CWD LTD: THE QUIET SOUNDBOX STORY THAT JUST GREW ITS TOPLINE 4.5 TIMES

A microcap that most investors scrolled past two years ago has just closed FY26 with around Rs 147 crore in revenue, up from Rs 33 crore the year before. Here is what is actually happening underneath that number, including the parts that deserve a harder look.

WHAT CWD ACTUALLY DOES

CWD stands for Connected Wireless Devices. It is an Information and Communication Technology company that designs, develops, manufactures and sells integrated solutions combining software and electronics, built almost entirely around wireless connectivity. Its technology spans short range (NFC, Bluetooth BLE, WiFi, Zigbee), mid range (LoRa) and long range systems (4G and 5G, NB-IoT, LTE Cat-M1).

In practical terms, the business runs on three engines today.

1. Soundbox (Fintech). UPI payment soundboxes for India’s digital payment rails. This is the primary growth engine, and CWD has positioned itself as one of India’s larger “Made in India” soundbox manufacturers, including a Rs 76 crore UPI soundbox order announced earlier.

1. CNIC (Smart Meter Communication). Communication modules tied to India’s national smart metering rollout, a long runway and policy driven theme.

1. WMS and bespoke IoT. Enterprise deployments and custom IoT solutions across agriculture, healthcare, logistics and manufacturing.

A fourth vertical, walkie-talkies and smart communication devices, is being readied and is not yet included in the company’s forward guidance.

FY25: revenue Rs 33 crore, EBITDA close to Rs 7 crore, PAT Rs 2.5 crore.

FY26: revenue of around Rs 147 to 151 crore, EBITDA of Rs 28 crore, adjusted PAT of around Rs 12 crore.

That works out to roughly 4.5 times revenue, about 4 times EBITDA and about 4 times profit in a single year. The ramp was back-ended: 9M FY26 stood at Rs 81 crore, with Q3 alone contributing close to Rs 41 crore.

The enabler was capacity. CWD commissioned a new integrated facility, operational from 1 January 2026, that lifted manufacturing floorspace from about 15,000 to about 55,000 square feet, a 3.7 times jump, taking soundbox capacity to as much as 15,000 units a day.

The order book stands above Rs 200 crore, which management frames as 12 to 18 months of revenue visibility.

FY27 guidance (management): revenue of Rs 380 to 400 crore, EBITDA of Rs 72 to 80 crore, and adjusted PAT of Rs 38 to 44 crore. Notably, this guidance excludes the new walkie-talkie vertical.

THE PART THE HEADLINE NUMBER HIDES

Hyper-growth from a small base always deserves a balance sheet check, and CWD’s tells a more nuanced story.

Working capital is heavy. As of FY25, debtor days were around 190, inventory days around 566, and the cash conversion cycle around 378 days. Scaling a hardware business this quickly consumes cash.

Debt has stepped up sharply. Borrowings rose from roughly Rs 9 crore in March 2025 to roughly Rs 63 crore by September 2025 to fund the ramp and capex. The debt to equity ratio remains modest at about 0.6 times, but the trajectory matters.

Return ratios are still low. FY25 ROE was around 5.8 percent and ROCE around 9.5 percent. Growth has not yet translated into high returns on capital, and this is the metric to watch as the new plant fills up.

Promoter holding has fallen from 72.3 percent to about 58.8 percent over the past year through capital raising and a warrant route, worth tracking for alignment and potential future dilution.

CORPORATE ACTIONS YOU SHOULD KNOW

A 4:1 bonus issue took effect on 2 January 2026 (record date). So if you are comparing charts, the roughly Rs 1,900 level of December 2025 and the roughly Rs 300 level of mid-2026 represent the same company. Adjust for the bonus before reading too much into the price move.

Shareholders approved migration from BSE’s SME and Startups platform to the main boards of both BSE and NSE, a meaningful step up in visibility and in eligibility for a broader investor base.

#shreerefrigerations#aeroflex#KRNheatexchanger

The Indian DC Cooling Supercycle: 3 Stocks, 3 Strategies — Pick Your Risk/Reward

India's AI infrastructure buildout is creating a thermal management supercycle. Three companies are positioned to capture it — but they play completely different games. Know which one fits your portfolio. 🧵

1/ Shree Refrigerations — Deep Value hiding behind a Defense Moat

Most are chasing Aeroflex. The real alpha is hiding in plain sight.

