Yesterday, we witnessed an incredible trading frenzy at @HMXorg, surpassing anything since our launch! 🤯

Our 24-hour trading volume has soared beyond $100m for the very first time 🚀

Here's to even greater heights, dragons! 🐉

Trade limitless 🔽:

https://t.co/1dQEb91Wbf

Phase 4: Full-Scale Launch is LIVE! 🟢

The following features are now live:

🔹 Trading incentive programs

🔹 Emissions of $TLC, $DP, $esHMX

🔹 Staking of platform tokens

🔹 Trade size & OI limit increased

Trade limitless with HMX 🐉:

https://t.co/nPAAPUCR5g

Yes PayPal’s new centralized $PYUSD stablecoin has centralized admin functions

As does $USDT, $USDC, $USDP, and all other preexisting centralized stablecoins issued by trusted third parties

It’s not really that surprising given the regulatory compliance requirements around handling fiat with consumers

Honestly, I’m surprised they actually went with the traditional stablecoin model (blacklist) versus a more aggressive model (whitelist)

Transfers are permisonless by default for all EOA address and smart contracts (only issuance/redemptions are KYC/AML checked), blacklisting usually reserved for requests by LE and recovering hacked funds

Tokenized assets (like stablecoins) provide many advantages over the status quo of finance (cost, speed, accessibility, programmability, etc), but there does exist trade-offs over ‘pure crypto’

The nice thing about public permissionless blockchains is that users have full transparency over what controls exists and can choose what assets they want to use/hold

$PYUSD legitimizes crypto, Web3, and stablecoins, introducing more liquidity into the ecosystem by providing another trusted on/off-ramp

Still don’t like it? There’s a simple solution, don’t use it

First mover advantage is key in DeFi!

I missed $GMX last year and I regretted it.

I would never miss any promising project that might repay heal that pain.

Well, I found one already!

Let's explore 👇

We're more than excited to announce multiple exciting major developments to HMX (prev. Perp88)

1️⃣ Private round fund raise

2️⃣ Rebranding from to HMX

3️⃣ Launching HMX on Arbitrum

4️⃣ Launching HMX’s governance token

1/14 🧵a thread summarizing the article:

https://t.co/bzosTZPXI7

I picked up $ABR (Arbor Realty Trust) at $10.43 a few days ago.

I believe there is a high likelihood that the market has overreacted to macro-economic news, the short report, and the Houston foreclosure.

I think $ABR could regain 30-50% from here.

🧵...

In case you didn't notice @Level__Finance Treasury went from:

557k $LVL in treasury reserve to 27,3M $LVL 🤯

New $LGO value ~ $1,824,081 👀

The team transferred unused $LVL to Treasury and gave it to DAO management.

Treasury Total Value~$170M

You can redeem funds from Treasury ONLY with $LGO...

What project gives you direct access to a treasury of this magnitude?🤔

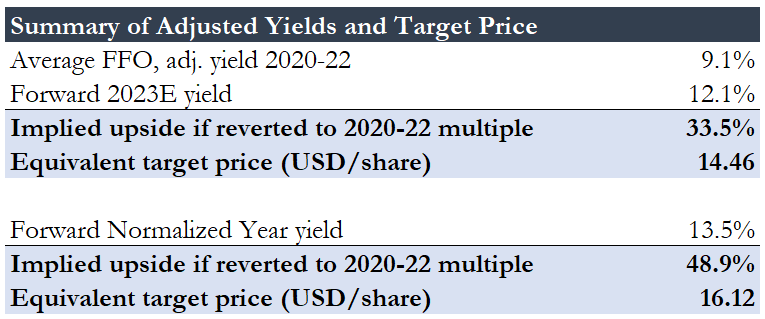

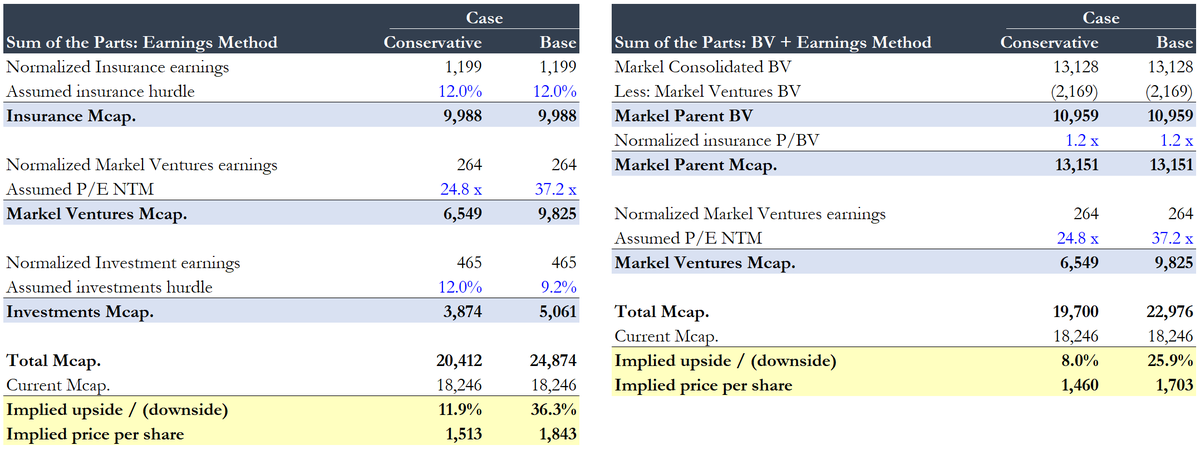

I picked up some $MKL shares last month at $1,326.3/share.

