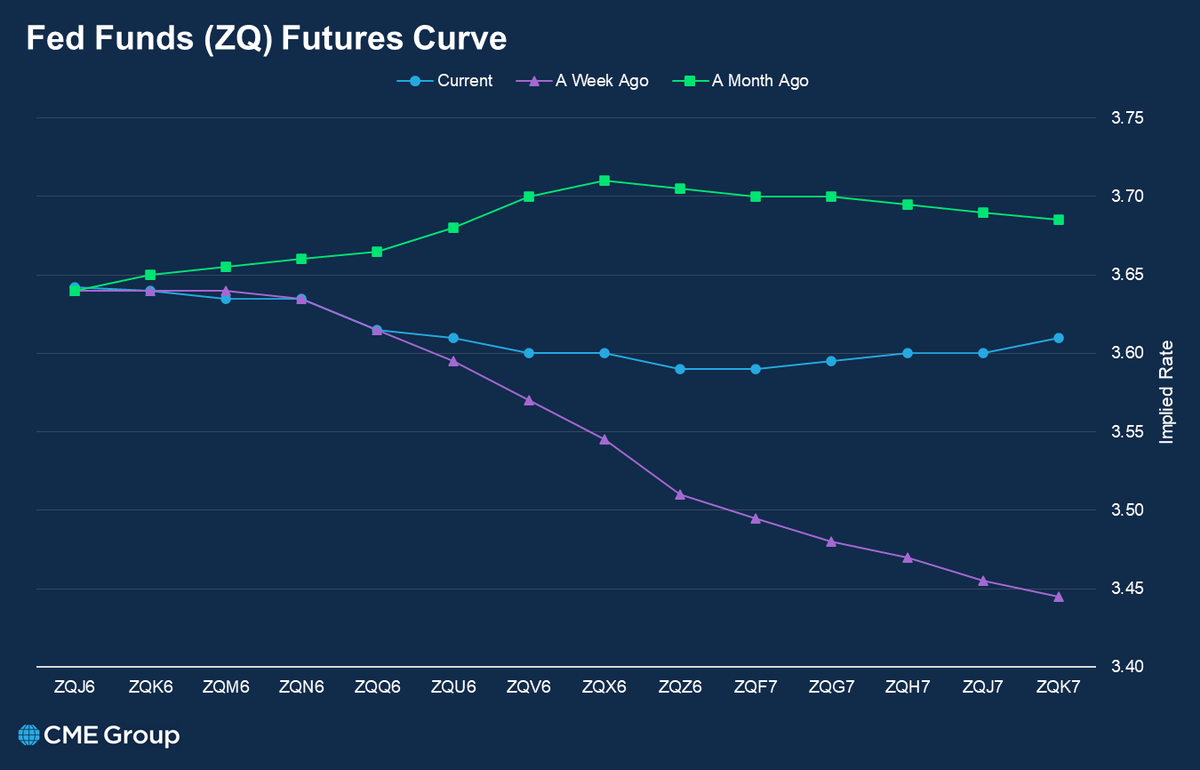

Asset managers have built their largest net short position in Fed Funds futures since early 2023, a year that saw the Fed hike four times.

Chart via @quikstrike1

The Warsh era begins with key growth data and EU inflation reports:

Mon: Memorial Day 🇺🇸 (U.S. Markets Closed)

Tue: Auctions: T-Bills ($166B) & 2-Yr ($69B)

Wed: 5-Yr Auction ($70B)

Thu: U.S. GDP Growth, PCE & Personal Income, 7-Yr Auction ($44B)

Fri: Inflation (🇮🇹, 🇩🇪, 🇫🇷)

#SOFR M6M7 spread hits 40 bps.

The spread between Jun26 and Jun27 SOFR futures has risen over 92 bps since late Feb, as inflation concerns have fueled a dramatic shift in market expectations from cuts to hikes.

