@smarter411 Hi @smarter411 I’m new here. So when I see such post, does that mean I should be closing the trade as I was only looking for the flag and hence missed to sell this at better price.

Season’s Greetings from https://t.co/tTTmlEhK5m! 🎄🎅

As we celebrate this wonderful time of year, we want to extend our warmest Christmas wishes to our entire community.

Since launching earlier this year, https://t.co/tTTmlEhK5m has been met with an incredible response - from highly engaged users and enthusiastic followers to thoughtful feedback and encouragement that have exceeded our expectations.🎁

We are proud of the vibrant and growing community that has formed around our platform and are deeply grateful for the trust and support you have shown us. Thank You! ✨

Your engagement continues to inspire us to innovate, improve and deliver a high-quality financial platform that truly adds value.

From all of us at https://t.co/tTTmlEhK5m, we wish you a very Merry Christmas and a joyful, prosperous and successful 2026.

With gratitude,

The https://t.co/tTTmlEhK5m Team

#Moneyvize #Investing #StockMarket #FinTwit #Fintech #Christmas2025 #ThankYou #SeasonsGreetings

$NKE Q2'26 Earnings Report from https://t.co/tTTmlEhK5m.

#NKE Q2’26 Earnings — Beat, but Market Wasn’t Impressed

Nike reported a solid Q2 FY26 print, beating expectations on both the top and bottom line. Revenue came in at $12.43B vs $12.21B expected, while EPS surprised meaningfully at $0.53 vs $0.37 estimates. The quarter showed disciplined cost management, with operating income of $1.01B and net income of $792M, highlighting that execution remains intact despite a challenging consumer backdrop.

However, the stock sold off sharply because the market focused less on the backward-looking beat and more on the forward outlook. Management’s commentary pointed to continued pressure from uneven consumer demand, promotional intensity, and margin normalization. With #NKE still trading at a premium multiple, investors were looking for clearer signs of demand re-acceleration rather than earnings driven largely by cost control.

In short, this was a case of “beat the numbers, miss the narrative.” The earnings were good, but not strong enough to justify the valuation without improved visibility on growth and margins. Near-term performance will now hinge on guidance clarity, demand trends, and Nike’s ability to re-establish consistent top-line momentum.

Login to https://t.co/tTTmlEhK5m — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#NKE #Nike #ConsumerCyclical #Apparel #Retail #Footwear #AthleticWear #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize

Not investment advice.

EOD Market Heatmap and Session analysis from https://t.co/tTTmlEhK5m.

Markets closed red again today, with the S&P500 and #NASDAQ slipping as traders stayed risk-off heading into a data-heavy week.

Tech was mixed but heavyweights dragged: $AAPL fell -1.5%, $MSFT -0.8%, $GOOGL slightly red and $AMZN down -1.6%.

Semis were split — $NVDA managed to stay green, but $AVGO got hit hard (-5.6%) after continued concerns around AI capex normalization and valuation compression. Software wasn’t spared either with $ORCL, $CRM, $NFLX, and $PLTR all under pressure. On the flip side, defensives and select growth pockets held up: $LLY surged over +3% in healthcare, $TSLA jumped +3.6% in consumer durables, and $BRK.B outperformed financials as banks like $JPM stayed choppy.

Macro is the main culprit for today’s weakness. Investors are de-risking ahead of key inflation and labor data later this week, which will heavily influence Fed expectations going into year-end. There’s also lingering uncertainty around U.S. budget negotiations and shutdown risk, keeping volatility elevated and limiting upside follow-through. With 2025 gains already locked in for many funds, this feels like classic December positioning + profit-taking, especially in mega-cap tech.

