$JD and $NVO are large positions in my portfolio. I have been in and out of options on $ADBE. I like the company the market just has no respect for them YET!! $NVO is probably my favorite of the 4. I was in $META in the $80’s and it did me well. I like deep discounts.

$NVO Novo Nordisk will likely become a trillion dollar company. I still can't believe how many key data points it ranks 1st in versus the top 10 Big Pharma companies.

-Oral GLP-1's parabolic growth is going to pull a $META type move over the next 3+ years. Oral GLP-1 is Meta/ Instagram ad rev. Injections are like TikTok.

Rev & use will show via Orals. $LLY $ABBV $MRK $HIMS

-NVO ranks 1st out of the top 10 Big Pharma

1st ROIC 45.29%

1st Lowest P/S 4.00

1st Pretax Margin 47.52%

1st Upside to 52 wk high +77%

1st Global GLP-1 Market Share

1st Oral GLP-1 Launch Trajectory

1st Weekly Oral GLP-1 Prescription Growth

1st GLP-1 Prescription Scale

1st GLP-1 Brand Mindshare

1st Diabetes GLP-1 Franchise

1st Lowest P/E 10.81

1st Lowest EV/Revenue 4.34

1st Lowest EV/EBIT 9.56

1st Lowest EV/EBITDA 8.34

1st Lowest Relative Volume 0.56

1st Highest CapEx $13.51B

1st Highest % gain 1 month 21%

1st MA Rating Strong Buy

1st RSI 74.18 despite lowest relative volume / 1M Gain %

1st Positive MACD Level 1.76

1st Positive MACD Signal 1.14

-The market is pricing Novo like a slowing legacy pharma company while oral GLP-1s IMO will massively expand the total addressable market over the next decade.

-Nobody wants to pin themselves with a needle but stats show everyone will take a pill if it means changing their lives.

-One in eight adults already report currently using GLP-1 drugs and oral adoption is just getting started.

-Wegovy pill prescriptions are already showing explosive early trajectory growth.

-If oral GLP-1 adoption scales globally this could become one of the largest recurring healthcare markets in history.

-If I had to hold one stock even through a bear market this is my current pick.

I have been buying shares & LEAPS the last month here.

It is also a huge % of my Deep Value fund up 16% the last 2 weeks.

If you want to know exactly how I have been positioning myself and fund here, give me a follow!

Uranium went from $30 a pound to $98 a pound in 6 years.

The mining stocks did 5x to 7x in the same window.

Microsoft and amazon just signed deals to power their AI data centers with nuclear. The uranium they need does not exist in the global supply…

Most people have no idea what's happening with uranium in 2026.

AI data centers consume 8-12x more power than traditional data centers. The biggest tech companies need 50+ gigawatts of new power capacity by 2030. Renewables can't run a data center 24/7. Natural gas is politically blocked. The only path is nuclear.

Microsoft just signed a 20-year deal to buy nuclear power from Three Mile Island. Amazon signed with Talen Energy. Google signed with Kairos. Meta is in talks.

50 gigawatts requires roughly 9,000 tonnes of uranium per year.

Current global uranium mining: 50,000 tonnes a year. Current demand pre-AI: 65,000 tonnes a year. The supply deficit was already 15,000 tonnes a year before the tech companies showed up.

Add the AI demand and the deficit triples.

The fastest way to position on the structural shortage is the 5-position nuclear stack.

I started buying uranium in 2020 at $30 a pound. NXE was a $0.95 stock when i bought it. It's at $7.85 today. Total time managing the position: 15 minutes a quarter.

Move 1. Pick the 5 names. CCJ (Cameco, the largest western producer). NXE (NexGen Energy, the biggest undeveloped high-grade deposit). DNN (Denison Mines). URA (Sprott Uranium Miners ETF). URNM (North Shore Uranium ETF).

Move 2. Set the allocation. 35% CCJ. 20% NXE. 15% DNN. 15% URA. 15% URNM.

