Infrastructure Capital Advisors, LLC (ICA) is an SEC-registered investment adviser managing a number of ETFs & hedge funds. Launched in 2012 and located in NYC.

Williams Companies: +23% YTD. Energy Transfer: +18%. ET guides $17.45-$17.85B adjusted EBITDA for 2026, up 9-12% YoY. Distribution coverage near 1.8x on a 7.1% yield.

The Alerian MLP Index has returned 14.2% YTD, outperforming the S&P 500 by a wide margin. Midstream operators function as toll roads for the energy economy. The war premium amplifies a structural thesis.

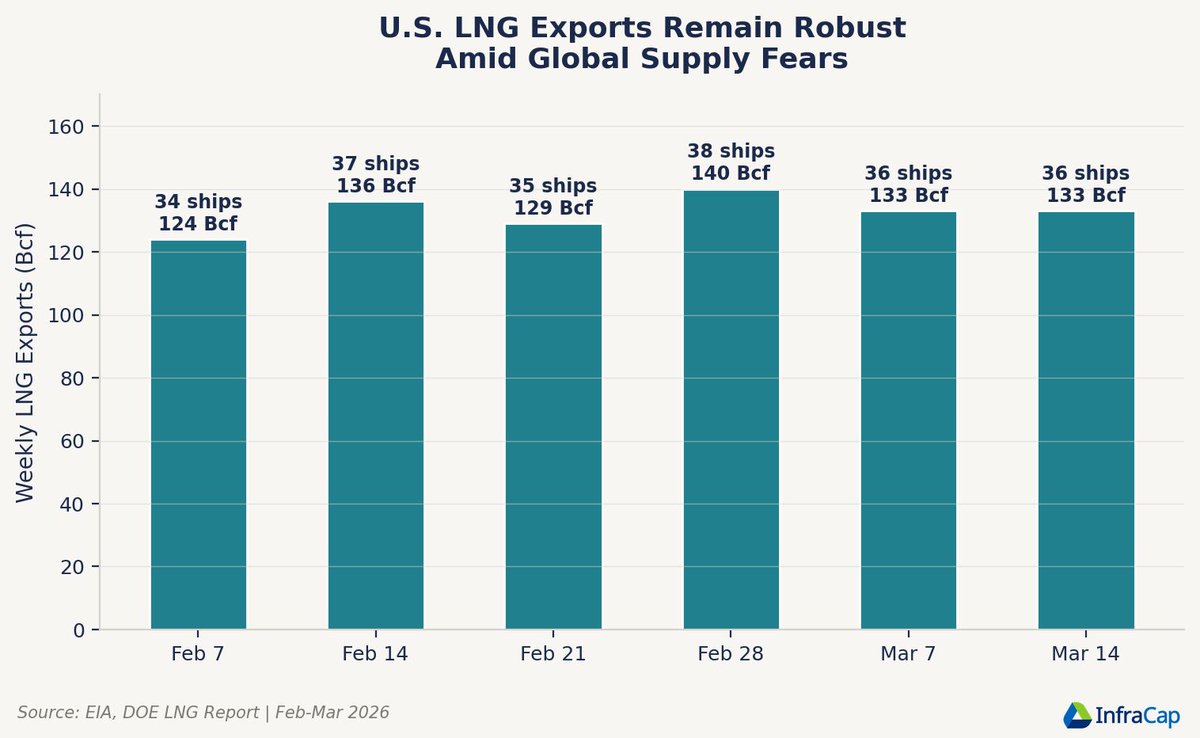

36 LNG carriers departed U.S. export terminals the week of March 14, carrying 133 Bcf. U.S. LNG capacity has nearly doubled since 2020 to 16.2 Bcf/day. American gas fills the global supply gap.

Brent crude breached $110 on March 18 after Israel struck Iran’s South Pars gas field. Prices are up 40%+ since the conflict began. The energy map is being redrawn in real time.

Russell 2000 companies face a $368 billion maturity wall in 2026. Refinancing at 6.5% vs. pandemic-era rates of 1-2%. The largest single-year refinancing burden in the index’s history.

~41-46% of Russell 2000 debt is floating-rate vs. below 10% for the S&P 500. The Fed held at 3.50-3.75% on March 18 and projected just one cut in 2026. No relief in sight.

