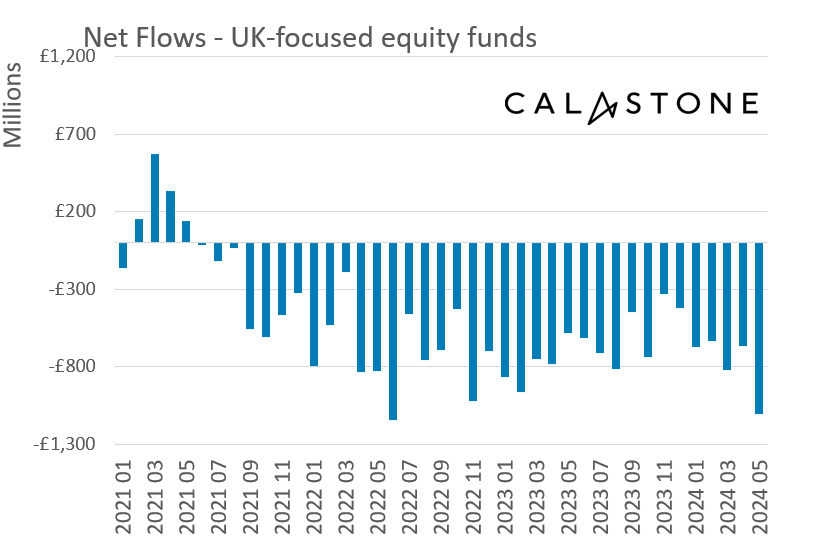

Calastone fund flows data shows continued net outflows from UK-focused equity funds

Profit taking after the recent UK market rally prompted a £1.11bn outflow from UK-focused funds, the worst net selling from this sector since June 2022

ECB expected to cut rates today. The graph below shows how rate expectations have been delayed and reined in over time, with rates set to remain higher for longer

May's Barclaycard consumer spending data also indicates a fall in margins in Travel as consumers appear to be trading down

Travel spend growth was 4.7% YoY in May, outpaced by transaction growth of 6.6%

Barclaycard May consumer spending data shows Hospitality & Leisure spend up 2.7% YoY with transaction growth up 1.6%

Perhaps the most alarming trend is the continued fall in restaurant spending, down 15.7% YoY in May, 13.1% in April and 12.6% in March

#RBG: Spurns NGHT approach. Says it 'has concluded that the Nightcap Proposal is incapable of being delivered.' The proposal was 'subject to multiple equity fundraisings by Nightcap' and would need 'the support of the Company's and Nightcap's respective lenders.'

BRC-NielsenIQ data shows Shop Price annual inflation eased to 0.6% in May, down from 0.8% in April

