Built Aurum because I was tired of giving banks to every finance app.

Privacy-first dashboard:

✅ Net worth tracking

✅ Simple budgeting

✅ No bank logins ever

Your money. Your data. Your clarity.

Try it here 👉 https://t.co/loAHjCkvjs. 🚀

@pmitu They pay for the outcome. The feature is just the vehicle. Stopped adding and started asking “does this get someone out of debt faster”, changes every prioritization decision.

@SkerdiDev Learned this the hard way. Built Aurum for months before seriously thinking about distribution. Product was ready, audience wasn’t. Playing catch-up now and it’s the harder path.

@sflorimm Feels accurate. I’ve spent more time on Product Hunt, HN, and Reddit than I have writing code this month. The product was ready, getting it seen is the actual job.

@JonBuildsHQ Showing up in niche communities where your exact user already hangs out. Not to promote, just to be useful. The trust compounds faster than any ad.

@SaidAitmbarek Most builders treat distribution as a phase 2 problem. By then the product assumptions are already baked in. The fit has to go both directions from the start.

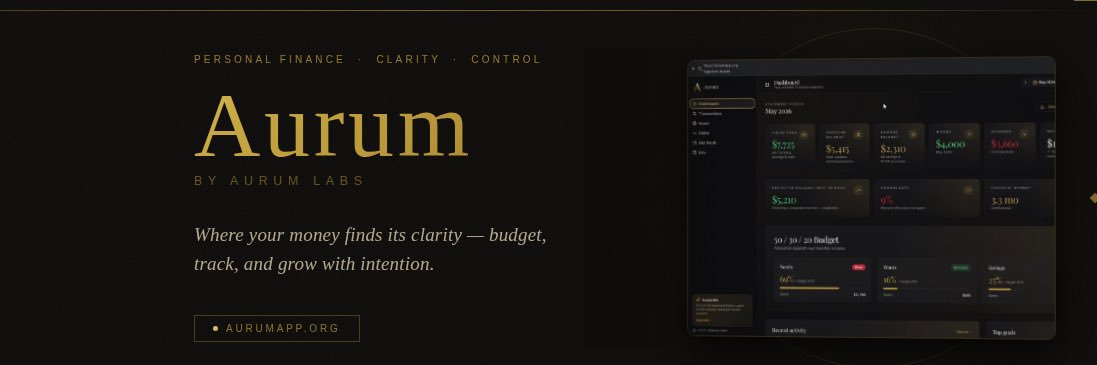

@TanzilaSha9574 Building Aurum, privacy-first personal finance tracking. No bank connections, ever.

Manual logging for debt payoff, bills, goals, and net worth. Built for people who want control over their data, not just their budget.

https://t.co/loAHjCkvjs

Building Aurum, personal finance tracking for people who don’t trust apps with their bank login.

No connections, no data sharing. You manually log what matters: debt payoff, bills, goals, net worth. The people who need it most are privacy-conscious earners tired of Mint/YNAB asking for credentials.

https://t.co/K4qhGqFSBm

Most finance apps ask you to hand over your bank login on day one.

Think about that. You're giving a third party the keys to every account you have, balances, transactions, who you pay, what you earn, and trusting they'll never leak it, sell it, or get breached.

I built Aurum so you never have to make that trade. No bank connection. No login handoff. You enter what you want tracked, and it stays on your terms.

The safest data is the data you never gave away.

Try it here at: https://t.co/7WK21hjwnG

#PersonalFinance #SoloBuilder #SaaS

@Local4News Consistency is the hard part, most apps make tracking feel like a chore, so people quit. Built Aurum specifically to remove the friction. No bank linking, no data sharing, just clean manual tracking that actually respects your privacy. https://t.co/loAHjCkvjs

This is the most honest thing I’ve seen posted about the solo founder experience.

I’m building Aurum on nights and weekends while running operations for a logistics company full-time. Some weeks the momentum feels real. Other weeks you’re staring at a dashboard with 8 users wondering if you’re delusional.

Nobody posts about those weeks. But that’s the actual job.

Still building. 🔨

Your budgeting app knows more about you than your closest friend.

Where you eat. What you drink. Which doctor you see. When your paycheck lands. How much you owe and to whom.

Most of them connect straight to your bank, pull all of it, and sell that picture of your life downstream to data brokers and advertisers. That's not a side effect, it's the business model. "Free" was never free.

I built Aurum the opposite way. It doesn't connect to your bank at all. You decide what it sees. The only person looking at your money is you.

Privacy isn't a feature I bolted on. It's the entire reason the app exists.

#PersonalFinance #FinTech #SideProject

@perkmaybe I'm building the budgeting app that never touches your bank. Most finance apps harvest and sell your transaction data, Aurum can't, by design. Privacy-first, solo-built, early days.

Solid post. This is one of the most common “quiet” wealth killers I see with people who are already making good money.

Lifestyle inflation doesn’t feel like a problem in the moment, it feels like “I’ve earned this.” New car, bigger apartment, nicer vacations, better restaurants, subscription creep… each one seems reasonable on its own. But compound them over a few years and your savings rate stays stuck at 5-10% even as your income doubles.

A few practical ways to fight it:

• The 30-day dollar tracking (as JJ suggested) is gold. Do it once and you’ll usually spot 3-5 “invisible” leaks that add up to hundreds (sometimes thousands) per month.

• Pay yourself first automatically — treat your investing/savings like a non-negotiable bill that hits the day your paycheck lands.

• Set “lifestyle rules” in advance. Examples I give clients:

• Housing ≤ 25% of take-home

• Cars: buy used, keep for 7+ years

• Vacations: cash only (no credit card debt for memories)

• “Want” upgrades: 48-hour wait rule

The goal isn’t to live like a monk. It’s to make sure your lifestyle upgrades are intentional instead of automatic.

If you’re already doing the tracking and want to go deeper (net worth tracking, tax optimization, investment allocation, etc.), feel free to DM me, happy to share the exact systems I use.

What’s one spending area that quietly grew for you after a raise? Curious to hear from others.