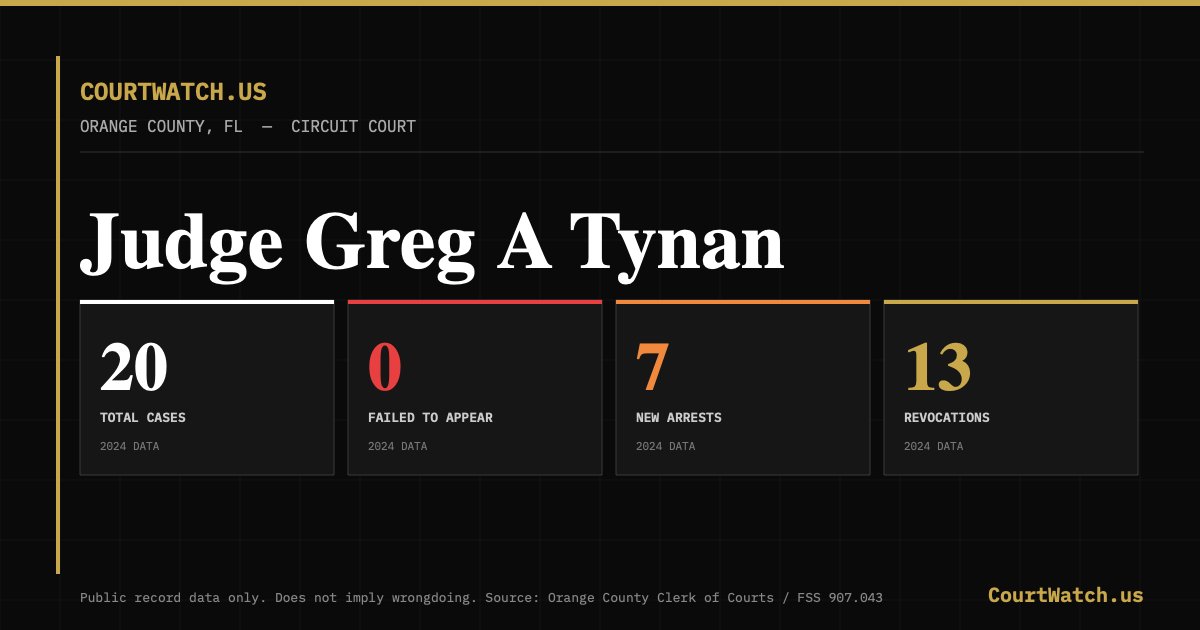

I built https://t.co/R1jAMUfNTv — a free public database for American citizens who deserve safer communities.

You can track which judges released defendants who then got rearrested, skipped court, or violated their release conditions. All public records. All free.

I started with Orange County FL and will be expanding to all 67 Florida counties and eventually every state in the country. This first batch of info is from 2024 and since public reports are released in March/April for the previous year, data is behind. But I wanted to see if this is plausible. After adding 2024,I'll add 2025 and then figure out how to get real-time-data uploaded.

It's in beta — would love to know what you think 👇

Numbers don't lie, but criminals do.

https://t.co/DfTcJ6XMYn

@bennyjohnson@jockowillink@GrantCardone@LauraLoomer@nickshirleyy@j_fishback

On my way to the Logan Square Farmers Market I see @BickerdikeRC still hasn't rented out the prime storefronts across street from the train station.

Why? Because it's actually work to rent out commercial space & everyone already made their money.

Affordable housing hustlers👇

BREAKING: The delinquency rate on Commercial Mortgage-Backed Securities (CMBS) for offices surged +51 basis points in March, to 11.71%, the 2nd-highest on record.

This is now 1.0 percentage point above the post-2008 Financial Crisis peak set in 2012.

Furthermore, the delinquency rate for multifamily CMBS rose +30 basis points, to 7.15%, the highest in 10 years.