Modality: Central bulk water-chilling engines — the baseline cooling every data center needs. Cloud AND AI. Generic solution = wider TAM than any niche play.

Defense is the backstop: Only Indian vendor certified for all 3 naval cooling sub-systems. 3-5 year shipyard validation. ~80% naval HVAC market share. Unreplicable.

DC is the upside: Smardt MagLev oil-free tech cuts PUE by 20-50%. 70,000 sq ft Karad plant moves to localised manufacturing post-FY28. Trezor subsidiary stacking sticky multi-year AMC contracts quietly.

Numbers: ₹154 Cr → ₹1,000 Cr by FY31 (45%+ CAGR). PEG 0.34. ROIC 22-25% vs 12% WACC.

✅ Defense monopoly as permanent backstop | Cloud + AI TAM = largest of the three | AMC recurring revenue compounding | Q4 FY26 net margin hit 19.3% on operating leverage

⚠️ Doesn't own Smardt IP — exclusivity risk | ~370 day cash cycle | DC revenues back-loaded to FY28

Verdict: Defense moat + oil-free tech + AMC stickiness + 0.34 PEG. DC exposure with structural armor underneath.

2/ Aeroflex — Pure-Play AI Infrastructure with Owned Technology

Modality: Liquid Cooling Skids and Secondary Fluid Networks routing coolant directly to GPU chips at >500W. Air cooling fails here. Liquid is the only answer.

IP is 100% owned. No licensing. No royalty drag. 30 years of proprietary SS corrugation process trade secrets.

Switching cost is existential — one coolant leak destroys millions in active GPU arrays. Clients cannot afford to switch.

Capacity: 2,000 → 15,000 skids/year. Frame deal with $50B+ US tech corp signed. TAM: $3B → $21B by 2030 at 33% CAGR.

Numbers: 63% EPS CAGR to FY28. EBITDA targeting 24.5%. Debt-free. 60-day debtor cycle. FY28 P/E at 36.63x.

✅ 100% owned IP — zero partner risk | Near-infinite switching costs near GPU arrays | Only Indian hyperscaler-certified SS liquid cooling skid maker | Cleanest balance sheet of the three

⚠️ 60% international revenues = tariff exposure | Pure AI CapEx play — order pipeline mirrors hyperscaler spend | 36.63x FY28 P/E leaves zero execution room

Verdict: Owned IP. Existential switching costs. $21B TAM. 63% EPS CAGR. Purest AI infra play in India.

3/ KRN Heat Exchangers — The Volume Machine Riding the OEM Wave

Modality: Fin & tube coils built to OEM print. Daikin designs the chiller — KRN stamps the coil inside it. Industrially. At scale.

No proprietary tech needed. No direct hyperscaler relationship needed. DC buildout fills OEM books — KRN rides the wave automatically.

Scale is the story: ₹1,000 Cr Rajasthan facility targeting 50% of Indian hyperscale DC coil demand. 6x capacity. Only 20% utilized today — operating leverage ahead is enormous. Fully backward integrated. Cost pass-through shields margins.

Numbers: ₹430 Cr → ₹1,350 Cr by FY28. 69% EPS CAGR. PEG 0.50. 17% concessional tax rate.

✅ 69% EPS CAGR at 0.50 PEG — cheapest earnings growth of the three | 6x plant at 20% utilization = massive leverage ahead | China-plus-one pulling OEM sourcing to India

⚠️ Daikin = 33% of revenue — one relationship defines the thesis | Narrow moat — replicable with capital | Builds to client print — EBITDA structurally capped ~19.5% | OCF negative during growth phase

Verdict: Not a moat buy. A capacity cycle buy. Maximum operating leverage at the lowest valuation.

[Not investment advice, DYOR]

RIR Power Con Call - A must-read, see how the company is struggling to get 33 kV power, this is how we want to compete with China.

We are definitely the world leader in red tapism.

Remember – RIR Power's upcoming unit to be set up in Orissa is India's first SiC based semiconductor unit, the government is providing incentives to this project, you can imagine the level of bureaucratic hurdles for a normal business.

