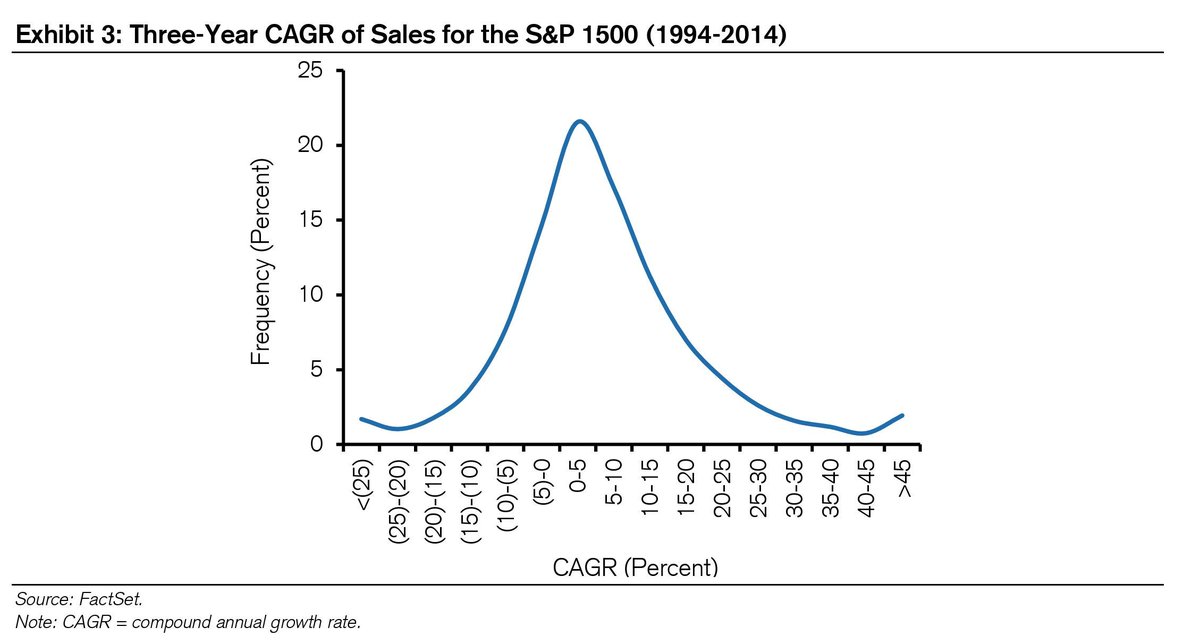

Remember that a 10% CAGR is very good. Chasing 30% CAGRs is tempting, but something that has rarely been done. If you're pricing in a 30% CAGR across your entire portfolio, there are some risks you're not considering.

value investors should understand that $nvda was cheaper at 250x ltm earnings than it is today at a fraction of that valuation.

you have to look ahead. consider that if youre looking at software just because it's cheaper on a multiple basis.

for PAs, i’ve always thought it would be a good idea to take your 10 favorite managers and make each of their largest positions a 10% position.

have to imagine this outperforms the s&p over time.

crazy to me that some people still aren’t interested in power stocks.

“the limiting factor for ai deployment is fundamentally electrical power. we’re seeing the rate of ai chip production increase exponentially, but the rate of electricity being brought online is negligible. it’s clear that very soon, maybe even later this year, we’ll be producing more chips than we can turn on.”

— elon musk in january 2026

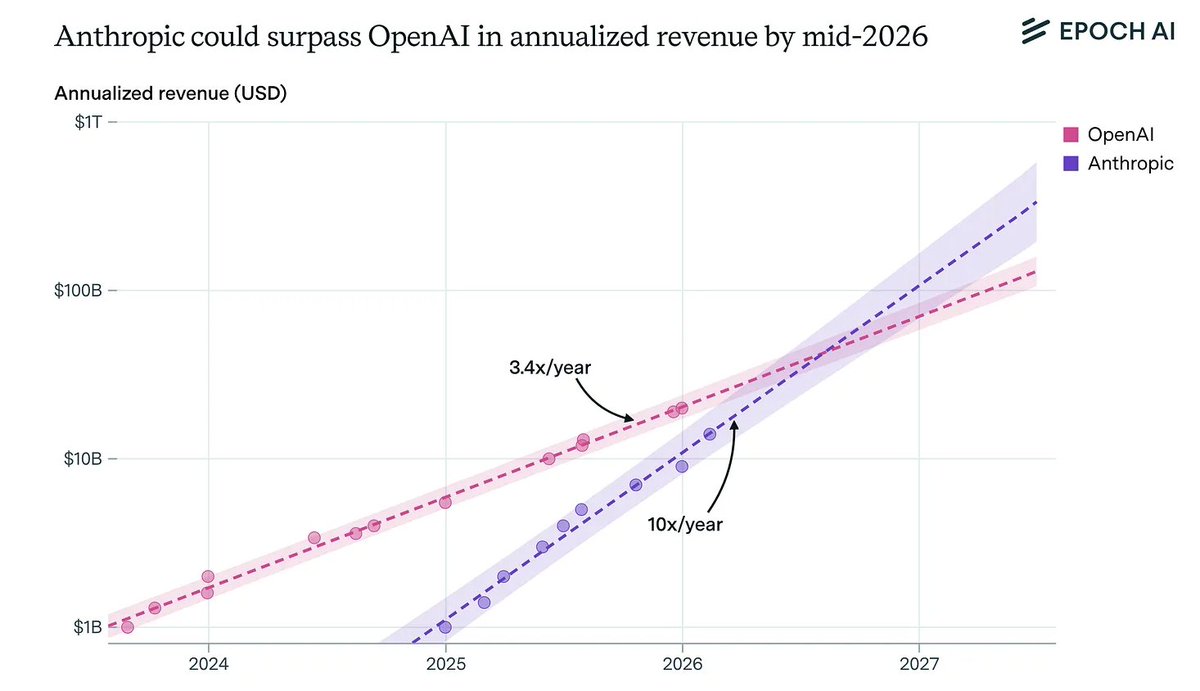

going to be honest, this surprised me. but it’s reflected in the latest funding rounds. openai’s feb 2026 valuation was ~$850b and anthropic’s was ~$380b. based on expected 2026 revenue, openai is trading around ~31x revenue while anthropic is ~44x. so certainly expected that anthropic will grow faster.