Thinking you can just ‘roll over’ your 401(k) into whatever account looks good is one of the fastest ways to accidentally gift the IRS thousands you’ll never see again.

Too many people 50+ are finally ready to simplify their money, only to get slammed with an unexpected tax bill because they moved things the wrong way.

🔕Not all rollovers are created equal. Do it wrong and you could trigger taxes and penalties immediately.

The good news? This is completely avoidable!

Before you touch that old retirement account, do these three things first: Confirm whether you’re doing a direct rollover (safest) or indirect (danger zone).

Make sure the new account is set up for the exact same tax treatment — traditional to traditional, Roth to Roth.

Run the numbers with a CPA or trusted advisor who understands 50+ retirement transitions, not just a random banker.

You’ve worked hard for this money. Don’t let a simple paperwork mistake turn your ‘I’m finally safe’ moment into an expensive surprise. Slow down, get it right, and sleep better knowing your retirement income is protected — not penalized.

Have more questions about moving old retirement accounts into safer strategies? Drop them below. #Retirement #401k #TaxTips #SafeMoney

Growth was great while you were building the portfolio. Now the priority for most $1M+ clients is simple: protect what they’ve built and turn it into reliable income that lasts.

Comment “RISK” for the Retirement Protection Checklist.

Or comment “SUBSTACK” for the full article that just went live.

Safe doesn’t mean small. The right structure can deliver the income you need while removing the worry that keeps so many successful retirees up at night.

Comment “INCOME” and I’ll send you the Will I Run Out of Money? Scorecard.

(And if you want the full deep-dive, comment “SUBSTACK” for today’s article.)

Most $1M+ retirees are still losing sleep over three things nobody warned them about:

• Market risk that can no longer be ignored

• Long-term care costs that can erase even large accounts

• The quiet fear of “Will I actually run out of money?”

I just published the full breakdown on Substack — the exact 4 tools I use with every high-net-worth client to fix them.

Comment “SUBSTACK” and I’ll send you the direct link right away (plus the first two guides free).

Here’s the single most important question every person with $1 million or more should ask their advisor right now:

“If the market dropped 30–40% tomorrow, would my income and lifestyle still be protected?”

Comment “CHECKLIST” and I’ll send you the Retirement Protection Checklist.

You’ve done well. Now you’d like steady income for life, a meaningful tax break, and the ability to support causes you care about — all while protecting your family from a blank check.

Comment “LEGACY” and I’ll send you The Family Legacy Blueprint.

🚨 Wild Retirement Fact: if you make it to 65 there’s a 70% chance you’ll need some type of long term care ….but only about 27% of people think it’ll happen to them.

I’m talking to the 50+ crowd —

Costs for care can easily range from $100k–$300k+

with no help from Medicare.

#longtermcareplanning

#retirementplanning

How much safe, predictable monthly income can a $1M–$3M portfolio actually produce without depending on the stock market?

Most people are surprised by the realistic number once the money is properly structured.

Comment “INCOME” and I’ll send you the Will I Run Out of Money? Scorecard.

Long-term care can destroy even a large retirement account faster than any market crash.

Most $1M+ families think “It won’t happen to us.” The smart ones plan for it.

Comment “CARE” and I’ll send you The Long-Term Care Reality Guide.

“Safe” is often misunderstood as settling for low returns.

For clients with $1M+, the right safe income strategies frequently deliver solid after-tax cash flow and far greater peace of mind than continuing to ride market volatility.

Comment “INCOME” and I’ll send you the Will I Run Out of Money? Scorecard.

Most people with $1 million or more still have a significant portion of their portfolio exposed to market risk. At this stage of life, another major downturn isn’t just uncomfortable — it can permanently change retirement plans.

Comment “RISK” and I’ll send you the Retirement Protection Checklist.

Long-term care can quietly destroy even a large retirement account faster than any market crash.

Most $1M+ families underestimate how expensive it can be — and how long it can last.

Comment “CARE” and I’ll send you The Long-Term Care Reality Guide.