A ₹77 crore business. Sold for ₹2,000 crore. To a buyer who owned ₹0.04 crore of assets.

- That single deal added ₹1,923 crore of profit to Suzlon's books.

- On 29 May 2026, SEBI ruled that the profit was never real…

Let’s understand how related-party transactions and accounting loopholes can be exploited to artificially "dress up" standalone financial statements...

1/

Nikhil Kamath bought 4.9% of Nazara Tech on 15th May at ₹266 for ₹486 Cr. Thankfully, it appears Co will not be affected by SC ruling on GST because it is not into 'Real Money Gaming'. Nazara has cash on hand & may benefit from the exit of the others & increase its market share

making profit of 1cr from 1 stock

making profit of 10cr from 1 stock

making 5 year salary in 60 days

everything is possible in stock market

Think BIG

First is mindset change

next is bank balance

Respected @nsitharaman ji and @FinMinIndia ,

Suggestion 1 of 3 for strengthening India's capital markets:

Long-term capital gains tax on listed equities should be abolished.

A long-term shareholder is not a speculator but a provider of patient risk capital. By investing in and holding businesses, investors help companies expand, create jobs, innovate and contribute to India's economic growth.

India requires enormous amounts of long-term capital to build world class enterprises, infrastructure and global champions. Tax policy should encourage households to move savings from passive assets, including imported stores of value such as gold, into productive businesses that create jobs, generate tax revenues and build national wealth.

The appreciation in a company's value is not created in isolation. During its growth journey, the government already collects corporate tax, GST, income tax from employees, customs duties, stamp duties and numerous other levies. Long-term capital gains are often the final outcome of economic activity that has already generated substantial tax revenues.

Most importantly, tax policy should clearly distinguish between investment and speculation. A long term shareholder is a partner in wealth creation, not merely a participant in market transactions. Tax policy should reward long-term ownership of productive businesses and distinguish it from short-term speculation.

India needs more patient capital, more entrepreneurship and more long term investing. Abolishing long-term capital gains tax on listed equities would be a powerful step in that direction.

Respectfully submitted.

Good #Q4FY26-26/5/26 till 1pm

SRM contractors

Astra Microwave Products

Refex Industries

SRM contractors

#SRM#SRMContractors

Solid Q4FY26 and FY26

Highest ever revenue, EBITDA, PBT and PAT in comps history

Good QoQ and YoY uptick across all parameters

Rev at 445cr vs 227cr

Q3 at 231cr

PBT at 70cr vs 33cr

Q3 at 37cr

PAT at 54cr vs 24cr

Q3 at 24cr

FY26 Rev at 1025cr vs 528cr

PBT at 151cr vs 74cr

FY26 PAT at 111cr vs 55cr

OCF at 92cr vs -47cr

Astra microvave Products

#AstraMicro

Solid Q4FY26

Highest ever set

Good QoQ and YoY uptick across all parameters

Rev at 488cr vs 407cr

Q3 at 260cr

PBT at 143cr vs 100cr

Q3 at 61cr

PAT at 106cr vs 73cr

Q3 at 47cr

OCF at 386cr vs -90cr

#Refex

Solid Q4FY26

Good QoQ and YoY uptick across all parameters

Rev at 934cr vs 594cr, Q3 at 576cr

PBT at 148cr vs 68cr, Q3 at 81cr

PAT at 94cr vs 48cr, Q3 at 53cr

Big jump

I went through 75+ concalls so you wouldn't have to.

The full FY27 guidance map across 15 Indian sectors.

Renewables & Clean Energy

🔹Premier Energies: 3 to 4x revenue growth over 3 years

🔹Inox Wind: 1,500 to 2,000 MW annual execution in FY27 to FY28

🔹Sarda Energy & Minerals: 20%+ growth over 3 years

🔹Waaree Renewable Tech: 30 to 40% growth

🔹Suzlon Energy: 4,000+ MW order book

🔹JSW Energy: targeting 20 GW by 2030

🔹Waaree Energies: targeting 20+ GW

Data Centers

🔹KRN Heat Exchanger: 60% growth in FY27

🔹Aeroflex Industries: 35% growth in FY27

🔹Netweb Technologies: 35 to 40% revenue growth, 13 to 14% EBITDA margin over next 2 years

