@jay_lits "Holds until something interesting walks in the door" is the entire story.

Every founder I know has a graveyard of pivots that started as "but this one is different."

Pre-committed criteria are how you stop negotiating with yourself in real time.

There's a difference between making discipline a value and making it a business model.

A value is aspirational. A business model is structural.

Aspirational discipline holds until something interesting walks in the door. Structural discipline doesn't bend.

Every dollar we deploy at @LiteStrategy clears the same bar:

- Does it grow our Litecoin position?

- Does it generate yield on existing holdings?

- Does it return capital to shareholders or strengthen the @litecoin ecosystem?

If the answer is no, the conversation ends there.

This has been the thesis since day one.

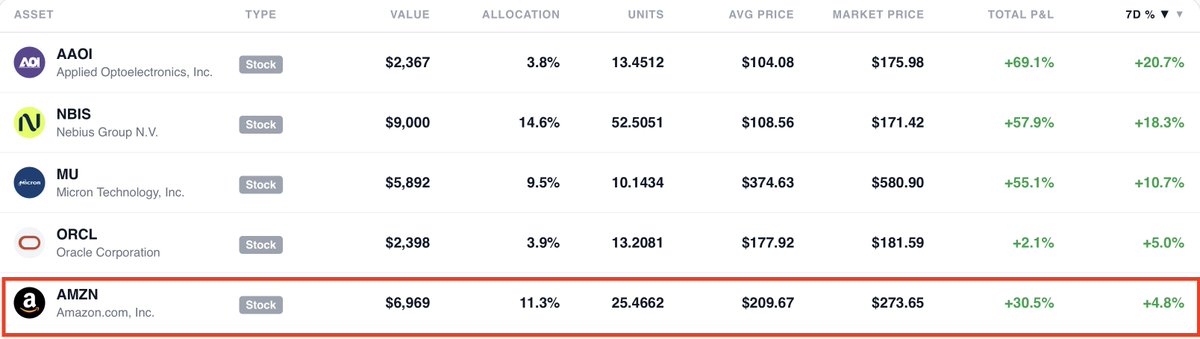

Amazon is still the most underrated stock in the Mag 7 and if you're sleeping on it, you're about to miss the next AWS moment (Save this).

Every few years, Amazon does something it has only done a handful of times in its history, it takes a capability it built for itself and opens it up to the world.

The first time it did this, it created AWS, a business now running at a $142 billion annual revenue rate, growing at 24% year over year, printing 35% operating margins, and projected by CEO Andy Jassy to hit $600 billion in annual revenue by 2036.

What started as Amazon's internal cloud became the backbone of the internet and today, it's doing it again, this time with logistics.

Amazon just launched Amazon Supply Chain Services opening its full freight, distribution, fulfillment, and parcel shipping network to any business on the planet.

And the early signups are P&G, 3M, Lands' End, and American Eagle Outfitters.

These are some of the most operationally sophisticated companies in the world, and they're handing Amazon the keys to their supply chains.

The proof of concept was already there.

Since 2006, independent sellers shipped more than 80 billion units through Fulfillment by Amazon and sellers using Amazon's end to end logistics see nearly 20% higher sales.

Amazon took that model, battle tested it across hundreds of thousands of businesses, and now it's offering it to the entire $1 trillion global 3PL market, a market projected to hit $2.1 trillion by 2032.

Now here's why the stock is still underrated, Amazon is trading at a

P/E of 32.7x on a market cap of $2.9T.

That multiple barely prices in what's already in the building, AWS re accelerating, advertising crossing $50 billion plus and gross margins expanding to 50% in 2025 and this doesn't price in ASCS at all.

This is a company that just opened a new enterprise logistics revenue line targeting a trillion dollar market, and the market is treating it like nothing happened.

The financials back the bull case hard, FY2025 revenue hit $716.9B , up

12.4% year over year. Q1 2026 came in at $181.5B in revenue with EPS of

$2.78, 74% above the consensus estimate.

Milk Road now see $810B in revenue for FY2026 and the earnings machine is not slowing down.

The capex spend $200B in 2026, looks scary on paper but it's the same bet Bezos made with AWS in the early 2000s. Build infrastructure nobody else can afford to replicate, then monetize it for decades.

Every dollar Amazon is spending on robotics, AI forecasting, and logistics density is making the same network it just opened up to enterprises cheaper and faster to operate.

That's operating leverage compounding in real time and this is exactly why Milk Road analysts remain bullish on Amazon.

AWS is accelerating into the AI supercycle and sitting on $244 billion in contracted backlog, ASCS is a multi year enterprise revenue unlock that is just getting started.

We've already started building a significant position and is up on it massively.

If you want to see exactly how we're sizing it, what we're buying, and our full thesis, come join us.

Link in below!

This is Leopold Aschenbrenner and this clip is from before the hedge fund, before the 13F filings, he raised $225 million and turned it into over $5.5 billion.

