The space economy is no longer a concept. It's a market. And Shift4 is helping to power it.

We power recurring subscription revenue for @Starlink's global satellite network.

We process crypto & stablecoin payments for @BlueOrigin spaceflights.

Today, as @SpaceX makes history on Nasdaq, we're proud to be the infrastructure behind this industry's commerce — from orbit to your doorstep.

Congratulations SpaceX!

$FOUR 🛰️

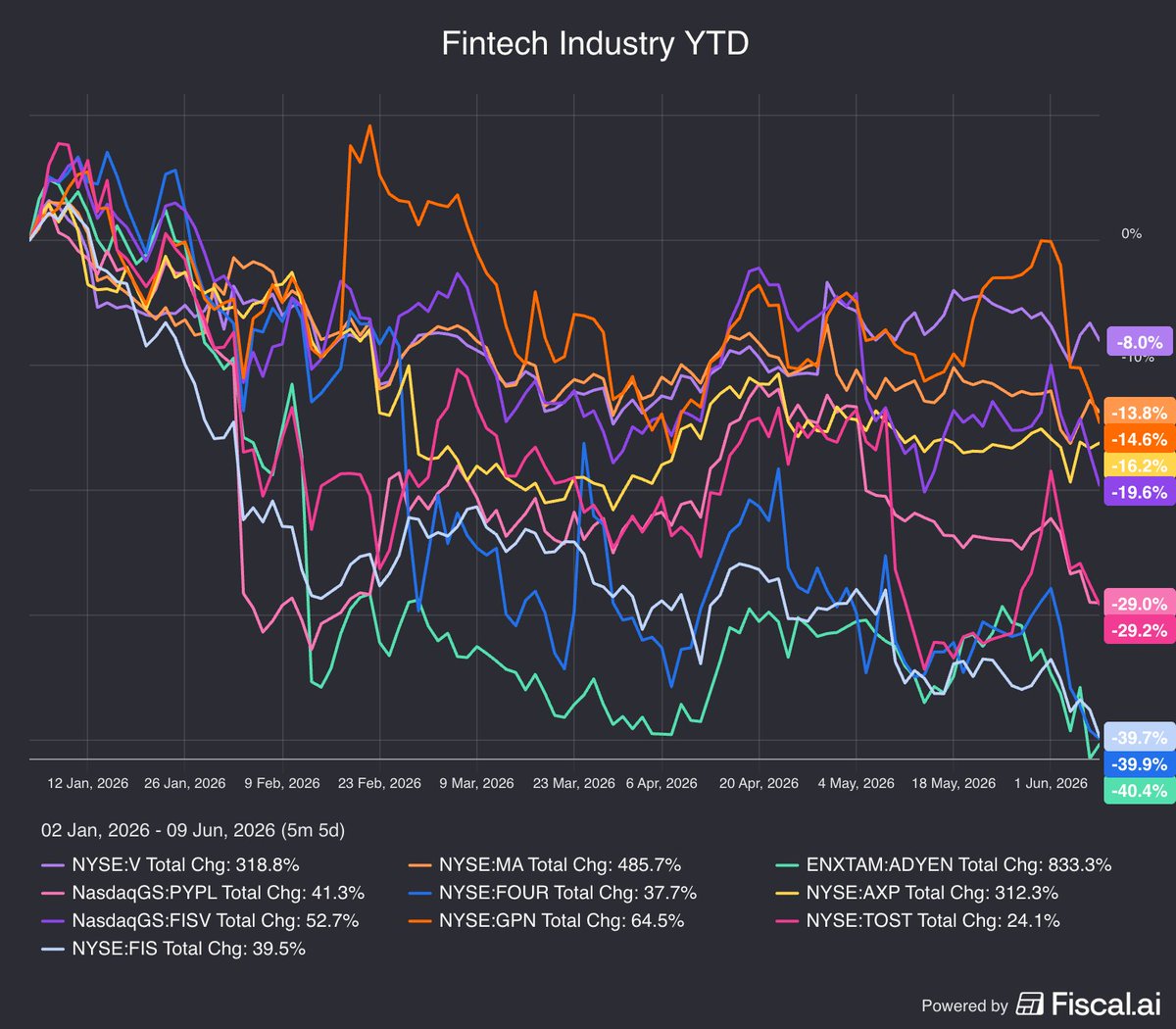

$FOUR hit $34 yesterday. That's a 73% drawdown from the Feb 2025 peak.