Move 3. Track long-term contract pricing weekly. Uranium has 2 prices: spot and term. Term is 70% of all volume. Currently $84 a pound. Above $100, marginal mines come back online and supply restarts. Free at uxc. com.

Move 4. Watch the hyperscaler PPA announcements. Set google alerts for "data center nuclear PPA" and "small modular reactor agreement." Every announcement is a 20-year demand commitment.

Move 5. Watch the kazakhstan situation. Kazakhstan produces 43% of global uranium. Russia transports the conversion services. The supply chain has 2 chokepoints. When russia restricts uranium exports (already happening), CCJ runs.

Move 6. Quarterly rebalance. 15 minutes.

The asymmetry nobody talks about.

S&P 500 on $50K: $7,000 a year average.

Energy ETF on $50K: $4,800 a year. Diluted by oil majors.

Nuclear stack on $50K: CCJ +112% over 24 months, NXE +208%, DNN +156%, URA +89%. Blended 124% over 24 months. $62,000 in pure capital appreciation.

Plus the AI demand cycle has not peaked. The structural shortage has 6+ years of runway.

i run 6 sub-portfolios across 6 account types. They've appreciated 89% in 18 months while i barely look at them. 8,000 of my goat academy students hold positions in these names. Combined exposure: over $1.1B.

The 2026 NRC small modular reactor approvals will trigger another leg up. Window: 6-12 months.

I'll probably regret posting this. Once CNBC starts running uranium segments, the spot price runs to $150 and the miners overshoot.

(the entire western world bet its energy security on solar panels made in china. the AI data center build-out hit. the only reliable carbon-free baseload power is nuclear. the only fuel for nuclear is uranium. the only major mining companies are in canada, australia, and kazakhstan. the supply chain runs through russia. nobody planned this. somehow we're going to have to figure it out anyway.)

This is my once in a lifetime FREE webinar.

I'm walking through the exact 5-position nuclear stack live. Plus the uxc term-price tracker and the hyperscaler PPA calendar.

I started buying when uranium was unfashionable. The window to be early is closing.

Limited spots. Link in comments: https://t.co/1j7Dmb4qHR

$NVO Novo Nordisk is a future trillion dollar company. The market still does not understand what Oral GLP1 will become. Wegovy pill is seeing monster adoption & GLP1s are expanding beyond obesity into cardiovascular disease, diabetes, addiction & potentially longevity related markets. At barely 4x sales & around 13x earnings, the valuation compression here is extreme for a company still generating elite margins, cash flow & global growth. The market has been treating this like a temporary pharma trend. I think Oral GLP1 becomes one of the biggest pharmaceutical categories in history. I went in big the last two weeks Shares & Leaps. Reminds me of $META at $88 recently haha. My full writeups on my substack. Congrats to those that saw it too!

💊 $HIMS Big Picture…

1. HIMS received a FDA warning letter addressed to @AndrewDudum on September 9, 2025. Andrew had to respond to the letter with specific steps they’d change from their advertising.

2. Andrew appeared to change very little, non-compliant ad’s continued to run for 5 months

3. HIMS angered FDA, leading to pending actions taken against their API suppliers. This directly threatens existing GLP1 injectable products now. A DOJ referral is made to the justice department as well.

4. HIMS launches cancer screenings which aren’t FDA approved & accuracy is dubious. HIMS uses their Super Bowl ad to promote.

5. HIMS acquires at-home lab device, YourBio but elects to not pursuit broad at-home testing. Other competitors launch free at-home labs by narrowing testing to labs relevant to their platform.

6. HIMS maintains peptide research partnership with CS Bio Co, but prioritizes less popular product launches instead.

➡️ There’s so many poor leadership judgements & uncertain legal and regulatory overhangs, $HIMS trajectory remains tragically unclear.

Anfield: A Near Term 🇺🇸 #Uranium Producer

Anfield Energy $AEC owns Shootaring Canyon Mill, one of the only licensed mills in 🇺🇸. Backed by a ~30% stake from Uranium Energy Corp $UEC, the co. broke ground on its Velvet-Wood mine, & 🎯 its first production milestones for 2026.