Pharma & Healthcare

🔹Poly Medicure: 25% revenue growth, ₹2,300 to 2,400 Cr in FY27

🔹Senores Pharma: 50 to 60% PAT growth in FY27

🔹Sai Life Sciences: 15 to 20% revenue growth in FY27

🔹Cupid: 70% PAT growth in FY27

🔹Beta Drugs: 20 to 25% revenue growth in FY27

🔹Kwality Pharma: 50% PAT growth in FY27

Power Transformers

🔹Transformers and Rectifiers India: 40%+ growth over 3 years

🔹Danish Power: 20 to 25% growth over 3 years

🔹Supreme Power Equipment: 50% growth over 2 years

🔹Hitachi Energy India: strong multi-year HVDC and grid modernisation opportunity

🔹Atlanta Electricals: 40% growth over 2 years

🔹Shilchar Technologies: 20%+ growth over 2 to 3 years

🔹TD Power Systems: 30% growth in FY27

EMS & Electronics

🔹Aimtron Electronics: 40 to 50% revenue growth in FY27

🔹Netweb Technologies: 30 to 35% growth in FY27

🔹Rashi Peripherals: 20% revenue growth in FY27

🔹Avalon Technologies: 24 to 27% growth in FY27

🔹Kaynes Technology: strong multi-year growth opportunity

🔹GNG Electronics: 25% revenue growth in FY27

🔹E2E Networks: hyper growth phase, no specific guidance

Power Capital Goods

🔹Yash Highvoltage: 50 to 70% in FY27, 40 to 42% CAGR over 4 to 5 years

🔹Quality Power Electrical Equipments: 15 to 20% in FY27, 50% in FY28

🔹Genus Power Infrastructures: 33%+ growth in FY27

🔹Apar Industries: 15 to 20% CAGR over 3 to 5 years

🔹Synergy Green Industries: 33% revenue growth in FY27

🔹Skipper: 30% PAT growth in FY27

Defence

🔹Data Patterns India: 20 to 25% revenue growth, order book ~₹1,868 Cr

🔹Krishna Defence and Allied: 30 to 40% growth over next few years

🔹Solar Industries: 42% revenue growth in FY27

🔹Zen Technologies: 50%+ growth over 2 years

🔹MTAR Technologies: 80% ±5% growth in FY27

Recycling & Waste Management

🔹Gravita India: 35% revenue growth in FY27

🔹Namo eWaste: 40 to 50% growth

🔹Tinna Rubber: 25%+ growth

🔹Baheti Recycling: 30 to 35% growth

🔹Antony Waste: 20%+ growth

🔹Sunlite Recycling: 20%+ growth

Cables, Wires & Pipes

🔹Man Industries: 40 to 55% revenue growth, ₹5,000 to 5,500 Cr in FY27

🔹RR Kabel: 16 to 18% volume growth in FY27

🔹KEI Industries: 20%+ growth in FY27 and over 3 to 5 years

🔹HFCL: 20 to 25% growth in FY27

🔹Welspun Corp: 20% revenue growth, ₹20,000 Cr in FY27

🔹V-Marc India: 40%+ growth in FY27 and over 2 to 3 years

FMCG & Consumption

🔹ADF Foods: 35 to 50% revenue growth, ₹925 to 1,000 Cr in FY27

🔹Bazaar Style Retail: 25% revenue growth in FY27

🔹Hindustan Foods: 35 to 50% PAT growth, ₹200 to 220 Cr PAT in FY27

Aerospace

🔹Rossell Techsys: 80 to 90% revenue growth in FY27

🔹PTC Industries: long-term aerospace and defence alloy growth opportunity

🔹Azad Engineering: 25 to 30% growth over next few years

Finance & Digital Platforms

🔹Pine Labs: 21 to 23.5% revenue growth in FY27

🔹Anand Rathi Wealth: 25% growth

🔹Northern Arc Capital: 22 to 25% growth

Chemicals & Specialty

🔹Acutaas Chemicals: 25% growth in FY27 and over 3 years

🔹Neogen Chemicals: 40%+ growth over 3 to 4 years

🔹Pondy Oxides and Chemicals: 20%+ growth over 4 years

🔹Krishana Phoschem: 35 to 40% growth in FY27

🔹Stallion India Fluorochemicals: 30 to 35% growth in FY27

Railways

🔹Ramkrishna Forgings: 80 to 85% capacity utilisation in FY27

🔹Airfloa Rail Technology: 50% growth over 2 years

🔹RITES: 15 to 20% steady growth

🔹Frontier Springs: 30%+ growth over 2 years

Logistics

🔹Shadowfax Technologies: 27 to 30% growth

🔹Zinka Logistics: 30%+ growth

Water Management

🔹Enviro Infra Engineers: 35 to 40% growth

🔹VA Tech Wabag: 20%+ growth

🔖Bookmark it. Earnings season will tell you who delivers and who blinks.

