Founder & CEO | CIO @gullbridge Innovation-obsessed. Improve lives through transformative financial and infrastructure solutions. | Not Financial Advice

@unusual_whales The concentration and momentum absolutely resemble late-90s behavior, but today’s leaders also generate enormous cash flow. That makes this look more like valuation excess than pure speculation.

@KobeissiLetter The concentration is real. When a handful of mega-cap names drive most index gains, markets can look stronger on the surface than underlying breadth actually suggests.

Rising asset prices themselves are easing financial conditions, which then fuels more inflows into the same winners. That loop can extend trends far beyond what fundamentals alone justify.

We truly are witnessing history right now.

It's clear that the period we are in now will be referenced for decades to come.

The S&P 500 has added +$10 trillion in 29 days, semiconductor, AI stocks are surging 100%+ in weeks, and the Trump Administration is up +550% on Intel.

When we began emphasizing the need to own assets to win in this market over 12 months ago, this is exactly what we meant.

While inflation is back and the labor market has weakened, it simply does not matter right now.

In fact, the return of inflation has only intensified the scramble for yield and hard assets that can preserve purchasing power.

Look at the data: just 5 stocks have accounted for ~50% of the S&P 500’s total gains since April 1st.

These same tech giants driving the market higher are gaining even more momentum amid rate cuts, deregulation, and historic inflows into equities.

Asset owners are experiencing one of the greatest wealth expansions in modern history while everyone else is being left behind.

Our 12+ month thesis has materialized.

@NoLimitGains If this drop holds, watch inflation expectations, energy equities, and the dollar, they’ll confirm whether this was just a spike or a broader macro shift.

@KobeissiLetter If this sustains, watch inflation breakevens, airline stocks, and bond yields, they usually react before broader equities fully price the shock.

@KobeissiLetter A move like this is classic risk premium repricing. You don’t need full disruption, just credible threat to Hormuz flows is enough for oil to spike aggressively.

People love to judge trades by how they end up. Cute. As if the outcome isn’t just the sloppy aftermath of the process. Before $BRAI was even a position, it was a diagnosis. A freshly listed name in full-blown price discovery, no real structure underneath it, just pure chaos wearing a suit.

In those setups, price doesn’t walk, it sprints like it’s late for therapy. It overshoots, it gets delusional, it prices in fantasies that balanced money would never touch. So you stop pretending you can call direction. That’s for amateurs with Bloomberg terminals and hope in their hearts. You start measuring stability instead. How long before this thing starts smelling like bullshit?

The moment the market stops behaving like a market and starts twitching, the odds of a hard reversion go through the roof.

The trade? Just the polite way of saying: “I see what this is.”

Long term, you don’t get consistent by hunting more setups. You get consistent by being less wrong about the conditions. Everything else is just noise and ego.

Our CIO breaks down the $BRAI trade, from price expansion to structural exhaustion. Markets don't fail randomly, they become unstable first. Understanding that shift is the edge.

Read the full note; https://t.co/8jzKhatIGW

The opportunity wasn’t in some naive little prediction about direction. That’s for the retail crowd with their charts and hopium.

No. It was in spotting the instability before it became obvious.

When price pushed beyond the structural support, that’s when you knew the game had shifted. Continuation no longer depended on real strength. It was suddenly about weaker participants piling in, hoping they weren’t the last ones left holding.

At that point, momentum is irrelevant. It’s all liquidity. Pure liquidity.

Read more; https://t.co/qPji0LA7Q0

@KobeissiLetter Government debt and AI-driven corporate borrowing have very different risk profiles. Productive capex debt behaves differently than consumption-driven debt.

The absolute number is massive, but markets care more about interest burden relative to GDP. Debt becomes destabilizing when growth slows and refinancing costs rise simultaneously.

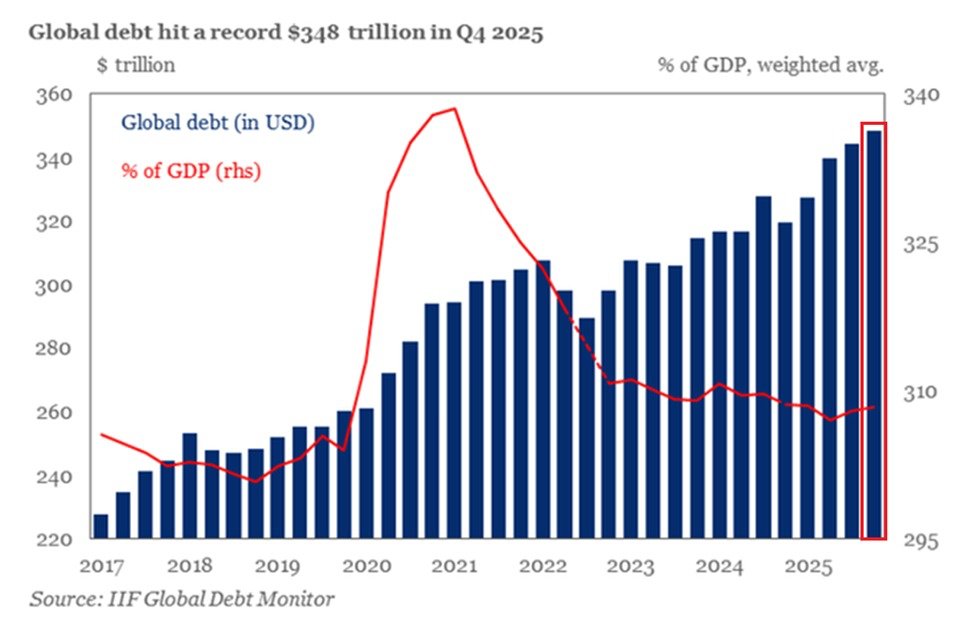

BREAKING: Global debt surged +$29 trillion in 2025, to a record $348 trillion.

This marks the biggest annual increase since the 2020 pandemic.

The surge was particularly driven by governments, which added +$10 trillion, with the US, China, and the Euro Area responsible for roughly three-quarters of the increase.

This brings the global government debt to $107 trillion, an all-time high.

Furthermore, non-financial corporate debt rose to a record $101 trillion, with AI-related investment a major driver of corporate borrowing.

Meanwhile, the total debt of emerging markets rose to a record $117 trillion, with a Debt-to-GDP ratio of 235%, also an all-time high.

The global debt crisis is reaching unprecedented levels.

If this thesis plays out, watch T-bill yields, reverse repo balances, and dollar liquidity metrics, those would reflect stablecoin-driven Treasury demand before broader bond markets react.

Standard Chartered forecasts the stablecoin market could expand from $304 billion today to $2 trillion by 2028, increasing demand for U.S. Treasury bills.