Non-Food remained in deflation at -0.8%

Food inflation decelerated to +3.2%, but remains stickier

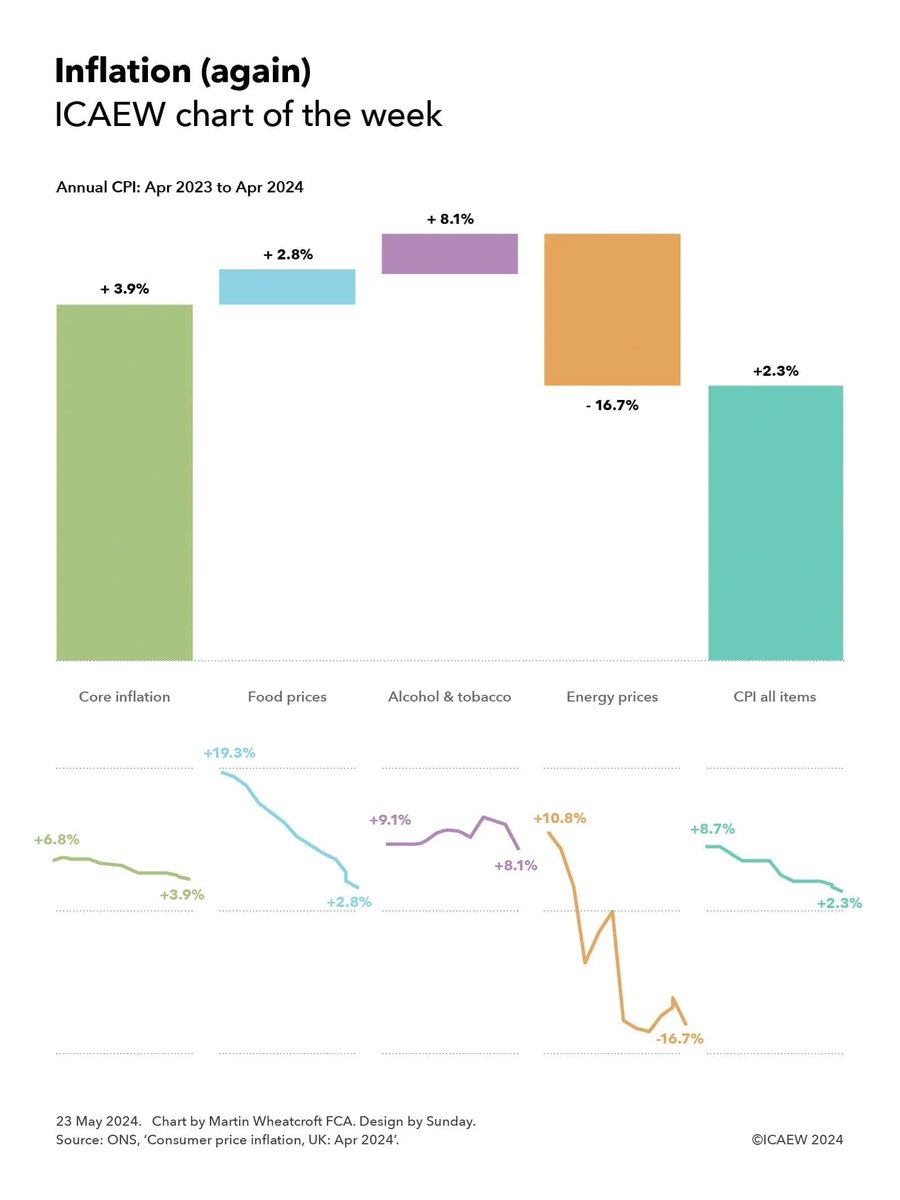

ICAEW's chart below illustrates how a 16.7% fall in energy prices between April 2023 & April 2024, have partially offset core inflation of 3.9%, food price rises of 2.8% and alcohol & tobacco prices rises of 8.1%, to result in annual CPI of 2.3%

Inflation hasn't fully gone away

UK Flash PMI comes in at 52.8 in May, down from 54.1 in April

UK businesses reported the softest increase in average selling prices for over three years in May and ongoing hiring challenges meant that the rate of job creation remained only marginal

Keyword Studios $KWS possible cash offer of 2,550p per share is good news for the UK listed games developer segment, Frontier Developments $FDEV +7.5% in reaction

The offer for KWS is x3 revenue, currently FDEV is being valued by the market at x1 revenue...

Ryanair's $RYA comments indicate that demand may be faltering slightly YoY for summer 24, resulting in more 'price stimulation'

This is contrary to Barclaycard data showing resilient spend on holidays

Ryanair $RYA comments on summer 2024 outlook: "demand is positive, with bookings trending ahead of last year. Recent pricing is softer than we expected, with Q1 requiring more price stimulation than last year...outcome will be heavily dependent on close-in peak S.24 pricing"

Big week for US Fed interest rate decision making coming up

Mon - New York Federal Reserve's monthly survey of consumers’ inflation expectations

Tues - Labor Department’s report on producer prices

Wed - US CPI reading (3.4% expected in April, down from 3.5% in March)