ASML Just Obliterated The "Peak AI" Narrative

$ASML

By Hataf Capital

If you have been listening to the bears lately, you have probably heard the narrative that we are approaching "peak AI" or that the infrastructure spend is getting ahead of itself.

Well, ASML Holding NV $ASML just took that narrative and completely dismantled it.

The Dutch semiconductor equipment giant reported its Q4 order bookings on Wednesday, and the numbers were not just good they were absolutely staggering. The market was expecting bookings of €6.85 billion. Instead, ASML delivered a record €13.2 billion ($15.8 billion).

Let that sink in for a moment. They didn't just beat estimates; they nearly doubled them.

I have been writing about the AI infrastructure buildout for months, covering everything from Nvidia’s dominance to Dell’s server pivot and the power constraints benefiting Vistra and Constellation Energy. But ASML’s report is arguably the most critical data point we have seen yet because ASML sits at the very beginning of the supply chain.

You can’t build an Nvidia H100 or the upcoming Blackwell chips without ASML’s photolithography machines. They are the toll booth for the entire semiconductor industry. When ASML posts a record quarter of this magnitude, it sends a clear signal: the largest technology infrastructure buildout in human history is accelerating, not slowing down.

The "Veldhoven" Signal

What makes this report so compelling to me isn't just the headline number; it is the composition of those orders. More than half of the bookings €7.4 billion were for their Extreme Ultraviolet (EUV) lithography machines.

These are the most sophisticated, complex, and expensive machines in the world, required to manufacture the most advanced chips at 3nm and 2nm nodes. This tells us that the demand isn't for legacy nodes or commodity chips; it is squarely focused on the bleeding edge of compute power required for training and running massive AI models.

ASML’s Chief Executive Officer Christophe Fouquet explicitly stated that customers have a "notably more positive assessment of the medium-term market situation." This directly contradicts the fears of an "AI air pocket" or a pause in spending.

In fact, this aligns perfectly with what we are seeing from the hyperscalers. Meta Platforms and Microsoft are pouring hundreds of billions into data centers. TSMC just announced they anticipate capital spending of more than $52 billion in 2026. You don't spend $52 billion on CapEx unless you have a crystal clear line of sight into end-market demand.

The Trillion-Dollar Infrastructure Play

Jensen Huang, Nvidia’s CEO, recently called this the "largest infrastructure build out in human history" and estimated a need for trillions of dollars of additional investment.

I believe the market is still having trouble wrapping its head around the sheer scale of this. We are moving from general-purpose computing to accelerated computing, and that requires replacing roughly $1 trillion worth of traditional data centers with AI factories.

ASML’s machinery is the integral component in this transition. The fact that their order book exploded to this degree confirms that chipmakers like TSMC, Intel, and Samsung are racing to secure capacity for 2026 and beyond. They are voting with their wallets, and that vote is a resounding vote of confidence in the longevity of the AI cycle.

The China Floor

There is another aspect of this report that I think the market is underappreciating, and that is the resilience of the Chinese market.

Despite US-led restrictions preventing ASML from selling its most advanced EUV and even some deep ultraviolet (DUV) tools to China, the region still accounted for 36% of net system sales in the fourth quarter.

While Chinese chipmakers are restricted to buying older equipment that is eight generations behind the most sophisticated models, the demand remains robust. They are buying up older equipment to manufacture mature chips, which creates a solid revenue floor for ASML while the AI boom provides the exponential ceiling.

The Valuation Reality

The AI boom has pushed ASML’s market value over $500 billion this month, and looking at the guidance, I believe this premium is justified. Revenue is seen between €34 billion and €39 billion this year, which is higher than previous guidance.

However, there is one piece of "fine print" in the report that investors need to watch. ASML stated they won’t report bookings in future quarterly reports, arguing the metric doesn't accurately capture business momentum due to lumpiness.

