👨💻

That's an 84x gap — because power is a capital game, not a people game.

Meanwhile Infosys revenue/employee (~$50K) is actually world-class for a services firm.

Two completely different business models — same market cap, totally different levers.

#IndianMarkets #FinTwit

📌 CDSL: PE compressed from ~85x to ~35x. Still a monopoly business.

📌 IREDA: Overvalued euphoria + NPA concerns. Fundamentals intact, but priced for perfection earlier.

📌 IRFC: AAA-rated quasi-sovereign. ₹99 is closer to fair value than ₹229 ever was.

Valuation reality checks hurt but they also create entries. 👀

More on @IQDecoded

Not SEBI Registered, DYOR

#FinTwit #IndianMarkets