I believe there could be additional $MKL upside of up to 25-30% from the current price based on a SOTP valuation using earnings and BV driven methods.

🧵...

Recently re-read One Up On Wall Street by Peter Lynch.

Peter Lynch was the fund manager of the Magellen Fund at Fidelity between 1977-90. Lynch averaged a 29.2% annual return, consistently more than double the S&P500 index.

Mainly writing this out to keep record for myself.

🧵

$SOFI earnings are out:

- GAAP Net revenue $472M, up 43% YoY

- Adjusted EBITDA $76M, up 772% YoY

- New Members Add 433k, Quarter end total members up 46% to 5.7M

- Total deposits grew by a record $2.7B, up 37% during the quarter to $10B

- Management raises guidance

A wide range of data and commentary indicate that the bank panic is over, bank lending is little impacted, and even bank profitability will be fine. This post reviews the evidence and suggests implied rate cuts based on banking weakness are unwarranted.

https://t.co/x4Q6m8ecJj

20-year-old kids are using AI and No-Code tools to make $10,000/m

They are building money printing machines

Here are 8 AI and No-Code tools to start printing money online:

Just picked up some $BN (Brookfield Corporation) at $32.23 / share.

$BN looks undervalued on a SOTP and FFO/earnings basis.

I estimate $BN is trading with over a 25% holding discount to the underlying assets.

🧵...

Exploring Fashion Styling & Color Assignments in Midjourney v5

A tutorial on how to assign colors to specific articles of clothing, a lesson in using syntax to your advantage.

🧵 Part 5 of an ongoing series

An entire MBA fits on one page.

But you better know the math cold.

Like & comment if you want the excel.

6 topics:

*1) Unit economics*

This builds from product-level unit economics to company financials.

Quantity per unit, growth in units.

Price per unit, growth in pricing.

Cost per unit, marketing spend per unit.

Get you return on ad spend (ROAS), customer acquisition cost (CAC), LTV/CAC, gross margins, unit contribution margins, and more.

This model sets up two diverging products:

A higher gross margin (GM), higher marking cost, low pricing power, low growth product.

Against a lower GM, better pricing power, better growing, lower unit market cost product.

To show how the dynamics of the two play out over time.

*2) Accounting*

Unit drivers flow into revenue, variable COGS, and variable SG&A.

Then to EBITDA, EBIT, EBT, Net income & EPS.

Simple cash flow statements & balance sheets reconcile D&A to inflation-adjusted replacement CapEx, debt levels, & GAAP PP&E.

You have to be fluent in accounting to look at public companies.

Not because accounting itself matters.

But because accounting can obscure what matters.

And your task it to translate GAAP into meaningful business logic.

*3) Operating ratios*

Unit drivers output financials, financials output overall business ratios.

Revenue growth, EBITDA growth, EBITDA margins.

Contribution margins (= change in profit over change in revenue).

Net debt-to-EBITDA, net debt % of EV.

*4) Valuation*

You can drive valuation on multiples or a DCF.

Which are equivalent:

The discount rate minus the growth rate determines the 'terminal multiple.'

Using a P/E instead of a DCF simply uses next year as the terminal value.

This model drives value from the DCF, and maps that to the multiples to show how they connect.

*5) Corporate finance & DCFs*

DCF math attached using the CAPM.

The summary is a beta from historical returns, add the cost of debt.

To get the WACC - the theoretically correct discount rate.

DCFs are extremely assumption laden - you can get out almost whatever you want.

But realistically.

Your banker (or analyst) will make the math work out to a 7-13% discount rate.

Depending on the risks, industry, markets - and what they want to achieve.

*6) Sensitivities & the hard part*

The last section sensitizes the equity value and multiples to unit and price growth.

Bringing unit drivers full circle to valuation outcomes.

Ultimately, the hard part isn't the math.

You have to be fluent in the math, its nuances and its limitations.

If not, you will lose out to those who are.

But once you are, you also have to shift focus.

To the hard part.

Which is always in filling in the numbers.

If you're investing, that means thoughtful views on unit drivers; on how, when, and why they shift.

And if you're building, it means making the numbers on the page happen.

That's all for now.

Like & comment if you want the excel.