@jameslavish A credible YCC “à la 1951” does not need much money printing, does it?. Just the threat of facing the Fed. Not expecting it anytime soon, just thinking

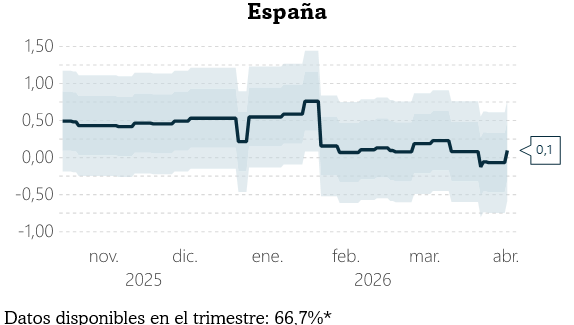

@atalaveraEcon@Manuj_Hidalgo@rdomenechv En @Afi_Research, coincidimos con Airef. Nuestro tracker de PIB de España para el 1T26 anticipa un crecimiento muy flojo (menos de lo contemplado en otros modelos por los que apostamos más en esta ocasión: rango 0.5-0.6% T)... veremos!

@dlacalle Desde 120/día pre-war, no está mal el recovery. La escala del eje importa. También la "bandera" y destino de los barcos. Pero cada uno tiene sus sesgos. BCA el suyo.

Pablo Hernández de Cos, Premio de Economía Emilio Ontiveros 2026.

Reconocimiento a una trayectoria de rigor técnico, vocación de servicio público y contribución al análisis económico y al debate público.

