Primera noche del PS salvada con oficio, me atrincheré en el Auditori con el diluvio y remontada histórica tras el palo de la cancelación de Massive Attack:

Paus

Blood Orange

Lucrecia Dalt 🏆

Caroline

Panda Bear

Rustie

Fcukers

VVV [Trippin'you] 🏆

Six Sex

¥ØU$UK€ ¥UK1MAT$U

En los años noventa, la alta cocina se medía por la capacidad de quebrar un pequeño bizcocho y ver brotar un río espeso de chocolate. El coulant no era solo un postre; era el clímax dramático de la cena. Como cocinero, recuerdo la tensión en la línea de pase cuando salían aquellas joyas. Si te pasabas un minuto, entregabas un vulgar panqué; si te faltaba un suspiro, el volcán colapsaba en el plato.

Esta genialidad nació en 1981 en las cocinas de Laguiole, Francia. El legendario chef Michel Bras tardó dos años de obsesiva investigación para patentar su Biscuit Tiède de Chocolat. La magia original de Bras no radicaba en una masa cruda, sino en una técnica de física culinaria: congelaba una esfera de ganache de chocolate y café, la introducía en una masa de bizcocho y, al hornear, el exterior se cocía mientras el núcleo se derretía por completo. Era una obra de ingeniería gastronómica.

El éxito fue su condena. El postre se transformó en un mito global y, con el cambio de milenio, mutó en infinitos primos hermanos. En los países anglosajones lo llamaron lava cake; en Italia, tortino al cioccolato; en Sudamérica, volcán de chocolate. Pronto aparecieron versiones saladas con quesos potentes o trufa, demostrando la versatilidad de la técnica de Bras.

Sin embargo, la industria alimentaria olió la sangre y decidió democratizarlo hasta la asfixia. El coulant ultraprocesado invadió los congeladores de los supermercados y las cadenas de comida rápida. Hoy, con tristeza, veo cómo cientos de restaurantes con pretensiones estafan al comensal sirviendo un bloque industrial recalentado en el microondas, vendiéndolo con el descaro de la etiqueta "hecho en casa". La masificación mató el misticismo del volcán original.

Por fortuna, la resistencia vive en el calor del hogar. En mi cocina, el postre ha encontrado una nueva vida, libre de la soberbia culinaria y lleno de afecto. Esta es la versión que preparo junto a mi hija, bautizada con orgullo como El coulant de chocolate de Lía.

Para revivir la magia en casa, fundimos despacio al microondas o a baño María 250 gramos de chocolate negro al 70% de cacao junto con 200 gramos de mantequilla sin sal. Mientras el chocolate se rinde al calor, batimos 6 huevos medianos con 100 gramos de azúcar morena fina hasta que la mezcla blanquee y duplique su volumen. En ese punto de aire y ligereza, tamizamos 90 gramos de harina de repostería y 36 gramos de cacao en polvo, incorporándolos a los huevos con movimientos suaves y envolventes.

Llega el momento crítico: vertemos el chocolate fundido con la mantequilla. Hay que cuidar con recelo la temperatura; si está demasiado caliente, cuajará los huevos y arruinará la textura. Una vez lograda la masa homogénea, la trasladamos a una manga pastelera y la dejamos reposar cinco minutos en la nevera para que tome cuerpo.

Para el montaje, untamos moldes individuales con unos 15 gramos de mantequilla pomada combinada con un pellizco de sal fina; este contraste potenciará el amargor del cacao. Rellenamos los moldes solo hasta la mitad. En el corazón de cada uno, colocamos el secreto de Lía: una lágrima de chocolate con frambuesa que aportará una acidez brillante. Cubrimos con más masa desde la manga, cuidando de no llenar el molde hasta el borde.

El desenlace depende del tiempo. Si decidimos congelarlos para el futuro, el horno debe estar a 200°C y se cocinarán durante 12 minutos. Si van directos al fuego, a la misma temperatura bastarán solo 5 minutos. En ambos caminos, la regla de oro del cocinero es inquebrantable: se dejan reposar dos minutos exactos dentro del molde antes de desmoldar con cuidado. Al romper la corteza con la cuchara, el río de chocolate y frambuesa nos recuerda por qué este ícono, a pesar de la industria, jamás podrá morir del todo.

