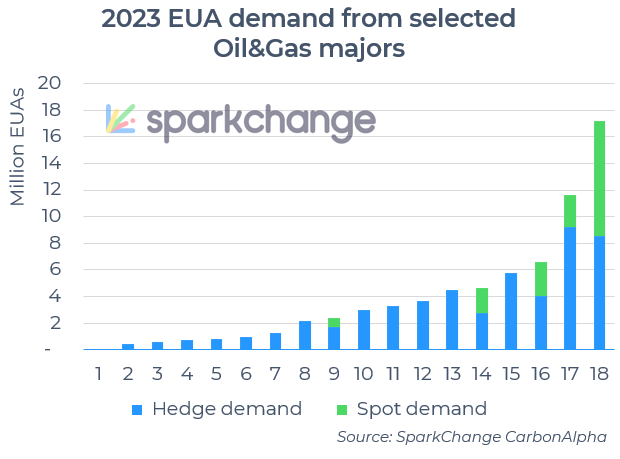

@SparkChangeCo2 data shows that most Oil&Gas majors are hedging their EUA demand, and just selectively complement this with spot purchases.

Find out more here: https://t.co/NknFtyiDNJ

(5/5)

Two truths and a lie:

1) Polish #power emissions are down ~15% against 2022

2) Polish refinery throughput is down 6% Year on Year

3) 2023 #EUA demand from Polish energy companies is down accordingly

A thread (1/5)

#OCTT#carbon#ORLEN2Q23#EUETS#carbonmarkets#ESG

Understanding how corporates manage their carbon allowance price exposure is critical to

👉 assess true EUA demand

👉 understand the competitive positioning against its peers. (4/5)

NABE – the biggest #EUA buyer you never heard of!

Something is rotten in the State of Poland: Being a laggard in decarbonisation for quite a while, the Polish government is now effectively forming a “bad bank” for emissions intensive assets.

(1/7)

https://t.co/78YAaNTC0t

💲 Furthermore, the positive impact on the four utilities is striking: @SparkChangeCo2 data shows that the utilities would have faced an EUA bill of €8.6 bn in 2024. A 1€/tonne uptick in carbon prices would have on average impacted the EBITDA by 7%.

(6/7)

At @SparkChangeCo2, we track more than 9,000 corporates globally on how they are exposed to carbon pricing. Emissions and free allocation in each carbon market like the #EUETS, #WCI, #RGGI and more, and how these companies purchase EUAs. Get in touch to learn more! (7/7)

‼️ Conclusion: Going forward, the utility hedge will reduce excess EUA demand. On the other side, the MSR reduced the available “excess” EUAs. But watch out: As industry receives less free allocation, they will start hedging EUAs, leading to increased excess EUA demand (6/7)