Usually, when a company stops reporting a key metric, it raises a red flag. But given the massive lead times and the astronomical price tag of these machines, quarterly bookings can indeed be incredibly volatile. The sheer size of the backlog they just built gives them tremendous visibility, regardless of quarter-to-quarter fluctuations.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]

🚨 $ASML Q4-25 Earnings are out! 🚨

Shares are up 9% initially!!!

- Rev: €9.7B vs est: €9.58B 🟢

- EPS €7.35 vs est €7.55 🔴

- Gross Margins: 52.2% vs est 52% 🟢

- Net bookings: €13.2B vs est €7B 🟢

Total sales 2025: €32.7

Backlog at the end of 2025 of €38.8B

Outlook Q1-26

Rev: €8.2B - €8.9B - consensus was €9.3B 🔴

Gross margin: 51-53% - consensus 5.1% 🟢

FY guidance for 2026:

ASML expects 2026 total net sales to be between €34 billion and €39 billion, with a gross margin between 51% and 53%. Estmates were around €35!B

Update on the buyback program:

New share buyback program of up to €12B to be executed by December 31, 2028

Highlights from the CEO statement:

"ASML reported another record year in 2025, with total net sales of €32.7 billion and a gross margin of 52.8%. The fourth quarter was particularly strong: we reported record total net sales of €9.7 billion, including the revenue recognized for two High NA systems. Our gross margin for Q4 was in line with our guidance at 52.2%.

"In the last months, many of our customers have shared a notably more positive assessment of the medium-term market situation, primarily based on more robust expectations of the sustainability of AI-related demand. This is reflected in a marked step-up in their medium-term capacity plans and in our record order intake.

"Therefore, we expect 2026 to be another growth year for ASML's business, largely driven by a significant increase in EUV sales and growth in our installed base business sales1.

I will give a full analysis of the earnings later today on my SS. Link in my bio.

1/7 Part of learning a biz is understanding their products and how they make money. And as I prep for this week's shallow dive into $NVO

Below is a short thread helping to explain GLP-1 from a beginners point of view. Keep in mind, not a doctor or scientist.

🧵⬇️

$NVO 's Oral Wegovy is taking off in the U.S.

New prescriptions jumped from 4,289 → 20,371 in the first two weeks after launch.

For comparison (week 2):

• Wegovy injection: 1,017

• Zepbound (Eli Lilly): 10,026

Insured patients only.

#StocksInFocus#investing

🚨 BREAKING: $NVO'S WEGOVY PILL SALES HIT A RECORD 20,371 IN WEEK 2!!!

Compare this to last week's 4,289 number (which was already very good), and you can see how big this is.

For comparison: Zepbound did 10k in week 2 and the injectable Wegovy did just over 1k in it's second week upon launch

So these numbers are very very promising and show how much interest there is in oral pills for weight-loss.

And keep in mind, this is excluding telehealth and Novocare numbers.

Even though sentiment is already changing, it seems to me the market is still heavily underestimating the impact the new oral GLP-1 era will have on revenue for both $NVO and $LLY.

