(1/5) Imagine a single global account that holds balances in 25+ currencies at once.

Keeta's multi-currency accounts will provide a single wallet where users worldwide can hold multiple fiat currencies simultaneously, fully backed 1:1 with reserves held at regulated banking partners.

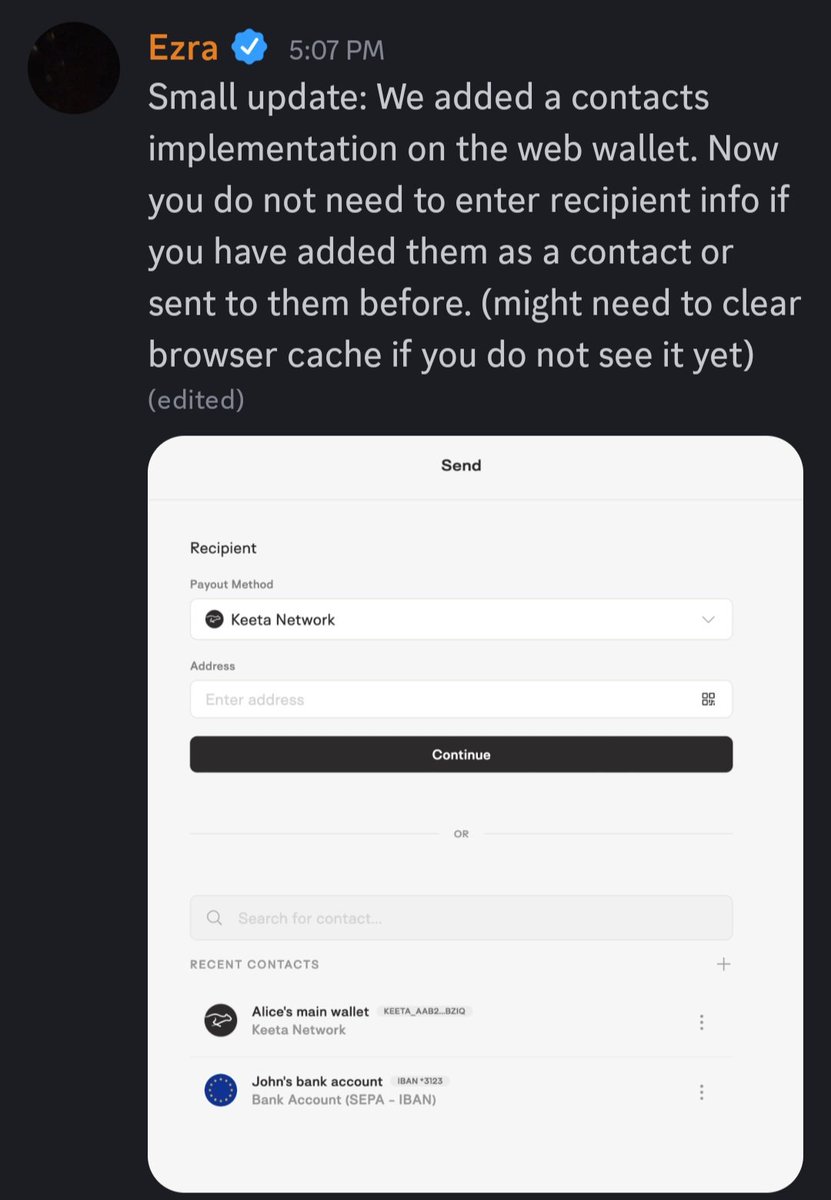

Most people won’t notice this update.

But replacing addresses with contacts is how you go from

“crypto tool” → “real payments app”

This is how adoption actually happens. $KTA

@pmcafrica This is why... ever since I was a teenager, I have wrenched on my own cars 99% of the time. It has saved me tens of thousands and its the primary reason why I can afford owning 4 cars at once.

Now if I could just insure my own cars...

$KTA Keeta is the only network combining:

• instant Visa Direct payouts

• 20+ fiat currencies

• native banking access

• T-Bills & securities

• cards with direct fiat spend

• identity + global rails

All in one system.

Keeta is unifying the entire stack.

@Tesitfy178672 Visa Direct isn’t the story — integration is.

Plenty of apps use Visa… almost none unify crypto, FX, bank rails, and settlement in one system.

And judging tx volume this early misses the point... infrastructure gets built first, adoption follows.

You dont know Fintech do you?

$KTA Keeta isn’t waiting on their bank acquisition — they’re staging it.

Many features in the announcement today looks pre-wired, ready to go live the moment the deal closes.

Bank closes → switch flips → full financial stack activates.

Most fintechs build apps.

$KTA builds the layer apps don’t have to think about.

Banks, chains, FX, on/off-ramps, identity... all abstracted into open rails.

No custody gymnastics, bespoke integrations or closed moats.

It’s financial infrastructure designed like software.

Keeta is the settlement API the internet never had.

$Stripe hid payment rails. $KTA hides all rails — chains, fiat, FX, identity, and institutions — behind one interface.

This is what “money as software” actually means.