📌Disclaimer: The above data should not be considered as a Buy or Sell recommendation. The analysis has been done for educational and learning purposes only.

Simple logic for sigma advance

#SigmaAdvancedSystemLtd

March Revenue consolidated : 322 Cr

Full year Revenue Projection: 1288Cr

Every defence company is getting 13-15X Sales As Valuation

So Taking 13X of sales

It comes to approx 16500Cr Market Cap

Current Market Cap : 6500 Cr

This is my personal Valuation thesis

No buy/sell recommendations

Sterlite Technologies and the Target Prices

FY27

My base case estimate for FY27 PAT was around ₹400 Cr, and many friends felt I was being too conservative.

Nuvama’s FY27 estimate: ₹551 Cr PAT

CLSA’s FY27 estimate: ₹350 Cr PAT

FY28

The gap becomes even wider for FY28:

Nuvama estimate: ₹912 Cr PAT

CLSA estimate: ₹643 Cr PAT

Interestingly, CLSA assigned a 50x multiple to FY28 earnings, arriving at a target price of ₹655 based on FY28 EPS of ₹13.1.

Now, if one applies the same 50x multiple to Nuvama’s FY28 EPS estimate of ₹18.5, the implied value comes to nearly ₹925!

Perhaps the optimism is influenced by Nuvama being the lead banker for the fund raise, which may explain the more bullish projections.

You figure out which projection you want to take!

These are companies listed on our exchanges with unusually high operating profit margins compared to their sector averages.

That makes them worth studying.

The key is to understand what drives those margins — pricing power, niche products, efficiency, brand strength or superior business mix.

A few may be cyclicals, so ignore them and focus on businesses where high margins are sustainable.

https://t.co/2ATBoLVoGq

Folks latest note on HCG is out , detailed research note on the business , a must read for someone who is interested in the Hospital sector , have gone in detail on the business here with detailed writing with Arvind from @logical_traderr

disc: this is just for research purposes , I do not own shares in this business , no reco

#SIEMENS#ENERGY#INDIA#ENERIN @ 3100

Pureplay Power Company ⚡️

Company Strategy and Operations

SEIL is a pure-play energy company covering the entire value chain through Power Generation (PG) and Power Transmission (PT).

Key verticals include Power Utilities, Metal and Cement, Oil and Gas, Petrochemicals, Data Centers, and Railways.

Local manufacturing is a core strength with 8 factories, 4 Engineering/R&D centers, 6 sales offices, and 4 service centers across India.

The company focuses on low-carbon or zero-emission power generation, specifically gas power and related services, but does not manufacture gas turbines or green hydrogen electrolyzers locally.

SEIL supports global operations through exports of products and engineering services (Local to Global).

Market Outlook and Dynamics

India projects GDP growth of 7.4% for FY26, showing strong resilience despite global geopolitical crises.

Electricity demand is projected to reach 3365 TWh by 2035-36, with total generation capacity hitting 1215 GW (65% non-fossil sources).

Per capita consumption is expected to reach 13,000 kilowatt hours by 2070.

Data centers are a major growth driver, with India's capacity expected to reach 7 to 18 gigawatts.

Growth is further driven by the Green Hydrogen Mission, National Manufacturing Mission, and nuclear energy plans (targeting 100 GW by 2047).

Financial Performance (H1 FY26 vs. H1 FY25)

Total revenue ⬆️ 27% YoY

PAT ⬆️ 52% YoY

Order book ⬆️ 22.2% to 18,430 Crores.