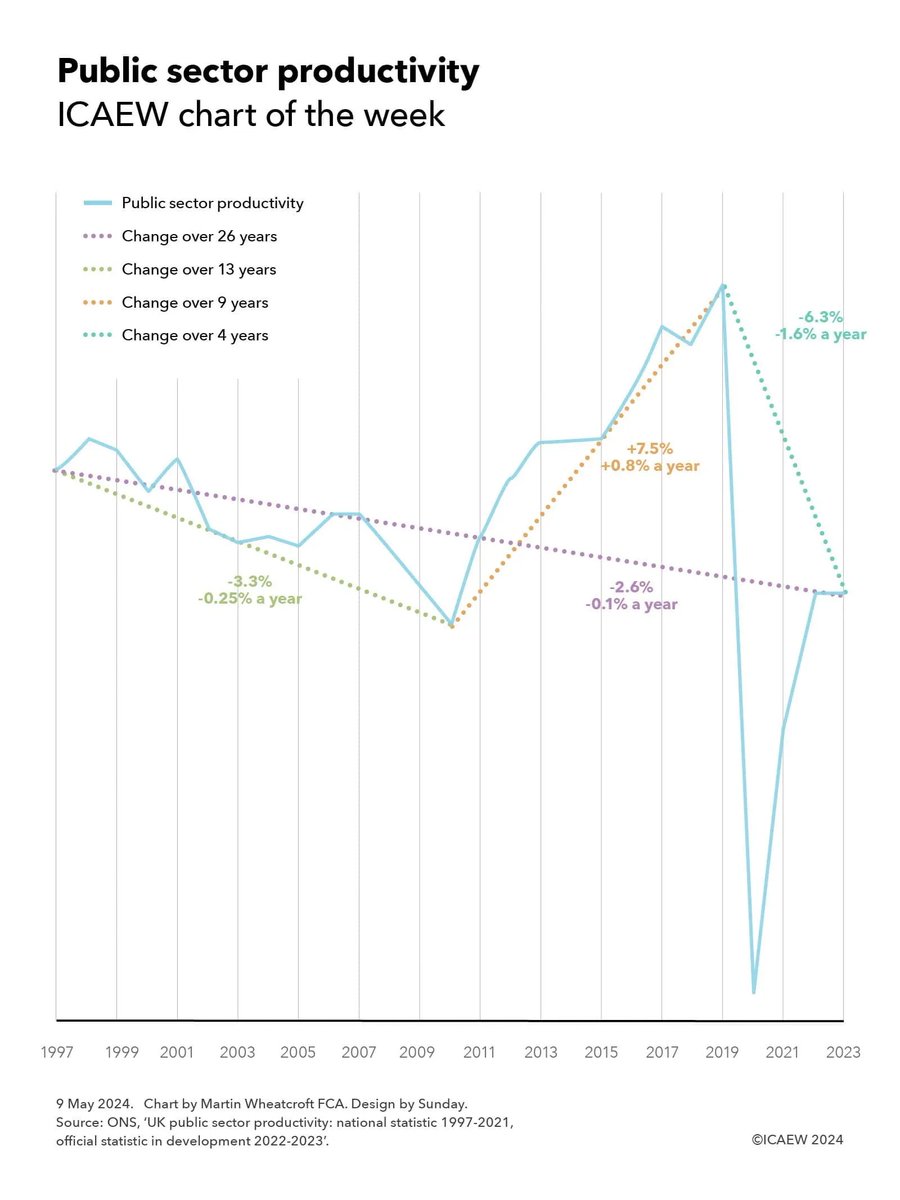

Interesting chart from the @ICAEW this week showing the long-term productivity decline in the public sector

A lot of the gains made in the last decade were wiped out by the pandemic, when many public services were closed or curtailed

Recent restructuring proposals from Tasty $TAST & Revolution Bars $RBG appear to be CVAs in all but name

'Non-critical' creditors (somewhat insulting term) have been disadvantaged on purpose

Likely to impact the terms offered by suppliers, both critical & otherwise, going fwd

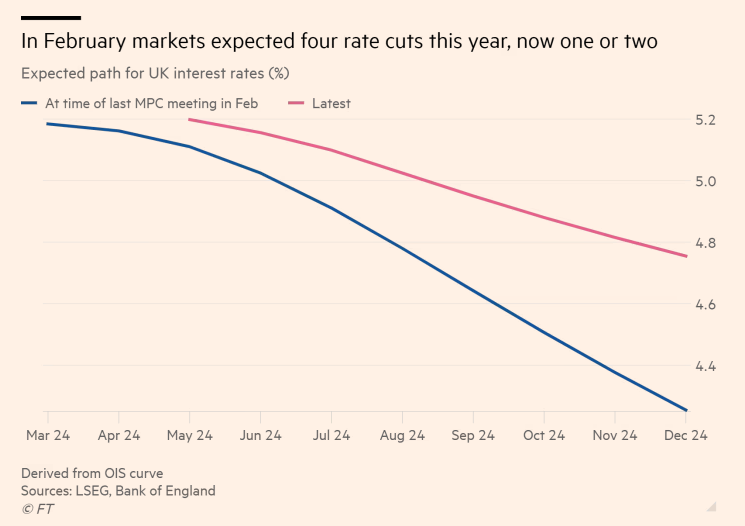

Data from US Commodity Futures Trading Commission shows traders are increasingly betting that £GBP will fall in the coming months amid growing conviction that Bank of England will cut interest rates before US

Chart from FT below indicates BoE to start cutting rates in the summer

Calastone Fund Flow Index shows a booming ISA season, with inflows to equity funds 5x larger than 2023 at £1.93bn

Bad news for London though - Global, North America & European funds are in favour, while Emerging Markets and UK are out #investing#equities#stockmarkets

JD Wetherspoon $JDW shares +3% on its Q3 update, will be hoping for better weather in its summer Q4 to boost sales, cost inflation abating, better visibility regarding labour pressures post NLW increase

#JDW Q3 Conf Call. Calendar 2024. Jan & Feb poor, next 2 months steady. Weather unhelpful. Underlying LfL (adj. for fall of Bank Hols) c5.5% to 6%. Says no plans for further large disposals. Hotels lapping tough comps. Growth slower than last year but will open more.

UK Hotels: Travelodge (y/e Dec 23) & Whitbread $WTB

(y/e Feb 24) reported FY numbers

Both saw profit significantly up YoY, driven by increase in room rates

Hotel performance is cyclical, with WTB signalling a tougher Q1 it might be that we've already seen the top of a cycle...