This is the thesis in its raw form, his point is simple, look at the jump from GPT-2 to GPT-4 (Save this).

GPT 2 was 2019 and it could sort of count to five before getting confused.

GPT 4 arrived just 3–4 years later scoring in the 90th percentile on exams like the bar, LSAT, and GRE, while solving complex math and playing chess.

That’s not incremental progress but rather a leap into an entirely new category of intelligence in less time than a college degree and his conclusion, play that forward.

Just a few more jumps like that, on a fairly short time horizon, basically this decade and we're going to hit extremely, extremely powerful systems.

Now here's where it gets interesting. Leopold didn't just say this but he put real money behind every implication of it.

His thesis was, if AI scales this fast, it will need compute at a scale the world has never built before.

The bottleneck won't be the algorithms bur rather the physical infrastructure like power, data centers and networking.

So while everyone else was buying Nvidia, Leopold was buying what Nvidia depends on.

Bloom Energy, CoreWeave, Lumentum, Core Scientific, Iren, Applied Digital, even Intel calls all ripping as AI turns power, compute, and chips into the real bottlenecks.

The whole fund is just the GPT-2 to GPT-4 chart, extended forward, and then asked, what does the world need to exist for that to happen?

He answered that question, then bought it.

Milk Road PRO is doing the same, come join us for our entire thesis Link below.

Q1 2026 was the strongest quarter in Sky Protocol's history.

Sky Frontier Foundation has published the full Q1 2026 Report, a complete breakdown of protocol financials, supply growth, and collateral expansion.

Read the key insights on @SkyEcoInsights ↓

This is WILD!

Bloom Energy just reported Q1 2026 earnings and the stock is up nearly 10% in after hours right now.

And the man with the most to gain is a 24 year old who got fired from OpenAI.

Leopold Aschenbrenner ran safety research at OpenAI until the company let him go.

He then wrote a 165-page essay arguing that AGI was arriving faster than any investor understood and that the people who would win were not the ones who owned the best AI model.

They were the ones who owned the electricity and that thesis became a hedge fund called Situational Awareness LP and he turned $225 million into $5.5 billion in under twelve months.

His largest single position is an $875 million stake in Bloom Energy and with tonight's 10% move, that position is now worth more than $2.2 billion and still climbing.

The catalyst is obvious in hindsight but almost no one saw it coming.

Bloom announced a 2.8 gigawatt fuel cell deal with Oracle, the largest on site power commitment in the history of enterprise computing.

Bloom delivered in 55 days against a 90-day commitment, Oracle gave Bloom a warrant for 3.53 million shares and the total backlog is now estimated at $20 billion.

His other major positions follow the same electricity-first logic.

$700 million in CoreWeave and a massive short on Infosys betting that AI coding agents destroy the outsourced IT business.

Intel call options printing multiples on a 53% run and a 10% activist stake in Core Scientific, a Bitcoin miner converting its power infrastructure into AI data center hosting.

The entire Wall Street AI trade was piled into model companies and chip companies.

Aschenbrenner looked at the same thesis and concluded the real bottleneck was whether the power grid could deliver enough electricity to run the models.

He was right, and the returns are public record.

One of our analysts at Milk Road called this exact play two months ago, took a massive position in Bloom Energy, and it is already up over 55%.

If you want access to the full thesis and what we are watching right now, go PRO. Link below.

Meta just signed a deal with Amazon to deploy tens of millions of AWS Graviton CPU cores into its AI infrastructure and Andy Jassy himself called it out as one of the most important signals in tech right now.

"Agentic AI is becoming almost as big a CPU story as a GPU story."

There are two reasons CPUs have become critical at scale.

The first is reinforcement learning, you don't just dump data into a model and train it anymore.

You put it in an environment, give it tasks, let it try things, score its outputs, and train on what worked and those environments run on CPUs, not GPUs.

The more capable AI gets, the more complex those scoring environments become and all of it runs on CPU.

The second is deployment, once a model is trained, its outputs don't go straight from a GPU to a human.

They route through apps, APIs, and agent workflows, all CPU bound on the backend.

That's exactly what this Meta-AWS deal confirms.

Graviton5 runs 192 Arm Neoverse V3 cores on 3nm TSMC, with a cache 5x larger than the prior generation and 33% lower inter-core latency, purpose-built for agentic workloads at this scale.

The demand signal is staggering, Andy Jassy revealed two large customers tried to buy out Amazon's entire 2026 Graviton capacity and he had to turn them down.

Amazon's chip business is running at a $20 billion annual revenue rate, growing triple digits and Jassy says if sold standalone, it's closer to a $50 billion run rate.

Everyone was watching GPUs but our analysts at Milk Road saw this coming.

Two of our top Pro holdings are AMD and Amazon, both sitting directly in the path of this CPU buildout before today's headlines.

If you want to see what we're buying next, come join us.

Link below.