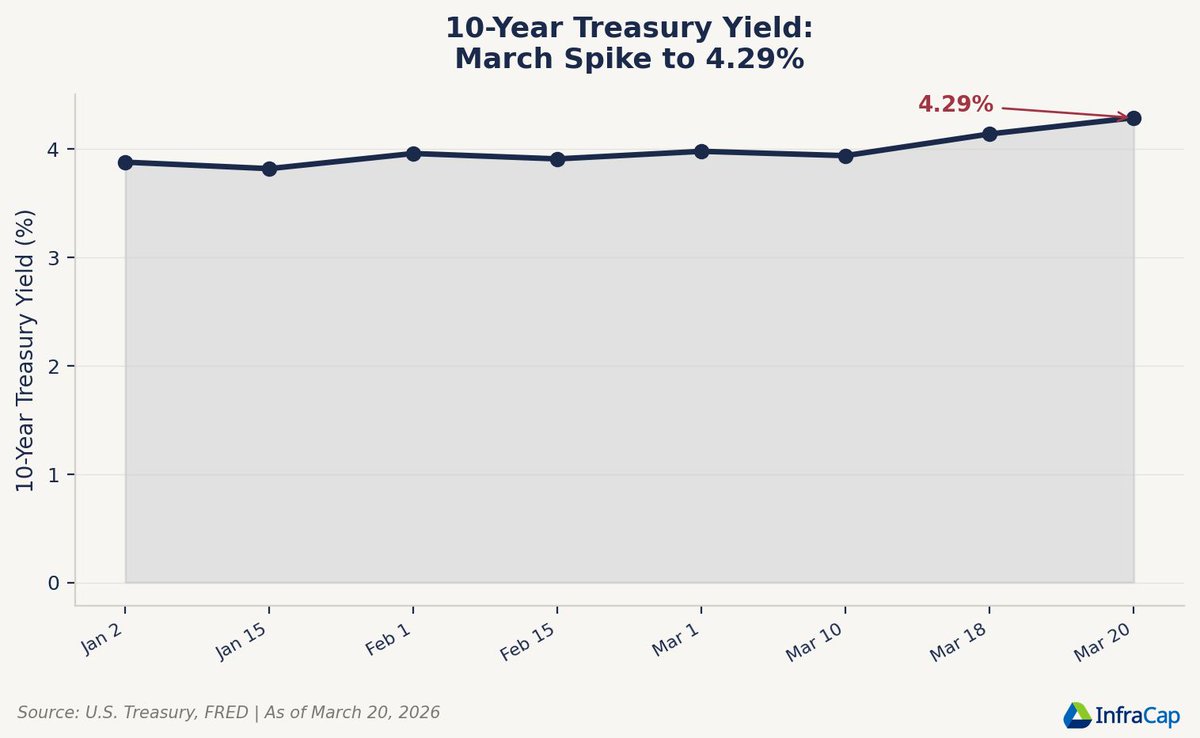

The 10-year Treasury yield climbed from 3.94% to 4.29% in eight sessions. For small caps where 41% of debt is floating-rate, every basis point higher means direct margin compression.

Russell 2000: +8.9% YTD on March 10. Just +0.75% by March 20. Ten trading days erased three months of gains. The sharpest small-cap reversal in recent memory.

BB-rated bonds now represent 58% of the HY index, an all-time high. CCC has dropped below 10%. The riskiest leveraged buyout financing migrated to private credit. Public HY quality has never been stronger.

Public HY ended February at 6.84% yield, 312 bps spread. Private credit spreads have blown past 600 bps. The divergence between public and private credit markets has not been this wide in a decade.

BlackRock Credit (BCRED) saw its largest quarterly redemption wave on record in early 2026. Investors pulled nearly 8% of net asset value. Blue Owl restricted withdrawals in February. Sixth Street calls it a multi-year reckoning.

The Cliffwater BDC Index has fallen 9.7% YTD through March 20. Private credit entered 2026 as a consensus favorite. The first quarter has tested that conviction with the sharpest drawdown since 2020.

Investment-grade spreads at 88 bps sit near multi-decade lows. The 20-year average is 148 bps. Selectivity matters more than ever when compensation is this compressed.

HY credit spreads widened from 264 bps in January to 312 bps by late February. Still well below the long-term average of 520 bps, but the direction matters.

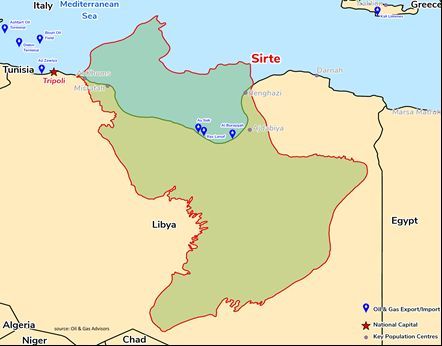

Chevron is planting flags in new basins: Libya awarded it an exploration license in the Sirte S4 Basin as the country tries to pull in foreign capital and rebuild output potential.

Source: Reuters

AI clusters are only as fast as the network between GPUs.

Cisco launched its Silicon One G300 switching chip and new systems aimed at hyperscale AI data centers, taking direct aim at competitors in the networking stack.

Source: Economic Times

Portfolio pruning is strategy, not just housekeeping.

Coca-Cola is phasing out frozen products in the US and Canada, shifting its focus toward higher-demand categories such as reduced-sugar and premium offerings.

Source: MMR