As a result, the overall US CMBS delinquency rate rose +41 basis points last month, to 7.55%, the highest since the 2020 pandemic.

Since 2023, this percentage has risen +450 basis points.

The commercial real estate downturn is deepening.

JB Pritzker's unemployment office sent $5 BILLION to dead people, inmates, and fraudsters.

DEAD PEOPLE CASHED CHECKS.

If this is what they let us see, what the heck are they hiding?

Illinois spent $5 billion more than it took in last year.

Lawmakers' proposed solution: a 3% surtax on millionaires to raise $4-5 billion.

Notice the math.

Even if the tax performed at the most optimistic projection (and no one left) it would barely close last year's gap.

It doesn't solve the structural problem. It papers over it for a cycle. The structural problem is spending growth.

Illinois government spending has been growing far faster than the economy or the population. Until that trajectory changes, no amount of new revenue closes the gap permanently.

You're filling a bathtub with the drain open.

The alternative that actually works: a smart spending cap.

Tie government spending growth to the rate of economic and population growth. Anything beyond that threshold requires voter approval. Both red and blue states have adopted versions of this. It doesn't require raising taxes on anyone.

It just requires fiscal discipline.

Meanwhile, the people whose taxes Springfield wants to raise are the same people leaving at the fastest rate. IRS data shows high earners departing Illinois at 2x the rate of other groups.

A million net taxpayers have left in a decade, taking $88 billion in income. Massachusetts, the state that just tried this, saw $4 billion leave in year one and its total income base shrink.

You can't close a deficit by shrinking your tax base.

Houston Office Availability Rate Q1 2026 29.5%

Inventory 180,502,679 SF

Direct Available 48,897,200 SF

Sublet Available 4,368,075 SF

-Cushman and Wakefield

#commercialrealestate

The vaccine dosage was obviously too high and done too many times.

I had the original Wuhan virus before there was any vaccine and it was much like any other cold/flu. Bad, but not terrible.

But my second vaccine shot almost sent me to the hospital. Felt like I was dying.

@VladTheInflator Received an auction notice for a $7 million 1st TD loan circa 2025 for a 829,500 sf, 29 story office building in downtown Chicago. Current pay 20% interest only... You do the math

@VladTheInflator Private Mortgages akin to Private Debt are the issue rampant in Public pensions but worst hit will be life insurance backing annuities https://t.co/xow9fyNlnr

Truth. I see a great divide between some boomers who want to force RTO and the rest of the generations who know WFH works well and that there are ways to ensure those who abuse it are not going unnoticed. It’s like we have two nations. We have a group that literally wants to live like it’s 1990 and the rest of us.

