$GME - A reminder to start off your week that @TheUltimator5's BottomFinder has been triggered on the MONTHLY chart.

This has happened exactly one other time since 2020: April 2024.

BREAKING: In brand new exclusive interview with Barron’s Ryan Cohen says $GME still wants to buy eBay, rips their BoD 🚨.

“I want to own eBay,�� Cohen says. “I want to own it for the long term. It’s a great business that’s been poorly managed.”

On rejected offer: “It’s not surprising. We presented a highly credible offer, and it’s exactly what you would expect from a professional board and management team that’s not aligned with shareholders. So, it’s par for the course.”

As the final ticker hits the tape, I am resharing for everyone that missed this due to posting in the late hour.

We will see some major $GME announcements soon.

Will it make or break this lens?

Clearing the Board: What Every Institution Sees That Retail Doesn't

$GME just posted the best quarter in its history.

$389.6 million in net income.

Revenue up 14%.

Operating income of $143.3 million.

The stock is trading at roughly $3.50 above its cash per share.

The market is assigning almost no value to the operating business. Zero probability to the $EBAY deal closing.

This is not the market rejecting the company.

This is the market waiting for an announcement it believes is coming but hasn't arrived yet.

And if you look at who is behaving how, you can see exactly what that announcement is.

------------------------------

THE REJECTION

On May 3, Cohen bid $125 per share for $EBAY (half cash, half $GME stock).

A $10 billion retailer offering its own equity as half the consideration for a $48 billion acquisition.

$EBAY could not say yes to that.

The stock component alone made the bid structurally unacceptable.

Then on May 11, GameStop filed its preliminary proxy, and in it was a surprise alongside the previously announced CEO performance award: a request for 2.5 billion authorized shares.

No prior indication it was coming.

The next morning, $EBAY rejected the bid.

"Neither credible nor attractive."

The rejection cited financing uncertainty, leverage concerns, and governance structure.

But the speed says more than the language.

They were not evaluating the deal.

They were looking for something specific, and it was not there.

What was missing was any language about a holding company. The only thing that could make this bid credible.

$EBAY's board cannot accept this bid.

The bid was unacceptable before the proxy landed.

The proxy made it worse by threatening dilution at a scale that would destroy the stock component - while simultaneously signaling a structure that would change the identity of the acquirer entirely.

But that structure has not been announced so there is nothing for eBay to say yes to, so they rejected.

And they are waiting.

They are not the only ones.

------------------------------

THE LEVERAGE WALL

Michael Burry sold his entire $GME position on May 5. Two days after the bid.

His analysis was straightforward: the combined entity's leverage would reach approximately 7.7 times Debt/EBITDA.

"Wall Street does indeed mistake debt for creativity,"

CNBC reported that the TD Securities highly confident letter requires the combined entity to maintain an investment-grade credit profile.

That's condition one.

GameStop is not investment grade.

The financing condition fails under the proposed structure.

The deal, as structured, is dead on arrival.

Everyone agrees on this math.

The leverage does not work if GameStop is the acquirer.

And that is the point only retail is missing.

------------------------------

THE HOLDCO SOLVES EVERYTHING THEY'RE OBJECTING TO

Every major objection to this deal - from Burry, from eBay's board, to wall street Wall Street - is an objection to GameStop being the acquiring entity.

A $10 billion specialty retailer cannot credibly absorb a company four times its size while maintaining investment-grade credit.

But what if GameStop is not the acquirer?

IDENTITY.

The acquirer is no longer a video game retailer.

It is a diversified holding company.

Institutional investors, rating agencies, and target boards evaluate holding companies differently than single-segment retailers.

CAPITAL STRUCTURE.

A holdco raises capital at the parent level (equity from strategic co-investors, sovereign wealth fund participation, holdco-level debt) without loading the operating subsidiary's balance sheet.

The leverage that breaks the deal under a GameStop acquisition can be restructured across a holdco with multiple subsidiaries and diversified revenue.

FINANCING.

Cohen has referenced sovereign wealth fund participation but has never explained the vehicle.

Sovereign wealth funds do not invest in specialty retailers.

They invest in holding companies with diversified assets and a credible long-term acquisition strategy.