Operating profit margin improved to 20.7% from 19.1%, driven by operating leverage and favorable export mix.

Export contribution ⬆️ 28.5% of total revenue.

Revenue mix consists of Products (37.6%), Solutions (35.5%), and Services (26.9%).

Segment Highlights

Power Transmission:

Revenue rose 29.7% to 2,400 Crores with a 12,520 Crores backlog.

Success was driven by bulk 765 kV transformer orders and GIS products for renewable energy.

Power Generation:

Revenue rose 23.3% to 1,900 Crores with a 5,920 Crores backlog.

Highlights include steady demand from utilities and industry sectors.

Important Projects and Deliveries

Received an order for 13 large 765 kV transformers (500 MVA) for domestic grid expansion.

Winning transformer orders for the US market driven by data center and renewable energy needs.

Refurbished a 210 megawatt turbine in Odisha, highlighting growth in modernisation services for the thermal fleet.

Exporting offshore Gas Insulated Switchgear (GIS) to the Middle East for oil and gas expansion.

Guidance and Future Highlights

Order Intake: No specific numerical forward guidance provided, but a strong 1.5 book-to-bill ratio suggests healthy development.

New CAPEX: Announced 2,060 Crores for a Greenfield Transformer factory (location pending).

Ongoing Expansions: Brownfield investments of 740 Crores at Kalwa and Chhatrapati Sambhajinagar are in progress, expected to come online by mid-2027.

Profitability: Margin improvements are expected to be sustainable through economies of scale and high-value project selection (value over volume).

ESG and Safety

Aiming for climate neutrality in operations by 2030; achieved a reduction of 7,500 tCO2e in H1.

Achieved 15.3% gender diversity and maintained a "Zero Harm" safety record with no fatalities or lost time injuries.

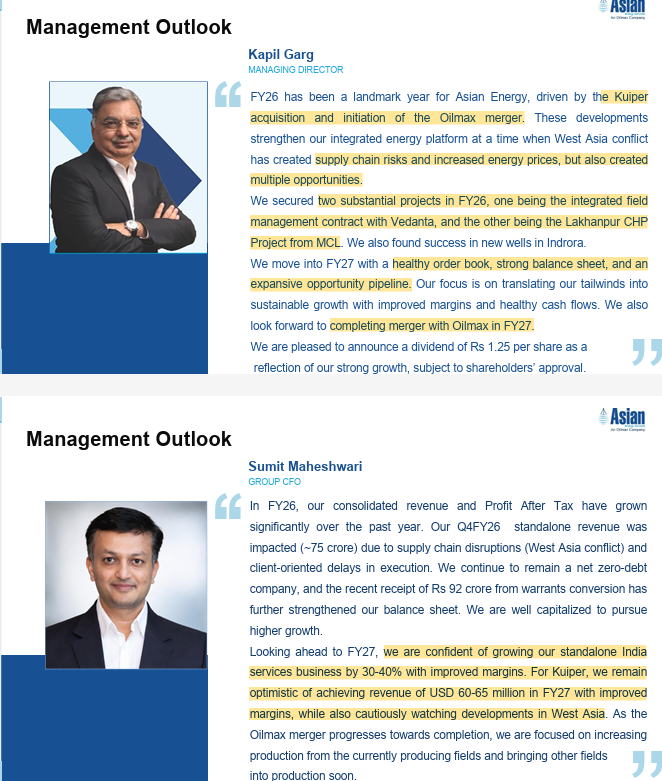

#Asianenergy

Asian Energy Services Ltd

Very strong set of numbers

Revenues are in continuous uptrend and significant jump from 102cr to 338cr

Operating profit jump by 6x in 2 quarters

EBITDA and PAT Margins improved in QoQ but decreased in YoY

PAT from loss of 4crs to profit of 33crores

Operating cashflows turns positive for 53crs

Order Book stands on 31st March 2026 - Rs 1,750 crore

Oilmax Merger Status: expected to be completed by September/October 2026

Significant progress in the Indrora Block, with the NM-01 Well producing ~100 BOPD

Growth: Asian Energy + Kupier group + Oilmax

![ramesh_vd's tweet photo. #shreerefrigerations #aeroflex #KRNheatexchanger

The Indian DC Cooling Supercycle: 3 Stocks, 3 Strategies — Pick Your Risk/Reward

India's AI infrastructure buildout is creating a thermal management supercycle. Three companies are positioned to capture it — but they play completely different games. Know which one fits your portfolio. 🧵

1/ Shree Refrigerations — Deep Value hiding behind a Defense Moat

Most are chasing Aeroflex. The real alpha is hiding in plain sight.