🚨 $NVO 2ND WEEK WEIGHT LOSS PILL NUMBERS COME IN AT 20,371 SCRIPTS

BIGGER NUMBERS THAN THE HISTORICAL LAUNCHES OF LEADING BLOCKBUSTER INJECTIONS FROM BOTH $LLY & $NVO

ANALYSTS SAY THIS IS UNPRECEDENTED

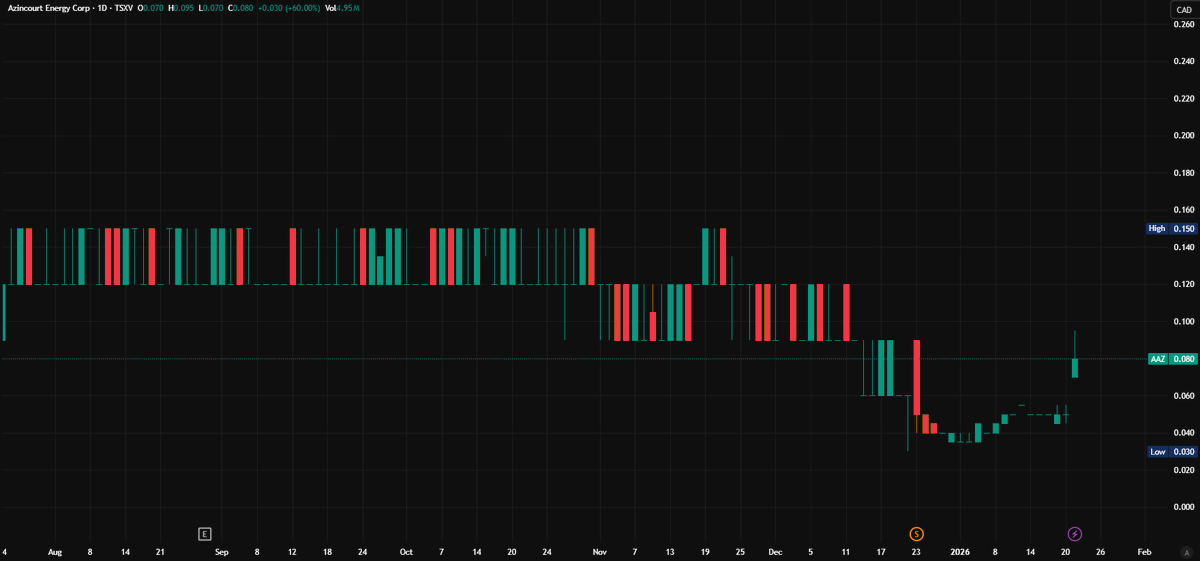

Today's pick is Azincourt Energy $AAZ.V.

Azincourt popped from $0.05 to an intraday high of $0.08, closing up around 60% on volume spiking to over 5M shares, 10x the average.

Welcome back to Catalyst Casefile.

We will deep dive a catalyst, walk through what lead up to it, map what changed, what would actually prove it, and the risks so you can track the stories like us.

Let's check it out! 👇🧵

![hataf_capital's tweet photo. ASML Just Obliterated The "Peak AI" Narrative

$ASML

By Hataf Capital

If you have been listening to the bears lately, you have probably heard the narrative that we are approaching "peak AI" or that the infrastructure spend is getting ahead of itself.

Well, ASML Holding NV $ASML just took that narrative and completely dismantled it.

The Dutch semiconductor equipment giant reported its Q4 order bookings on Wednesday, and the numbers were not just good they were absolutely staggering. The market was expecting bookings of €6.85 billion. Instead, ASML delivered a record €13.2 billion ($15.8 billion).

Let that sink in for a moment. They didn't just beat estimates; they nearly doubled them.

I have been writing about the AI infrastructure buildout for months, covering everything from Nvidia’s dominance to Dell’s server pivot and the power constraints benefiting Vistra and Constellation Energy. But ASML’s report is arguably the most critical data point we have seen yet because ASML sits at the very beginning of the supply chain.

You can’t build an Nvidia H100 or the upcoming Blackwell chips without ASML’s photolithography machines. They are the toll booth for the entire semiconductor industry. When ASML posts a record quarter of this magnitude, it sends a clear signal: the largest technology infrastructure buildout in human history is accelerating, not slowing down.

The "Veldhoven" Signal

What makes this report so compelling to me isn't just the headline number; it is the composition of those orders. More than half of the bookings €7.4 billion were for their Extreme Ultraviolet (EUV) lithography machines.

These are the most sophisticated, complex, and expensive machines in the world, required to manufacture the most advanced chips at 3nm and 2nm nodes. This tells us that the demand isn't for legacy nodes or commodity chips; it is squarely focused on the bleeding edge of compute power required for training and running massive AI models.

ASML’s Chief Executive Officer Christophe Fouquet explicitly stated that customers have a "notably more positive assessment of the medium-term market situation." This directly contradicts the fears of an "AI air pocket" or a pause in spending.