The reason Cohen has not explained the SWF component may be that the entity it flows through does not publicly exist yet.

Burry's leverage math is correct for the entity he analyzed.

His conclusion is correct for GameStop as it currently exists.

But the same math produces a different answer under a different corporate structure.

The market sees a company trading at its cash floor after record earnings, waiting for a structural catalyst.

------------------------------

THE EVIDENCE

The 2.5 billion share authorization does not make sense for a company with 448 million shares outstanding and a shrinking retail footprint.

It makes sense as authorized capital for a new parent entity for acquisition currency, equity issuance capacity, and structural flexibility for future deals.

The $2 billion buyback does not make sense as traditional capital return for a company about to spend $55 billion on an acquisition.

It makes sense as float reduction before a share conversion where every share bought back is one fewer share that converts to holdco equity, concentrating ownership for existing holders.

The CEO performance award does not make sense for a video game retailer.

It makes sense for the CEO of a holding company that intends to grow through acquisition.

Each of these individually could be explained away.

Together, they form a pattern that eBay's board, Wall Street's institutional desks, and the options market all appear to recognize.

The only constituency still debating whether this is a holdco play is retail.

------------------------------

THE CALENDAR

@ryancohen ran a daily pressure campaign from May 3 through May 29.

SEC filings, stake increases, interviews, escalating public attacks on eBay management.

He moved $GME's AGM from early June to July 7.

He dropped earnings a week before anyone expected them, clearing the window that was originally expected to hold both the AGM and the earnings date.

He created dead space on both sides of eBay's June 17 AGM.

A full week before.

Two and a half weeks after.

Cohen currently holds derivative exposure to approximately 7.5% of $EBAY.

The question is not whether a holdco announcement is coming.

The question is whether it arrives before June 17, reshaping how institutions vote on Proposal 4 at eBay's AGM, or after in the dead space before GameStop's July 7 AGM.

------------------------------

TL;DR:

Retail is debating whether the deal can close. Whether Cohen is serious. Whether the stock is undervalued.

These are the wrong questions.

The right question is why a company that just posted its best quarter in history is trading at its cash floor.

And why every institutional participant - eBay's board, TD Securities, the options market - is behaving as though they are waiting for a specific structural event rather than reacting to the information already public.

Burry looked at the deal and saw a retailer taking on 7.7x leverage.

He was right about the math.

He was wrong about the entity.

The market is not confused about the earnings. It is not confused about the cash.

It is waiting for the structure that makes the rest of the strategy legible.

The pieces are on the table. They have not been assembled yet.

Where to start.

Well I think this might be the most significant earnings report in GameStop history.

There are so many headline numbers of high importance. How do I rank them.

#1 Revenue beat and increase YoY. This can finally be crossed off the bear thesis side of the sheet for whoever still maintains it. On fewer stores than ever. Incredible turn.

#2 Margin. No scratch that - UPDATED THE SHARE REPURCHASE AUTHORIZATION TO $2 BILLION. LET'S GO. Almost 3.5 years ago I asked the board for this. And while, yes, we did sell shares two years ago at $20, we can afford to start buying back shares now, because...

#3 $389.6m in net income for the quarter. Extrapolate that out. GameStop can make $1.6b a year now. That new share repurchase authorization? Paid for in 5 quarters. This is how the story began, the large share repurchase in 2019. Maybe this story just starts over again right here this year.

#4 $143.3m in operating income. OPERATING INCOME. That means not only is the inner shell of the company (cash) expanding, but the second level (operation) is expanding and could soon break out with a new multiple as margin grows and TTM EPS grows. This is very good news for the quarters to come.

Excited to see the 10Q. Hope you all have a great evening. Let's go GameStop!

✍️✍️ $GME Earnings Grade: A

This wasn't just a beat... this was a statement.

📈 Revenue +14%

📈 Record Q1 operating income

📈 Record quarterly net income ($389.6M)

📈 Gross margins jumped to 40.7%

📈 Cash pile now $9.7B

📈 New $2B buyback approved

The old GameStop was fighting to survive.

The new GameStop is printing cash, buying back stock, and sitting on a war chest big enough to make shorts uncomfortable.

Ryan Cohen continues to execute.