You’ve done well. Now you’d like steady income for life, a meaningful tax break, and the ability to support causes you care about — all while protecting your family from a blank check.

Comment “LEGACY” and I’ll send you The Family Legacy Blueprint.

How much safe, predictable monthly income can a $1M–$3M portfolio actually produce without depending on the stock market?

Most people are surprised by the realistic number once the money is properly structured.

Comment “INCOME” and I’ll send you the Will I Run Out of Money? Scorecard.

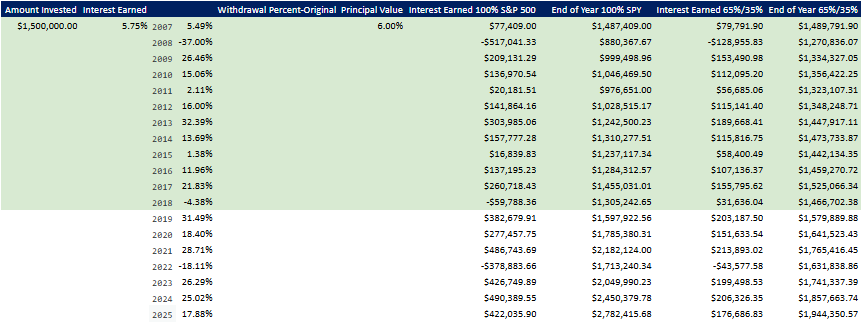

What happens when you retire at the exact wrong time?

Imagine clocking out for the last time in 2007. You have a $1.5 million nest egg and plan to withdraw $90,000 a year to live comfortably.

Then, 2008 happens.

We ran a stress test comparing two different approaches over the last 18 years to see how they survived the Global Financial Crisis and beyond:

1️⃣ An all $SPY allocation (100% S&P 500)

2️⃣ A conservative hybrid allocation (65% Fixed / 35% S&P 500)

📉 The 2008 Reality Check

In year two of your retirement, the market collapses.

If you were 100% invested in the S&P 500, your $1.5M plummeted to $880,000.

You still need your $90k to live, meaning you are forced to liquidate over 10% of your remaining portfolio at the absolute bottom of the market.

If you used the 65/35 hybrid approach?

Your portfolio only dipped to $1.27M. Your fixed income acted as a crucial buffer, protecting your principal from the worst of the crash.

⏳ The Recovery Grind

It took until 2013 for the 100% S&P portfolio to reliably break back above the $1.2M mark.

5 years of stressing over every single withdrawal, over every single daily valuation change.

During that same window, the 65/35 portfolio remained highly stable, hovering between $1.3M and $1.4M.

🏁 The 2025 Reality

Here is what is left today:

• 100% S&P 500: $2.78M

• 65/35 Portfolio: $1.94M

The all-equity portfolio ultimately won the math equation thanks to the historic bull market of the late 2010s.

💡 The Real Lesson

If you were 100% in equities in 2008, watching your life savings get cut in half while still needing to pay bills, would you have stayed invested or would you have panicked, sold at the bottom, and completely derailed your retirement?

The 65/35 portfolio didn't capture all the upside, but it did something more important: It prevented a catastrophic behavioral mistake. It provided the stability needed to sleep at night, weather the storm, and still end up with almost $2 million today.

Check out the attached table to see the exact year-by-year breakdown. 👇

#RetirementPlanning #WealthManagement #SequenceOfReturns #Investing #FinancialAdvice

Most people think ‘Safe’ means settling for low returns.

For those with $1M+, the right retirement income strategies often produce stronger after-tax cash flow and far greater peace of mind than staying fully exposed to market swings.

Comment ‘INCOME’ and I’ll send you the Will I Run Out of Money? Scorecard so you can see how your plan actually stacks up.

Most people with $1 million or more still have a significant portion of their portfolio exposed to the same market risk they carried at 45.

At this stage, another 30–40% drop isn’t just uncomfortable — it can permanently change their lifestyle due to an emotional decision.

Comment “RISK” and I’ll send you the Retirement Protection Checklist so you can see exactly where your plan stands.