Commodities & crypto painted the risk-off picture clearly:

• #Gold moved higher as yields eased and safe-haven demand picked up

• #Silver followed gold with modest gains

• #CrudeOil drifted lower on demand concerns and global growth uncertainty

• #Crypto traded mixed to lower, with #Bitcoin and majors losing momentum as liquidity rotated out of risk assets

What to expect next: markets are likely to stay choppy until inflation and jobs data land. If numbers come in cooler, expect a relief bounce led by tech and growth. Hot data or negative shutdown headlines could extend this pullback. For now, the tape says rotation > risk-on, with defensives, healthcare, and selective names outperforming while big tech digests gains.

https://t.co/tTTmlEhK5m makes it easier to spot where strength and weakness are concentrated — whether you’re tracking daily movers or looking for value in recently sold-off names.

Our heatmap isn't just a picture—it's a launchpad. Click any stock to instantly visualize the fundamentals driving its unique move!

#MarketHeatmap #Investing #AIPowered #Moneyvize #TechStocks #Inflation #StockMarket #Visualization #ratecut #Labormarket #Fed #EarningsSeason #Earnings #EarningsReport #AISpending #AIValuation #Crypto #Gold #Silver #CrudeOil #FOMC #jobreport

Not investment advice.

$LULU Q3'25 Earnings Report from https://t.co/tTTmlEhK5m.

#LULU Q3 FY’25 Earnings & Stock Reaction

Lululemon reported Q3 FY 2025 revenue of $2.57 B and EPS of $2.59, both smashing estimates, driven by a 7% global sales gain and strong international growth, even as U.S. comps softened. The board also authorized a $1 billion increase to its stock buyback program, reinforcing confidence in the business. Investors rewarded the earnings beat and capital return plan, lifting the stock over 11% in today's trading.

Guidance & Leadership Change:

For Q4 FY 2025, Lululemon guided revenue of $3.50 B–$3.585 B and EPS of $4.66–$4.76, slightly shy of higher Wall Street expectations, though still reflecting solid demand amid calendar shifts and tariff headwinds.

Full-year FY 2025 guidance was reaffirmed/raised to ~$10.96 B–$11.05 B in sales and EPS of $12.92–$13.02, which helped underpin confidence despite margin pressures.

At the same time, CEO Calvin McDonald announced he will step down in January 2026, with interim co-CEOs stepping in while a search for a new leader begins, a move markets interpreted as a potential reset.

What to Watch Into 2026:

Going into 2026, keep an eye on same-store sales trends in the U.S. and product innovation, as recent softness in core categories has been a concern. Tariff impacts and promotional activity could continue to pressure margins, so execution on inventory and cost initiatives will matter.

The leadership transition also creates both risk and opportunity: a new strategic vision could reinvigorate brand momentum, but execution under interim leadership will be critical.

Lastly, the stock had fallen more than 60% from its highs earlier this year, but it has been attempting to recover since the September low. Today’s rally helps regain some of that lost ground, underscoring just how volatile investor sentiment has been throughout the year.

Login to https://t.co/tTTmlEhK5m — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#LULU #LuluLemon #ConsumerCyclical #Apparel #Retail #athleticwear #Lifestyle #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize

Not investment advice.