Modality: Central bulk water-chilling engines — the baseline cooling every data center needs. Cloud AND AI. Generic solution = wider TAM than any niche play.

Defense is the backstop: Only Indian vendor certified for all 3 naval cooling sub-systems. 3-5 year shipyard validation. ~80% naval HVAC market share. Unreplicable.

DC is the upside: Smardt MagLev oil-free tech cuts PUE by 20-50%. 70,000 sq ft Karad plant moves to localised manufacturing post-FY28. Trezor subsidiary stacking sticky multi-year AMC contracts quietly.

Numbers: ₹154 Cr → ₹1,000 Cr by FY31 (45%+ CAGR). PEG 0.34. ROIC 22-25% vs 12% WACC.

✅ Defense monopoly as permanent backstop | Cloud + AI TAM = largest of the three | AMC recurring revenue compounding | Q4 FY26 net margin hit 19.3% on operating leverage

⚠️ Doesn't own Smardt IP — exclusivity risk | ~370 day cash cycle | DC revenues back-loaded to FY28

Verdict: Defense moat + oil-free tech + AMC stickiness + 0.34 PEG. DC exposure with structural armor underneath.

2/ Aeroflex — Pure-Play AI Infrastructure with Owned Technology

Modality: Liquid Cooling Skids and Secondary Fluid Networks routing coolant directly to GPU chips at >500W. Air cooling fails here. Liquid is the only answer.

IP is 100% owned. No licensing. No royalty drag. 30 years of proprietary SS corrugation process trade secrets.

Switching cost is existential — one coolant leak destroys millions in active GPU arrays. Clients cannot afford to switch.

Capacity: 2,000 → 15,000 skids/year. Frame deal with $50B+ US tech corp signed. TAM: $3B → $21B by 2030 at 33% CAGR.

Numbers: 63% EPS CAGR to FY28. EBITDA targeting 24.5%. Debt-free. 60-day debtor cycle. FY28 P/E at 36.63x.

✅ 100% owned IP — zero partner risk | Near-infinite switching costs near GPU arrays | Only Indian hyperscaler-certified SS liquid cooling skid maker | Cleanest balance sheet of the three

⚠️ 60% international revenues = tariff exposure | Pure AI CapEx play — order pipeline mirrors hyperscaler spend | 36.63x FY28 P/E leaves zero execution room

Verdict: Owned IP. Existential switching costs. $21B TAM. 63% EPS CAGR. Purest AI infra play in India.

3/ KRN Heat Exchangers — The Volume Machine Riding the OEM Wave

Modality: Fin & tube coils built to OEM print. Daikin designs the chiller — KRN stamps the coil inside it. Industrially. At scale.

No proprietary tech needed. No direct hyperscaler relationship needed. DC buildout fills OEM books — KRN rides the wave automatically.

Scale is the story: ₹1,000 Cr Rajasthan facility targeting 50% of Indian hyperscale DC coil demand. 6x capacity. Only 20% utilized today — operating leverage ahead is enormous. Fully backward integrated. Cost pass-through shields margins.

Numbers: ₹430 Cr → ₹1,350 Cr by FY28. 69% EPS CAGR. PEG 0.50. 17% concessional tax rate.

✅ 69% EPS CAGR at 0.50 PEG — cheapest earnings growth of the three | 6x plant at 20% utilization = massive leverage ahead | China-plus-one pulling OEM sourcing to India

⚠️ Daikin = 33% of revenue — one relationship defines the thesis | Narrow moat — replicable with capital | Builds to client print — EBITDA structurally capped ~19.5% | OCF negative during growth phase

Verdict: Not a moat buy. A capacity cycle buy. Maximum operating leverage at the lowest valuation.

[Not investment advice, DYOR]](https://pbs.twimg.com/media/HKRLCHKbsAAVSdU.png)