In fact, this aligns perfectly with what we are seeing from the hyperscalers. Meta Platforms and Microsoft are pouring hundreds of billions into data centers. TSMC just announced they anticipate capital spending of more than $52 billion in 2026. You don't spend $52 billion on CapEx unless you have a crystal clear line of sight into end-market demand.

The Trillion-Dollar Infrastructure Play

Jensen Huang, Nvidia’s CEO, recently called this the "largest infrastructure build out in human history" and estimated a need for trillions of dollars of additional investment.

I believe the market is still having trouble wrapping its head around the sheer scale of this. We are moving from general-purpose computing to accelerated computing, and that requires replacing roughly $1 trillion worth of traditional data centers with AI factories.

ASML’s machinery is the integral component in this transition. The fact that their order book exploded to this degree confirms that chipmakers like TSMC, Intel, and Samsung are racing to secure capacity for 2026 and beyond. They are voting with their wallets, and that vote is a resounding vote of confidence in the longevity of the AI cycle.

The China Floor

There is another aspect of this report that I think the market is underappreciating, and that is the resilience of the Chinese market.

Despite US-led restrictions preventing ASML from selling its most advanced EUV and even some deep ultraviolet (DUV) tools to China, the region still accounted for 36% of net system sales in the fourth quarter.

While Chinese chipmakers are restricted to buying older equipment that is eight generations behind the most sophisticated models, the demand remains robust. They are buying up older equipment to manufacture mature chips, which creates a solid revenue floor for ASML while the AI boom provides the exponential ceiling.

The Valuation Reality

The AI boom has pushed ASML’s market value over $500 billion this month, and looking at the guidance, I believe this premium is justified. Revenue is seen between €34 billion and €39 billion this year, which is higher than previous guidance.

However, there is one piece of "fine print" in the report that investors need to watch. ASML stated they won’t report bookings in future quarterly reports, arguing the metric doesn't accurately capture business momentum due to lumpiness.

Usually, when a company stops reporting a key metric, it raises a red flag. But given the massive lead times and the astronomical price tag of these machines, quarterly bookings can indeed be incredibly volatile. The sheer size of the backlog they just built gives them tremendous visibility, regardless of quarter-to-quarter fluctuations.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G_u7UJEbYAACJoM.jpg)

![hataf_capital's tweet photo. ASML Just Obliterated The "Peak AI" Narrative

$ASML

By Hataf Capital

If you have been listening to the bears lately, you have probably heard the narrative that we are approaching "peak AI" or that the infrastructure spend is getting ahead of itself.

Well, ASML Holding NV $ASML just took that narrative and completely dismantled it.

The Dutch semiconductor equipment giant reported its Q4 order bookings on Wednesday, and the numbers were not just good they were absolutely staggering. The market was expecting bookings of €6.85 billion. Instead, ASML delivered a record €13.2 billion ($15.8 billion).

Let that sink in for a moment. They didn't just beat estimates; they nearly doubled them.

I have been writing about the AI infrastructure buildout for months, covering everything from Nvidia’s dominance to Dell’s server pivot and the power constraints benefiting Vistra and Constellation Energy. But ASML’s report is arguably the most critical data point we have seen yet because ASML sits at the very beginning of the supply chain.

You can’t build an Nvidia H100 or the upcoming Blackwell chips without ASML’s photolithography machines. They are the toll booth for the entire semiconductor industry. When ASML posts a record quarter of this magnitude, it sends a clear signal: the largest technology infrastructure buildout in human history is accelerating, not slowing down.

The "Veldhoven" Signal

What makes this report so compelling to me isn't just the headline number; it is the composition of those orders. More than half of the bookings €7.4 billion were for their Extreme Ultraviolet (EUV) lithography machines.

These are the most sophisticated, complex, and expensive machines in the world, required to manufacture the most advanced chips at 3nm and 2nm nodes. This tells us that the demand isn't for legacy nodes or commodity chips; it is squarely focused on the bleeding edge of compute power required for training and running massive AI models.