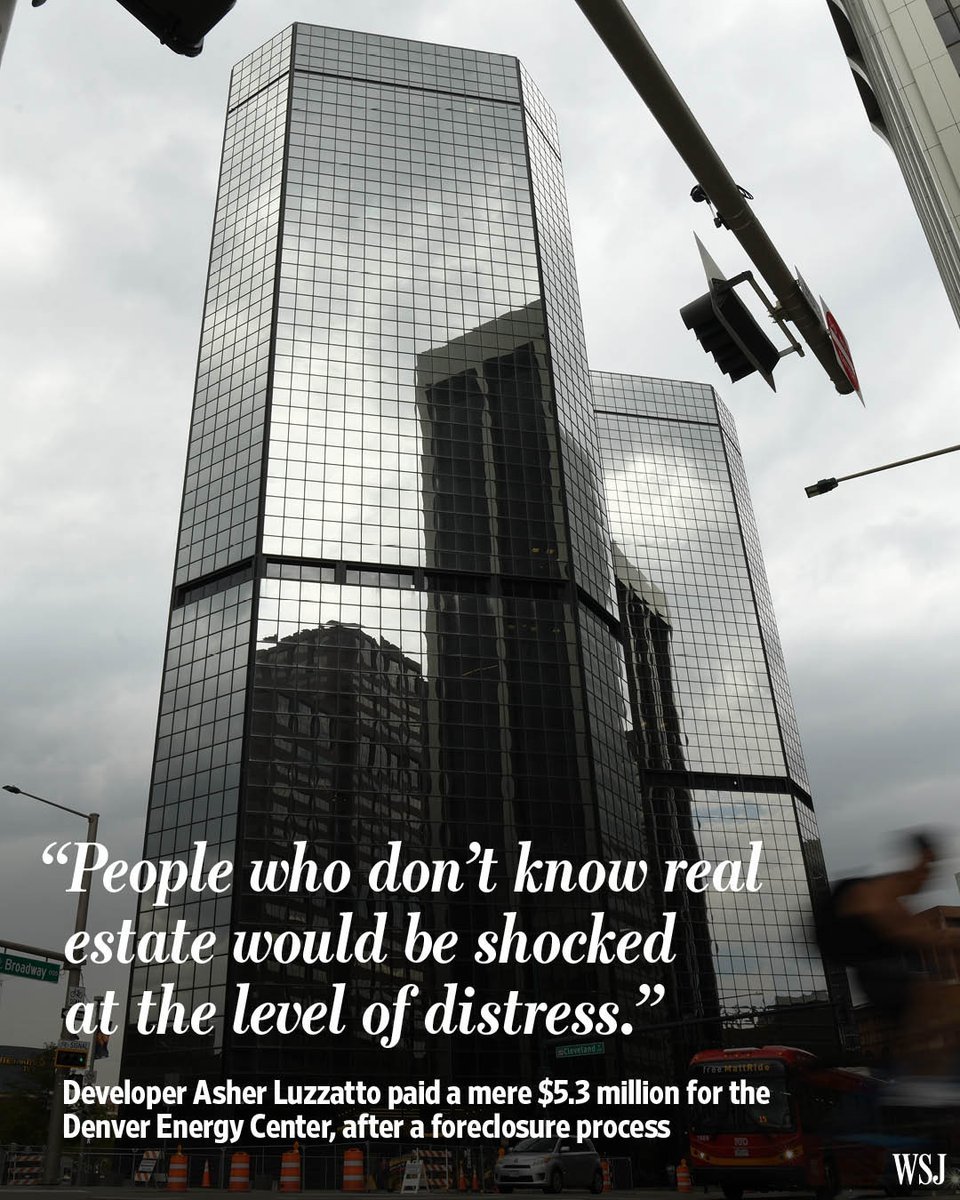

You are not wrong. If you want to see the distress follow the CMBS (Commercially Mortgaged Backed Securities) Market.

The loans go into receivership if you are servicing debt because the debt is beyond the equity. It is not a long term fixed rate market. It is a typically 5 to 7 years and June 2026 is going to be the lighting rod...but it is already happening.

There are several leftists cities like Seattle, Portland, LA that will suffer multi BILLION dollar budget disasters in the next few years due to the massive reset in commercial property value. ..and the subsequent lower tax reassessment as a result. This bomb will go off much sooner tha their pension crisis.

The unrealized losses on corporate balance sheets is epic. Said loans are on the books for the original loan amounts, not current market valuations. These equate to billions, if not trillions in toxic debt. Many of these loans will eventually have to be refinanced. Numerous small and medium sized banks own this bad paper. That’s when the party starts in earnest.

@VladTheInflator Question: if they don’t mark to market and pay taxes on it, are they over paying annual taxes to city/state just to avoid marking it correctly?

@DanHaskins25151 yes correct. Its all a charade praying rates fall to zero again, AI disappears and work from home goes away.

What it really is, is a pillaging they're trying to extend as long as they can

The office market is toast and it's never going to recover.

The fun part is a lot of these are hidden in private equity and shoved into pensions funds. They aren't being marked to market.

So everyone is insolvent and no one is admitting it yet.

Even more fun, allllll the state and local governments that need to tax theft to survive.