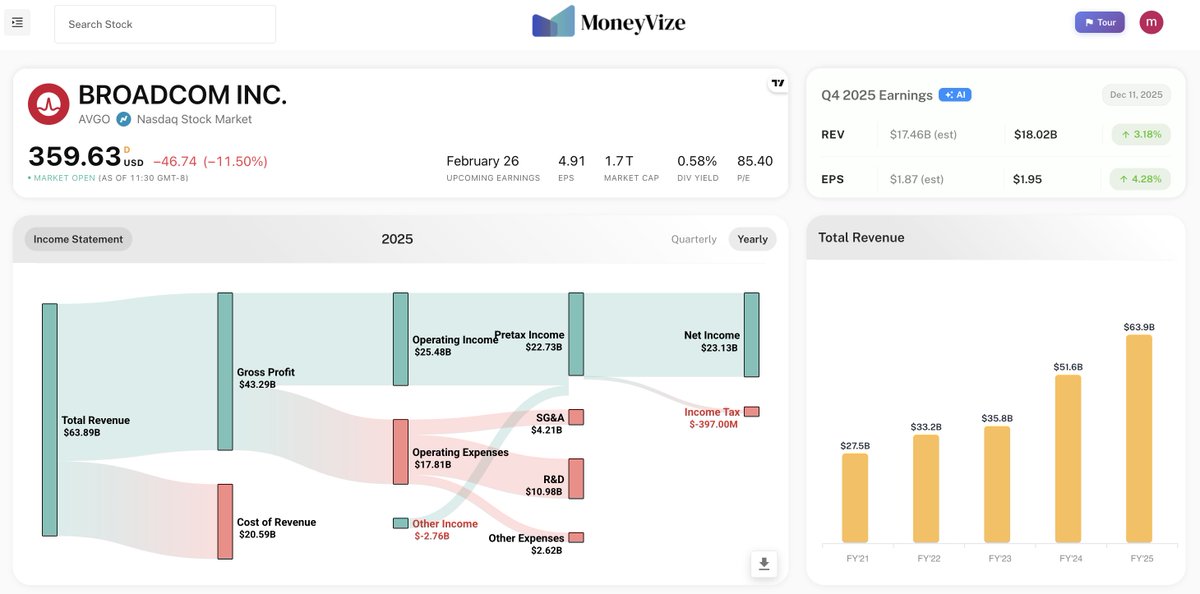

$AVGO Q4 and FY'25 Earnings Report from https://t.co/tTTmlEhK5m.

#AVGO Q4 & FY’25 earnings beat estimates and the market reaction has been wild.

#Broadcom reported Q4 revenue of ~$18.02 B, up ~28% YoY, and non-GAAP EPS of $1.95, both beating Wall Street expectations substantially. The company also raised its quarterly dividend by 10% and delivered record FY 2025 revenue of ~$63.9 B with strong free cash flow and earnings growth. AI semiconductor sales were a standout, with revenue up sharply and Broadcom forecasting those products to double year-over-year next quarter to ~$8.2 B.

The official guidance for Q1 FY’26 calls for ~ $19.1 B in revenue (also above consensus) and adjusted EBITDA around 67% of sales. That paints a picture of continued growth against a backdrop of strong secular demand.

So why did the stock drop more than 11%?

The short answer is expectations vs reality.

Even though #Broadcom beat on the quarter and issued solid near-term guidance, investors seemed disappointed by margin commentary and forward outlook tone. Management highlighted that AI system/server revenues carry lower gross margins, and while overall guidance was strong in absolute terms, it didn’t satisfy the super-charged expectations priced into the shares after a massive run to new highs this year.

There was also some investor consternation that the AI backlog (~$73 B) and customer disclosures weren’t as jaw-dropping as some had hoped, especially given how much the stock had rallied on AI narrative. Analysts saw this as a signal that margins could compress and growth might be a bit slower than the “AI hypergrowth” story implied.

In short, #AVGO delivered strong beats and healthy guidance, but investors punished the stock because the tone around profitability trends and long-term cadence felt more measured than expected. This is a classic case of a beat & guide that was good — just not good enough for a hype-driven market. As always, the numbers look solid, but the stock market looks forward — and that makes a huge difference.

Bull Case:

Broadcom is positioned to benefit from strong AI infrastructure demand, with AI chip revenue expected to double and a multibillion-dollar hyperscaler backlog supporting visibility into 2025. Q1 guidance above consensus indicates continued top-line strength, and recurring software revenue from VMware adds stability. If AI ASIC wins expand and margins stabilize, AVGO could sustain double-digit growth and multiple expansion.

Bear Case:

Rising AI system revenue carries lower margins, creating pressure on gross profitability even as sales grow. Heavy reliance on a small number of hyperscaler customers increases concentration and cyclicality risk. Competition from NVIDIA and AMD in AI silicon and ongoing VMware integration challenges could slow earnings growth, leaving AVGO vulnerable to valuation compression.

Login to https://t.co/tTTmlEhK5m — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#AVGO #Broadcom #Semiconductors #AIBuildOut #CustomAIChips #HyperScalers #AIInfranstructure #AIValuations #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize #MSFT #AMD #NVDA #GOOGL

Not investment advice.