#GME #GameStop

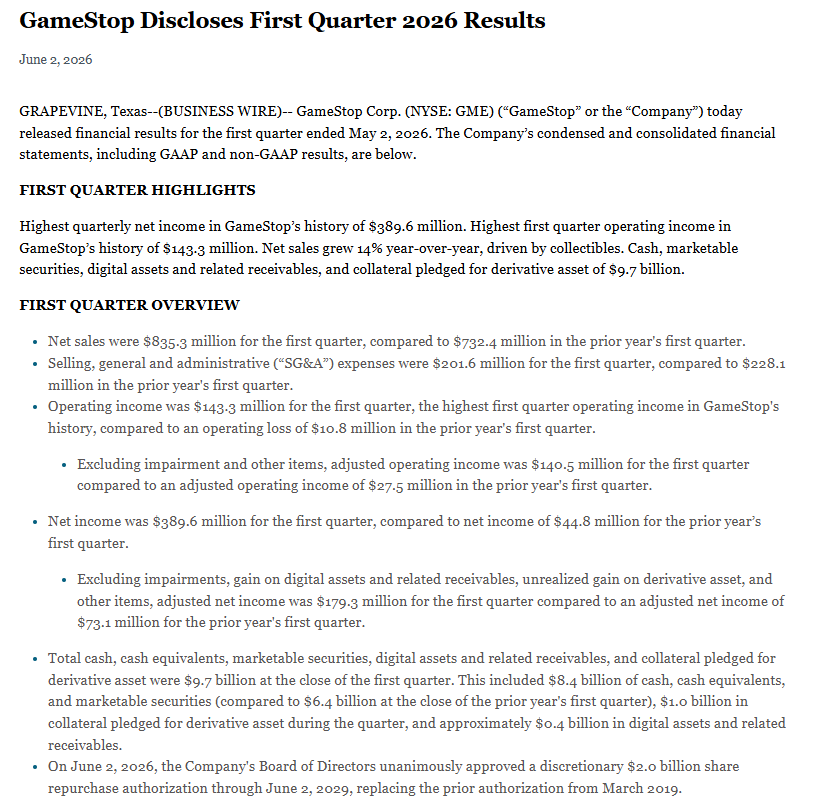

$GME Operating income was $143-3 million for the first quarter, the highest first quarter operating income in GameStop's history, compared to an operating loss of $10.8 million in the prior year's first quarter.

Excluding impairment and other items, adjusted operating income was $140.5 million for the first quarter compared to an adjusted operating income of $27.5 million in the prior year's first quarter.

Source: First Quarter 2026 Results

Question of the day is where's the Babe Ruth.

Welp, we're very close to the cash per share floor on low volume with extremely negative social sentiment. That's a pretty great setup.

Is it soon? Tough to say.

People might remember that on 2/2 I said that was probably our top and we'd likely fall down into Feb Opex and then March Opex before bottoming 5 weeks after earnings 5/1 when IV typically hits a low.

Instead, Implied Volatility hit a 7 year low April 13th, bonds le-legended (if that matters) and we spiked on 5/1 into the eBay announcement. Now we are deeply compressed a month later following the request to increase authorized shares leading into Q1 earnings.

So our cadence is a month off from what I had expected back on 2/2 but we got our dip.

Could the stock rally strongly here into 11 days of volume?

Perhaps.

I like the setup here a lot, it's just later than I expected back in January, but does make sense given all the events that have happened this year.

The more important thing I want to remind anybody following along is that this is likely to happen again. I'm not saying it will, but the chart below is fairly self evident. For some reason the stock returns to the cash per share floor on a somewhat regular cadence.

So the pain I feel right now I want to remember. And the social sentiment I want to remember. Because when it comes again in the months to come, I am going to be reading the same posts on Reddit, 4chan, and Twitter, about how GameStop is a terrible investment, opportunity cost, bagholding, etc.

But I will remember and I will look back to the last time all those things happened and what I did that was correct and what I did that was incorrect and I will try to make good decisions (for me) again.

I hope you are able to make good decisions for you, too. I don't know what those are.

These moments are challenging, though, but after 20+ times I am honestly kind of numb to it and just mechanically buy the dip and wait patiently for the rip.

If you are new, well, welcome to the show.