At these levels, the same questions keep coming up: Takeover, take it private (@rookisaacman floated that himself back in 2022), buybacks, and why public payment names trade so far below private ones.

I asked @tlaubers about a lot of this directly a few weeks ago. His answer 👇

~5x forward FCF, Americas core growing 15%, international at 51%. Everyone's debating takeovers, but why wouldn't you just own a business that generates its whole market cap in free cash flow in ~5 years, and growing?

Credit to @tlaubers and the team for getting through what's probably the hardest stretch @Shift4 has been through. They keep executing, tightening the product and the value prop.

None of this is fun at the lows, but +10% today shows how fast it flips. Sentiment turns way quicker than the fundamentals ever did.

What the Street sees:

"MELI is growing the loan book way too fast. They must be loosening their risk parameters to do this. There's no way NPLs don't ramp up."

What I see:

$MELI has incredible first-party financial data on the people they offer loans to. They see their financial behaviors in real time all throughout the entire ecosystem. This is data and visibility that banks don't have. Because of this, MELI can build accurate risk models for their customers.

NPLs are flat or falling YoY even though the loan book is ramping. There is no evidence that the quality of the loan book is suffering. It's also worth mentioning that MELI’s many business segments mean that it can more readily absorb temporary unexpected problems, unlike a bank which is more singularly focused.

4/5

I've been tracking the new #Shift4Dine wins daily and found out a few data points:

$TOST has been replaced by @Shift4 in quite a few places. An installer said:

"How many Toast POS systems have we replaced? It's getting hard to keep count..."

#Shift4Dine seems to be up and running in SPAIN, with a few installations reported

The search query if anyone wants to do the same and share insights:

https://t.co/Nkv9CDLh2W

#FOUR

anthropic "mythos" marketing strategy:

opus 4.6 was great, but

> release 4.7, which gives nothing, and burns 10x more tokens

> release 4.8, basically 4.7 with fixed tokens, while 4.6 gets nerfed, so 4.8 wouldn't look bad next to it

> now release Mythos, basically pre-nerf 4.6, slightly better, but burns 5x more tokens

and everyone claps

$VEEV Q1 '27 KPI Summary.

R&D and Quality remains the faster growing subscription segment, up 19.1% YOY vs. Commercial subscription revenue up 10.6% YOY.

What did we think about the quarter?

Bill Ackman (All-In Podcast interview):

“Look, when you're a concentrated investor, or investor generally, and you're a long-term investor, the most important and most challenging thing to do is determine what's the risk of disruption.”

Suppose you make 20 or 30 real long-term bets over the course of your investing lifetime. If you are successful in making sure that your potential downside over the long-term for every one of them is either nothing or very small, what are you left with?

What you have is a collection of bets where all that's left is potential upside. Maybe some work out very well, and maybe some don't. But your starting point is one where you won't lose money. That's an extremely constructive starting point.

Spend 85% of your research time thinking about the downside. Moat, competition, runway, valuation, disruption, risk of the business model itself, the balance sheet. Spend almost all of your time on these things.

Analistas de Wall Street:

“Downgrade para $NU, hay incertidumbre por el nuevo CFO y los márgenes". La acción cae 8% en un día.

Management de $NU:

"Aprobamos US$ 1.000 palos verdes para comprar nuestras propias acciones porque están ridículamente baratas. Nostros ponemos la caja donde ponemos la boca.”

El clásico juego de quién tiene la billetera más grande. Hermosa transferencia de riqueza de las manos débiles al propio corporate.

Capital allocation masterclass.

Que poco $NU tengo. Fua

NFA

Peter Lynch on owning cyclical stocks

"At Magellan, I loaded up on cyclical stocks during the 1981-1982 economic slump.

This strategy was one of the keys to Magellan's success...

The best time to get involved with cyclicals is when the economy is at its weakest, earnings are at their lowest, and public sentiment is at its bleakest.

The staff at Standard & Poor's weekly newsletter, The Outlook, once reviewed the eight recessions since World War II to find out what happened to the prices of key cyclical stocks after the stock market hit bottom.

In every instance, the cyclical groups gained 50 percent or better in five months, more than double the advance of the S&P 500."