The President of the United States is literally telling you that you should either own assets or learn to be a permanent member of the underclass

Government is not coming to save you. No regulatory changes are coming to save you

Make your financial bets accordingly

It's officially Fed day.

Markets are heading into the most divided Fed meeting since 2008.

The majority of investors think that the Fed should cut interest rates by 50 basis points today.

But here's why history says you DON'T want a 50 bps rate cut.

(a thread)

1/5

What to Expect When You’re Expecting

The Fed will begin cutting rates later this month. What should we expect, and what will follow? And how we are positioned for it?

https://t.co/6E6UDg1wmF

The “next” crisis rarely looks like the previous one

Why?

Because governments will do everything they can to prevent repeating it

There is not going to be a 2008 sized wave of residential foreclosures in this country ever again

h/t @mortgagetruth

Milton Friedman in 1978:

"The Great Depression was not produced by a failure of business [but] a failure of GOVERNMENT... And today... Inflation is made in one place: Washington D.C."

In 1979, my friend, mentor, and Nobelist Milton Friedman on the role of government:

"The government is TOO BIG. It's TOO INTRUSIVE. It RESTRICTS what we can do. It's becoming our MASTER instead of our SERVANT. We've got to react against it and cut it down to size."

POWELL SPEECH SUMMARY ⚠️

1. The Federal Reserve held rates at 5.25-5.5%

2. The CPI print today has been confidence building for the Fed but they are yet to achieve the level of ‘greater confidence’ that they deem necessary to commence rate cuts. Inflation readings earlier in the year were higher than expected but more recent months have eased somewhat and shown ‘modest’ progress. The Fed wish to see more good inflation data going forward prior to commencing rate cuts.

3. As always, Powell emphasized the data dependence of the Fed saying that they need to let the data ‘light the way’. Powell refused to specify when cuts might come and stated the ‘totality of the data’ would be considered when deciding when to cut, rather than any one inflation print or economic variable.

4. If the Fed sees incoming data that gives them greater confidence inflation is moving sustainably to 2% target then they would commence their cutting cycle. Powell emphasized the Fed’s dual mandate of both stable prices and full employment, noting that an unexpected deterioration in the labor market would also give the Fed grounds to cut rates.

5. Powell noted that it is not the Fed’s plan to wait for things to break and try fix them. They are trying to balance their two mandate goals.

6. Median forecast for the Federal Funds Rate for the end of the year is 5.1%

7. The labor market is coming into better balance and is relatively tight but not overheated. Powell noted that unemployment remains low and we continue to see strong job growth; wage growth has eased but still running above a sustainable path that would be conducive with 2% target.

8. Powell commented on payrolled jobs still being strong but also noted there’s an argument they may be overstated. He commented on not being able to reconcile the differences seen between the establishment and household survey in the monthly BLS jobs report. He acknowledged that this is part of the uncertainty that the Federal Reserve have to deal with when making decisions.

When the monthly BLS jobs report is released the report has data from different surveys. One survey gives data used for things like the unemployment rate (Household Survey) and the other provides reports like Nonfarm payrolls (Establishment Survey). The most recent print saw a huge discrepancy between the two surveys - Household reporting weakness and Establishment continued strength. This sent mixed messages and called into question the veracity of the continued strong payroll numbers. This is not a new argument and there has been notable and unprecedented difference in the signals being sent by the two surveys of late.

9. Powell noted that labor supply has increased due to immigration and increased labor force participation but specified mainly due to immigration.

10. The Fed’s increased forecast of core PCE at the end of 2024 was discussed (2.8%). Powell explained this is a conservative forecast which they don’t have high confidence in.

11. Powell feels policy is restrictive and having the effects the Fed hope for. Time will tell if it is restrictive enough. He feels the Fed have made pretty good progress with current stance.

12. Powell commented that the long run neutral rate of interest (R*) is an important theoretical concept but states that this isn’t useful when trying to decide current policy decisions.

The neutral rate is the interest rate at which monetary policy is neither restrictive or accommodative. It is a hot topic of debate and fluctuates over time.

13. Powell states that the banking system seems to be in good shape and banks have made moves to bolster since the crisis starting in March last year.

14. GDP continues at a solid pace, consumer spending remains solid. Households not in as good a shape as they were a year ago but remain in good shape. This is something the Fed are keeping an eye on.

15. Discussed that shelter inflation is operating with long lags that could take years to be worked off. Fed sees this happening more slowly than they initially anticipated.

A 7% mortgage rate in 2024 is like a 15% rate in 1982

How👇

When accounting for U.S. home prices, home insurance, incomes, property taxes, and a 10% down payment, housing affordability in 2024 is similar to 1982 (when rates floated between 13%-17%)

via @johnburnsjbrec@JBREC

Jacksonville, FL

Slowed down quite a bit, pricing strategy is absolutely essential. Still a disconnect between Seller expectations and market pricing.

Well price homes in good areas still selling with multiple offers and above ask.

If it’s not priced well, it’ll sit and you’ll be chasing the market down, dangerous place to be at the moment!