ASML’s Chief Executive Officer Christophe Fouquet explicitly stated that customers have a "notably more positive assessment of the medium-term market situation." This directly contradicts the fears of an "AI air pocket" or a pause in spending.

In fact, this aligns perfectly with what we are seeing from the hyperscalers. Meta Platforms and Microsoft are pouring hundreds of billions into data centers. TSMC just announced they anticipate capital spending of more than $52 billion in 2026. You don't spend $52 billion on CapEx unless you have a crystal clear line of sight into end-market demand.

The Trillion-Dollar Infrastructure Play

Jensen Huang, Nvidia’s CEO, recently called this the "largest infrastructure build out in human history" and estimated a need for trillions of dollars of additional investment.

I believe the market is still having trouble wrapping its head around the sheer scale of this. We are moving from general-purpose computing to accelerated computing, and that requires replacing roughly $1 trillion worth of traditional data centers with AI factories.

ASML’s machinery is the integral component in this transition. The fact that their order book exploded to this degree confirms that chipmakers like TSMC, Intel, and Samsung are racing to secure capacity for 2026 and beyond. They are voting with their wallets, and that vote is a resounding vote of confidence in the longevity of the AI cycle.

The China Floor

There is another aspect of this report that I think the market is underappreciating, and that is the resilience of the Chinese market.

Despite US-led restrictions preventing ASML from selling its most advanced EUV and even some deep ultraviolet (DUV) tools to China, the region still accounted for 36% of net system sales in the fourth quarter.

While Chinese chipmakers are restricted to buying older equipment that is eight generations behind the most sophisticated models, the demand remains robust. They are buying up older equipment to manufacture mature chips, which creates a solid revenue floor for ASML while the AI boom provides the exponential ceiling.

The Valuation Reality

The AI boom has pushed ASML’s market value over $500 billion this month, and looking at the guidance, I believe this premium is justified. Revenue is seen between €34 billion and €39 billion this year, which is higher than previous guidance.

However, there is one piece of "fine print" in the report that investors need to watch. ASML stated they won’t report bookings in future quarterly reports, arguing the metric doesn't accurately capture business momentum due to lumpiness.

Usually, when a company stops reporting a key metric, it raises a red flag. But given the massive lead times and the astronomical price tag of these machines, quarterly bookings can indeed be incredibly volatile. The sheer size of the backlog they just built gives them tremendous visibility, regardless of quarter-to-quarter fluctuations.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G_u7CGFWYAAcVg1.jpg)

![hataf_capital's tweet photo. ASML Just Obliterated The "Peak AI" Narrative

$ASML

By Hataf Capital

If you have been listening to the bears lately, you have probably heard the narrative that we are approaching "peak AI" or that the infrastructure spend is getting ahead of itself.

Well, ASML Holding NV $ASML just took that narrative and completely dismantled it.

The Dutch semiconductor equipment giant reported its Q4 order bookings on Wednesday, and the numbers were not just good they were absolutely staggering. The market was expecting bookings of €6.85 billion. Instead, ASML delivered a record €13.2 billion ($15.8 billion).

Let that sink in for a moment. They didn't just beat estimates; they nearly doubled them.

I have been writing about the AI infrastructure buildout for months, covering everything from Nvidia’s dominance to Dell’s server pivot and the power constraints benefiting Vistra and Constellation Energy. But ASML’s report is arguably the most critical data point we have seen yet because ASML sits at the very beginning of the supply chain.

You can’t build an Nvidia H100 or the upcoming Blackwell chips without ASML’s photolithography machines. They are the toll booth for the entire semiconductor industry. When ASML posts a record quarter of this magnitude, it sends a clear signal: the largest technology infrastructure buildout in human history is accelerating, not slowing down.

The "Veldhoven" Signal

What makes this report so compelling to me isn't just the headline number; it is the composition of those orders. More than half of the bookings €7.4 billion were for their Extreme Ultraviolet (EUV) lithography machines.