La foto es de su primera receta con 7 años.

one of my most anticipated albums of the year just dropped and it's sooo good. v much recommended for ppl into the weirdest corners of brazilian music, extreme glitching/electronic manipulation and post-rock that, thankfully, does not feel ai generated 👍

https://t.co/Jj7CtJYpff

Investment thesis: The moment has arrived for the oil services supercycle.

For the past decade, I’ve listened to permabulls predicting the start of the oil capex supercycle. I always laughed because the right conditions weren’t there. However, this is changing now. Despite what you might think, it’s not driven by the Middle East conflict, as it wasn’t affected by the Russian war. Let me explain:

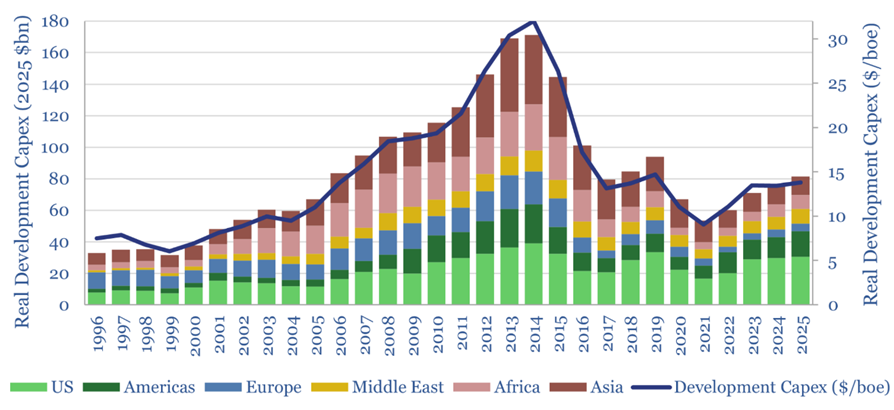

Oil service companies saw substantial growth before 2014, particularly between 2010 and 2014, as the global economy bounced back quickly following the financial crisis, with offshore oil supply attracting major focus. During this period, oil prices remained above $100, and market sentiment focused on oil scarcity. Consequently, O&M companies prioritized expanding and securing reserves, with little concern for costs or CAPEX. As a result, the oil services sector expanded quickly, and stocks traded at higher multiples, reflecting optimistic long-term prospects. However, this trend reversed sharply after 2014 when the US introduced fracking technology, unlocking unconventional reserves and establishing the US as a leading global energy supplier. This disruption killed the offshore sector, which was the marginal supplier, and triggered a wave of bankruptcies. Most offshore producers exited the market because their breakeven costs were too high to compete. In contrast, US shale could bring oil to market much faster and with less investment, unlike offshore drilling, which requires many years and significant capital expenditures before producing its first oil.

As shown in the graph below (first picture), capex declined sharply starting in 2014, and we are currently at just 50% of that year's oil investment level. Interestingly, this graph is often used by permabulls as an investment case, arguing that insufficient global investment will lead to prolonged periods of high oil prices. However, over the past decade, this prediction has repeatedly failed, leading to many failed claims of an upcoming oil supercycle. They overlooked the impact of the US shale revolution and the fact that US output now meets market needs with much lower investments, rendering this graph less relevant.

Returning to the story, the offshore sector somewhat adapted to the new oil environment, with lower prices driven by the US's infinite supply. Thanks to technological efficiencies and industry consolidation, the offshore space was revived in 2019. Oil demand was strong, and for the first time since 2014, prices exceeded $80, prompting new offshore investments to develop oil reserves.

However, this was short-lived as COVID emerged in early 2020, disrupting not only oil demand due to widespread closures but also supply, as Saudi Arabia initiated a price war against Russia, flooding the market with oil. Inventories soared, and demand weakened, requiring significant time for the world to adjust. Who was willing to invest in developing reserves in this environment? Perhaps even more critical for the sector was the irrational behavior during 2020/2021. Suddenly, oil faced harsh criticism while the world shifted to green energy. Oil majors were pressured to redirect investments toward renewables, further reducing investment in the oil sector, including oil services. By then, the consensus was that oil demand would peak by 2030, killing any hope for investments in the offshore space, which requires large, long-term commitments. Additionally, investors grew frustrated with oil companies' stock performance and demanded that firms prioritize shareholder payouts over reserve development. Consequently, oil services endured another wave of downturns, with increased scrapping, bankruptcies, and layoffs.