1/4

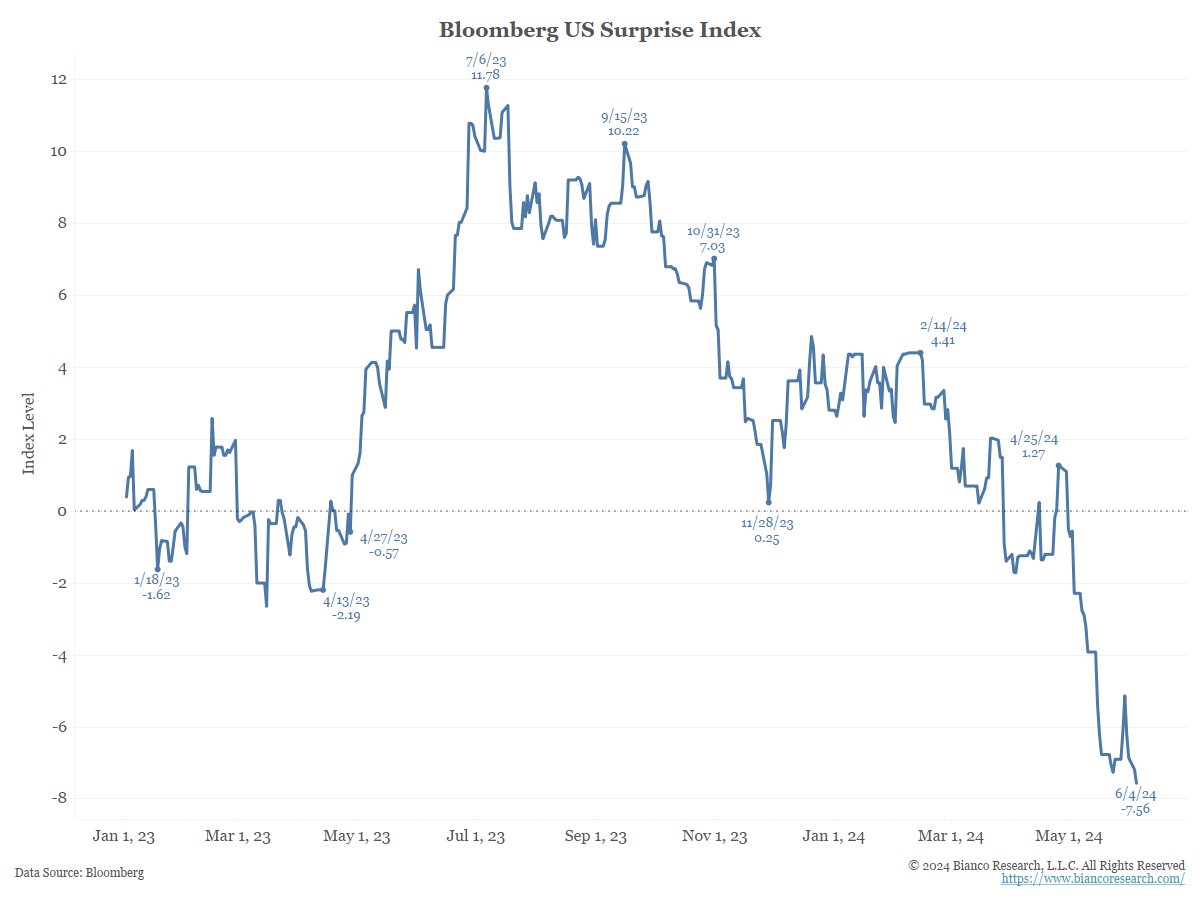

Lots of talk about an economic slowdown, but what exactly is slowing down?

tl:dr, surveys of opinions, not actual or "hard" data.

---

Start with the Bloomberg Surprise Index. It is an index of economic releases measured against the consensus forecast for each release.

How to read it?

A number above zero means the economic data is coming in above expectations, and a number below zero means worse than expectations. The trend matters as it shows whether things are improving or deteriorating (again relative to expectations).

What does it say?

The economy has turned sharply lower (steep downtrend) and, since the beginning of April, coming in much worse than forecasted (below zero).

Sound ominous. However ....

There "has been a change" in the TX RE market

Economy is affecting "wealthier people" and multi-million dollar homes

He verifies "occupancy"

For everybody in TX who was crying FOMO in early spring...

Things are not always what they seem

H/T: @GRomePow

CC: @DiMartinoBooth

Existing home sales are in a deep recession

We're back to 70s levels—despite a much bigger country

--

April 1978: 4.09 million U.S. existing home sales print

April 2024: 4.14 million U.S. existing home sales print

1978: 223 million U.S. population

2024: 341 million U.S. population

Lennar—a homebuilder ranked No. 119 on the Fortune 500—is presently promoting a FHA fixed rate of 4.25% in San Antonio

It's "available for the life of the loan"

3.5% down, a minimum credit score of 680

h/t @RickPalaciosJr on flagging this one

https://t.co/1TFJQySaYP

#TurkeyWatch🇹🇷: Turkey's money supply (M3) continues to SURGE at a RECKLESS ~64%/yr.

The result:

On this week's #HankeInflationDashboard, Turkey registers the WORLD'S 7th HIGHEST INFLATION RATE at 74%/yr by my measure.

Pres. Erdogan is asleep at the wheel.

U.S. housing market falls short: 18 million fewer people than projected by Census in 2008

@AzizSunderji finds the U.S. fertility rate is falling much faster than expected

https://t.co/XBj9hwwm9T