After a hot CPI reading in the U.S., inflation reports go global this week

Mon: T-Bill Auctions ($166B)

Tue: Canada Inflation, Japan GDP Growth

Wed: UK Inflation, 20-Yr Auction ($16B), FOMC Minutes

Thu: Philly Fed, 10-Yr TIPS Auction ($19B)

Fri: Japan Inflation

After a strong jobs report, markets pivot to funding and inflation.

Mon: Auctions: T-Bills ($166B) & 3-Yr ($58B)

Tue: Auctions: 52-Wk ($50B) & 10-Yr ($42B), CPI

Wed: 30-Yr Auction ($25B), PPI

Thu: Retail Sales

Fri: Industrial Production

#SOFR M6M7 spread, +12bps today, has gained over 70bps since Feb 27.

SR3M7, the tail wagging the spread, reflects a 91bp increase in expected SOFR over that period.

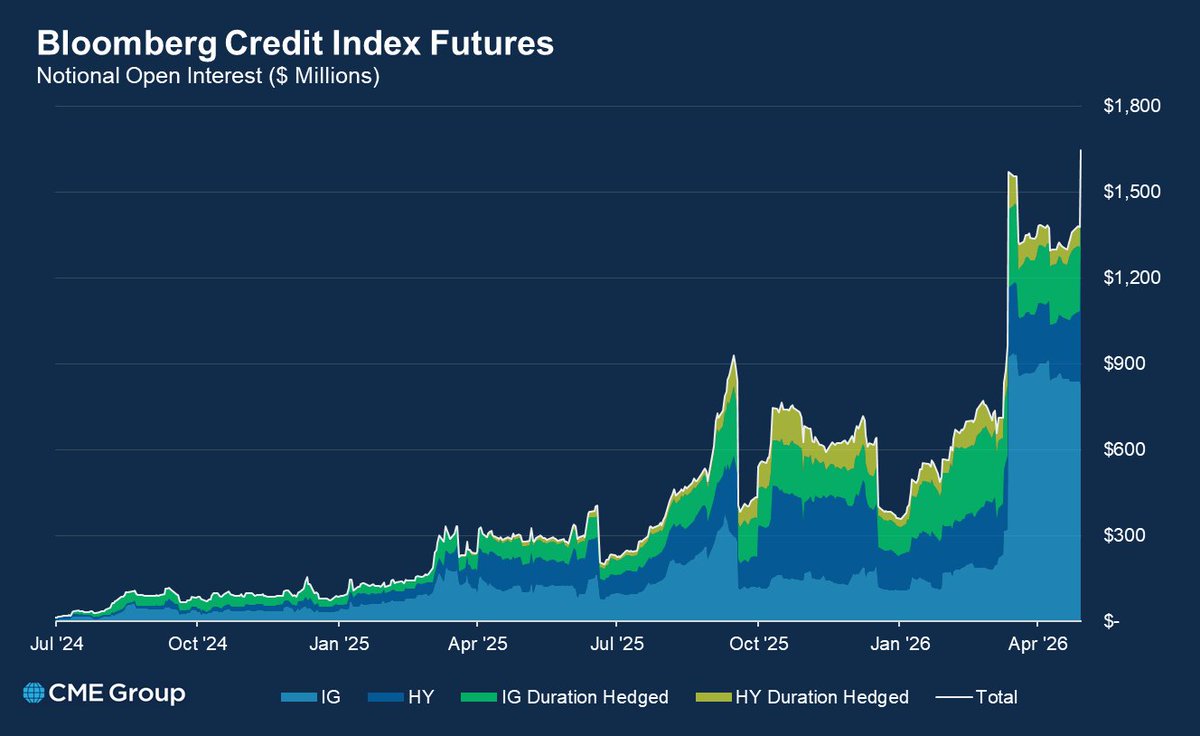

🇺🇸 Credit futures attracting institutional flows.

Open interest just surpassed 15,000 contracts (~$1.65B), driven by deep screen liquidity and record-sized block trading in High Yield futures.