I also want to highlight that during that period, we achieved significant profits in the oil sector, primarily by investing in oil producers. In 2020, core investments like Devon Energy and IPC yielded extraordinary returns, as did recent ones like Kosmos. Our idea was simple; we differ from the consensus on the oil demand outlook. I believe oil demand was healthy and growing, driven by emerging markets, yet the world was well supplied by US shale. Therefore, investing in oil producers was a smart move, as these investments were carefully sanctioned, with a focus on cost control and short-term payback periods. Oil suppliers require investment enthusiasm, which was not the case in our scenario.

As shown (second and third pic), oil demand grew steadily over the years. It has never been a demand issue, except for short-term impacts, making the narrative about peak oil quite unfair.

However, the US supplied nearly all new oil demand, rendering OPEC insignificant. Notably, OPEC's production has remained stagnant for the past 30 years. (pic 4 and 5 in the following post)

Finally, the environment is undergoing significant changes:

1. The consensus on peak oil demand has shifted from the late 2020s to the 2040s. Irrational behavior in green investments has notably slowed, and major companies have redirected their focus back to oil.

2. US oil production seems to have peaked. Last year, the US shale industry warned that the era of abundant free oil supply was behind us as first-tier reserves were exhausted. US shale oil output was known for its rapid responses, spiking when oil prices rose. However, despite oil prices surpassing $100 this time, there hasn't been a corresponding increase in production. Key indicators such as Frac Spread Counts and other metrics point to the conclusion that US shale supply growth has ended.

3. The Middle East situation has highlighted the importance of energy security.

4. Investor sentiment has shifted – investors now place a higher value on oil companies with longer production profiles.

In this environment, with demand continuously increasing and the US supply struggling to meet this new demand, I see companies once again investing in the offshore sector, since it’s the only way to balance global supply. Moreover, the offshore industry has seen a significant reduction in supply due to considerable challenges, so even a small increase could make a meaningful difference.

Based on that, I made Constellation Oil Services ($COSH) my largest equity position. I'll explain in a future post why I chose COSH. As a conservative investor, likely influenced by my management of a fixed-income fund, I believe that if my outlook is correct, COSH may not be the top gainer, even though it will be a home run. However, it offers better safeguards if my view proves less accurate. Its strong backlog, healthy balance sheet, and dividend focus give us a substantial margin of safety.

I see many catalysts, including the uplisting, dividend increase, and debt refinancing in November. That last will significantly lower interest costs, improve covenant flexibility, and enable higher dividends.

Do your own diligence

Euforia total. Goldman avisa: . La asimetría (skew) media put-call a un mes de las acciones individuales del S&P está en el nivel más bajo de nuestra serie de datos (mirando 24 años atrás). Es decir en 24 años nunca se había visto una euforia como la actual.

This is an excellent interview btw

Nicolai (Norwegian Sovereign Wealth Fund CEO) asks the IBM CEO if AI a bubble

Listen very very carefully to his answer

Este librito es un regalo para todos los fans de Coil. Las tiernas memorias de Matthew Levi Stevens de su amistad con John Balance, con numerosas visitas a su casa de Londres, antes de la auténtica explosión de la banda. (...)

Una química israelí que vendió fósforo blanco militar deja en Catalunya 45 millones de toneladas de sal contaminante

La montaña de sal de la empresa ICL Ibérica ha contaminado el río Llobregat y sus alrededores

https://t.co/ZsgIefvViX

Buah. Andrea Fuentes y el equipo español 🇪🇸 de natación artística se han propuesto hacer historia DE VERDAD.

Así ha sido el estreno internacional de la rutina acrobática de este año al ritmo de ‘Berghain’ de Rosalía.

Van a conquistar el mundo.