Accede a la nota: https://t.co/EihWcU7XAa

#Economía#PremioEO

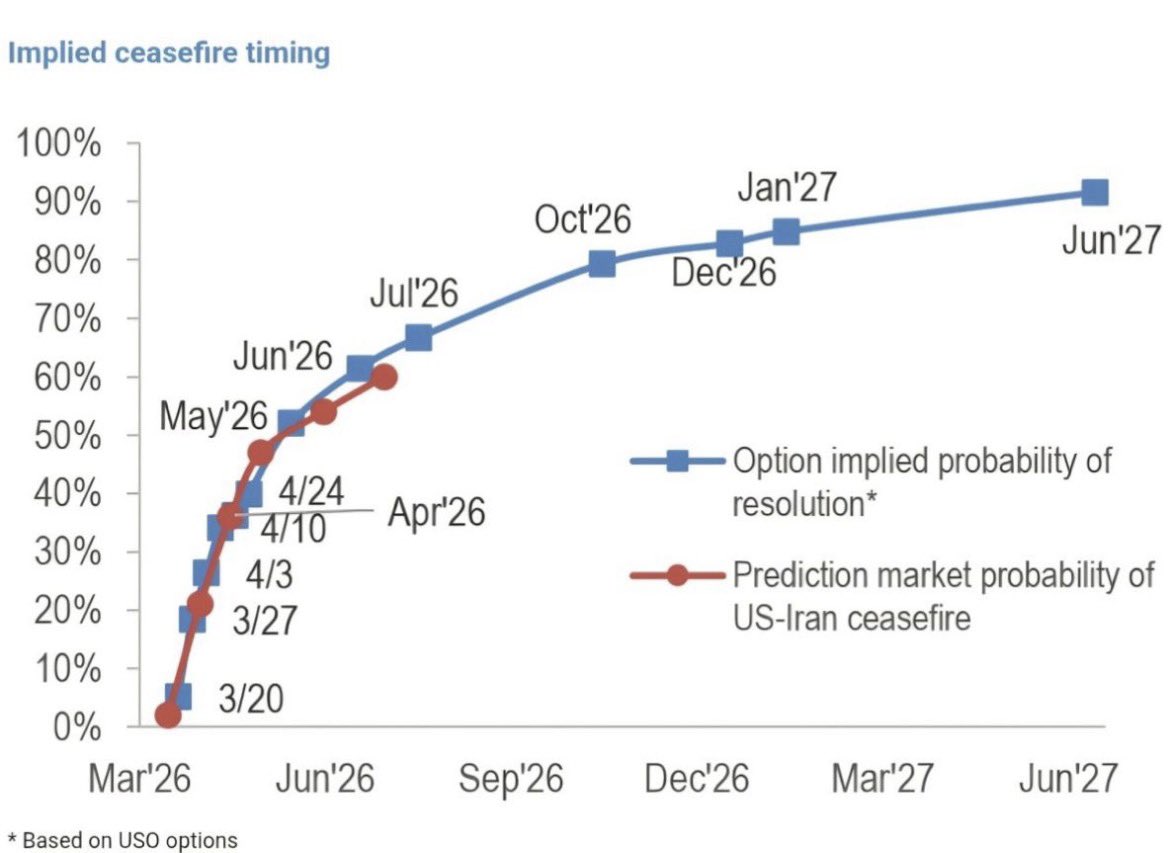

Markets are pricing both the probability and timing of a US–Iran ceasefire. Prediction markets imply ~60% odds by mid-2026, while oil options suggest a gradual resolution with risk fading into 2027. The option surface shows hedging demand, not panic, meaning markets are pricing insurance against shocks rather than a structural supply disruption.

@albertedwards99@FT@hakyungkim_@rbrtrmstrng 5Y5Y is an implicit rate built on 5Y and 10Y breakevens... so it does not make much sense to look at it now. 5Y BEI rises on top of 10Y and the 5Y5Y is below the 10Y BEI. Better concentrate attention in 2-5Y breakevens. Those surely remain well correlated to oil.

En este primer episodio,@JMAafi, socio director de Análisis Económicos y de Mercados de Afi, y Raúl Viñas, analista y experto en geopolítica de Afi, responden a la pregunta: ¿Está la Unión Europea condenada a la irrelevancia #geopolítica?

I find it hard not to have as a central scenario where oil prices will remain very high for a long time, higher than the market current prices.

I am no expert on geo-politics and defense technology, but this is what I think I have learned:

Fully protecting ships in the strait of Hormuz is basically impossible. Not enough time to stop missiles or drones.

There is no reason, whether or not Trump declares that war is over, to think that Iran will not continue for some time to threaten to destroy the ships that try. Why should they stop?

The risk will thus remain sufficiently high that most non Iranian ships will not take the risk.

Thus, the shortfall of 20 million barrels a day is likely to last for long.

The scope for increased supply from elsewhere is very limited in the short run. Perhaps 2 million barrels at the most.

The 400 million barrels reserve release can only add 3-4 million barrels or so daily.

The short run elasticity of demand for oil is very low, at most -0.1, and probably less.

This suggests to me prices closer to 150-200 dollars per barrel (or more, but I hesitate to give higher numbers…) than to the current market price.

To repeat. I am no expert (As an economist, I have a bit more sense about the next step, namely what such a price would to the world economy). I would be more than happy to be proven wrong.

On the effects of higher oil prices: The conclusions from our 2009 paper (with Marianna Riggi) https://t.co/4AaN8Jtm8t are going to be tested. (but there is more to the current episode than higher oil prices)

Hoy hemos celebrado una formación para periodistas junto a @APIE_es para analizar cómo la #geopolítica está transformando la #economía y los #mercados.🌍

Kremlin has proposed a wide-ranging economic partnership with Trump administration, including its return to the dollar settlement system. Looking at the Russian seven points provided by @christogrozev, it looks like Russia positions itself for reversed Nixon amid New Cold War.

Siempre llegando allí donde nuestros clientes necesitan tomar decisiones. Puedes suscribir un trial de nuestros servicios de research aquí https://t.co/dTyXIDfD6d

📊El EU‑ETS arranca 2026 en un entorno de mayor volatilidad geo, climática y especulativa. Desde @Afi_Research analizamos: caída de correlación TTF‑EUA, exigencias en aviación y marítimo, factores fundamentales (clima/ generación energética) y posicionamiento táctico futuro.

José Manuel Amor, socio director de @Afi_es: "El mercado no es que ignore los riesgos políticos, pero los trata de forma excepcional. El error del mercado es valorar todo de forma cortoplacista porque lee mal la prima de riesgos política"

Cuando el precio del riesgo se ajusta tarde, suele hacerlo de forma abrupta. Mi último artículo en @el_pais con mi compañero Raúl Viñas 👉 https://t.co/kbQzE0yHZc

El inicio del 2026 viene marcado por una aceleración, a momentos caótica, en la geopolítica global. La implementación de la doctrina “Donroe” de la Estrategia de Seguridad Nacional de EE. UU. no se ha hecho esperar. La inestabilidad doméstica en Irán como guinda. Y sólo es 9/1.

👇 Algunos de los vectores clave que están configurando el escenario geopolítico actual.

El orden global se reescribe: las normas se diluyen, se cruzan umbrales antes impensables y la ambigüedad pesa tanto como la fuerza. No hay nuevo equilibrio, sino su fabricación.