Viceory's estimate of 895,000 eligible loans seems to be based on dividing the loan book by the average loan value of £5.5-7.2k over the 2007-2023 period. Was the Irish book removed? Are these the original loan values not the lower book values? https://t.co/wUzBlVII3c

Why the numbers in the Adam Smith Institute's new paper on Motability are so far off the mark - and the case for expanding Motability-type arrangements to help lower income households obtain access to mobility. My new blog at https://t.co/9oLPLV2K8n

What's missing from today's Buy Now Pay Later Regulation announcement? 1) The market is now all about PayPal and Klarna 2) Providers can shift to the long-established and simpler revolving credit regulation instead. Details in my post here:

https://t.co/Q0RFPe8djx

The "wild west" of Buy Now Pay Later? By the time the Sheriff arrives, the market may have solved the problem. My new article at https://t.co/CWmiAYWUGF

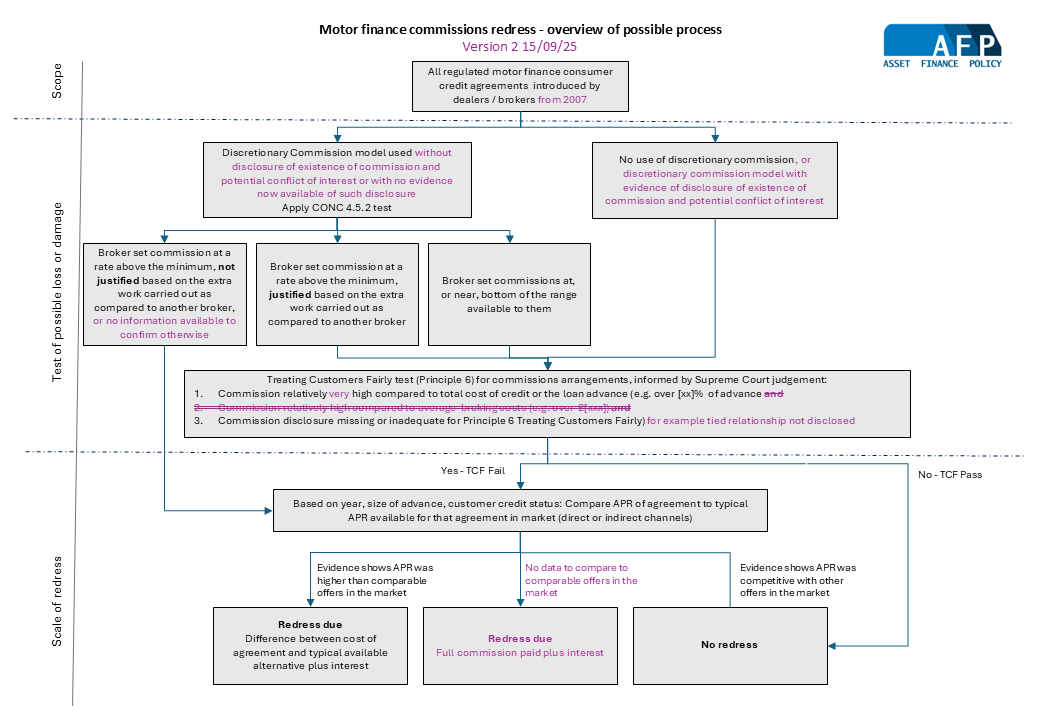

🔷 Reading between the lines of the FCA's update on motor finance commissions complaints.

My new blog analyses the FCA's updates on its (slow) progress yesterday. I suggest the FCA's eventual interventions will be more targeted than many expect.

https://t.co/QCbKORGq1O

Check out my latest article: Can Barclays or S&U turn the motor finance regulatory tide in the interests of consumers? https://t.co/7nMBSK2xKJ via @LinkedIn

Used car finance customers are already paying more in real terms than when FCA first objected to dealer commissions in 2019. One of the reasons why a redress scheme may be less dramatic than some estimates - my article for #AssetFinanceInternational https://t.co/Zpz6vcljKZ

Why Difference in Charges (usually) works well for consumers in motor finance. My summary of why the commission models under investigation are likely to have actually worked in consumers' interests. https://t.co/kfeHXyhAp0 https://t.co/LCAjHdPGm8

Why the collective action on UK used car finance commissions against Black Horse, Santander Consumer and MotoNovo Finance should fail. My new article is at: https://t.co/7hiUMSpDN5

@stellacreasy The answer could be existing regulation, if only HMT recognised BNPL for what it is - running account credit. It would be proportionate and effective. Details at: https://t.co/TaoblAOwAT

If only BNPL was recognised for what it is - running account credit - the regulatory problem disappears overnight. Correctly applied, the existing regulation would be proportionate and effective. Details: https://t.co/TaoblAOwAT

https://t.co/FYPvT4WOX3

What connects this week's FCA censure of Amigo loans, HM Treasury BNPL consultation, and reports of Barclays Partner Finance 'scaling back' its retail point of sale solutions? My latest blog: https://t.co/NjAp6kCwx9

Smarter regulation in 2023: Consumer Duty works, FRED 82 doesn't. My new blog sets out what seem likely to be the two most significant regulatory developments impacting asset finance this year. See https://t.co/6k2WOzFaYs

Despite all the finger-pointing, fraud on Bounce Back loans is now estimated by lenders at £1.1 billion, or 2.3% of total loans, compared to current official estimate of 7.5% and previously 11% (£4.9bn). My blog at: https://t.co/DkPGyf6wEB

Will the FCA's new Consumer Duty rules end dealer groups putting barriers in the way of consumers searching for lower cost car finance? New blog and industry reaction here #consumerduty

https://t.co/FuyFT9Z2wS?