These are the most sophisticated, complex, and expensive machines in the world, required to manufacture the most advanced chips at 3nm and 2nm nodes. This tells us that the demand isn't for legacy nodes or commodity chips; it is squarely focused on the bleeding edge of compute power required for training and running massive AI models.

ASML’s Chief Executive Officer Christophe Fouquet explicitly stated that customers have a "notably more positive assessment of the medium-term market situation." This directly contradicts the fears of an "AI air pocket" or a pause in spending.

In fact, this aligns perfectly with what we are seeing from the hyperscalers. Meta Platforms and Microsoft are pouring hundreds of billions into data centers. TSMC just announced they anticipate capital spending of more than $52 billion in 2026. You don't spend $52 billion on CapEx unless you have a crystal clear line of sight into end-market demand.

The Trillion-Dollar Infrastructure Play

Jensen Huang, Nvidia’s CEO, recently called this the "largest infrastructure build out in human history" and estimated a need for trillions of dollars of additional investment.

I believe the market is still having trouble wrapping its head around the sheer scale of this. We are moving from general-purpose computing to accelerated computing, and that requires replacing roughly $1 trillion worth of traditional data centers with AI factories.

ASML’s machinery is the integral component in this transition. The fact that their order book exploded to this degree confirms that chipmakers like TSMC, Intel, and Samsung are racing to secure capacity for 2026 and beyond. They are voting with their wallets, and that vote is a resounding vote of confidence in the longevity of the AI cycle.

The China Floor

There is another aspect of this report that I think the market is underappreciating, and that is the resilience of the Chinese market.

Despite US-led restrictions preventing ASML from selling its most advanced EUV and even some deep ultraviolet (DUV) tools to China, the region still accounted for 36% of net system sales in the fourth quarter.

While Chinese chipmakers are restricted to buying older equipment that is eight generations behind the most sophisticated models, the demand remains robust. They are buying up older equipment to manufacture mature chips, which creates a solid revenue floor for ASML while the AI boom provides the exponential ceiling.

The Valuation Reality

The AI boom has pushed ASML’s market value over $500 billion this month, and looking at the guidance, I believe this premium is justified. Revenue is seen between €34 billion and €39 billion this year, which is higher than previous guidance.

However, there is one piece of "fine print" in the report that investors need to watch. ASML stated they won’t report bookings in future quarterly reports, arguing the metric doesn't accurately capture business momentum due to lumpiness.

Usually, when a company stops reporting a key metric, it raises a red flag. But given the massive lead times and the astronomical price tag of these machines, quarterly bookings can indeed be incredibly volatile. The sheer size of the backlog they just built gives them tremendous visibility, regardless of quarter-to-quarter fluctuations.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G_u65eRaAAAIPCL.jpg)

![hataf_capital's tweet photo. ASML Just Obliterated The "Peak AI" Narrative

$ASML

By Hataf Capital

If you have been listening to the bears lately, you have probably heard the narrative that we are approaching "peak AI" or that the infrastructure spend is getting ahead of itself.

Well, ASML Holding NV $ASML just took that narrative and completely dismantled it.

The Dutch semiconductor equipment giant reported its Q4 order bookings on Wednesday, and the numbers were not just good they were absolutely staggering. The market was expecting bookings of €6.85 billion. Instead, ASML delivered a record €13.2 billion ($15.8 billion).

Let that sink in for a moment. They didn't just beat estimates; they nearly doubled them.

I have been writing about the AI infrastructure buildout for months, covering everything from Nvidia’s dominance to Dell’s server pivot and the power constraints benefiting Vistra and Constellation Energy. But ASML’s report is arguably the most critical data point we have seen yet because ASML sits at the very beginning of the supply chain.

You can’t build an Nvidia H100 or the upcoming Blackwell chips without ASML’s photolithography machines. They are the toll booth for the entire semiconductor industry. When ASML posts a record quarter of this magnitude, it sends a clear signal: the largest technology infrastructure buildout in human history is accelerating, not slowing down.

The "Veldhoven" Signal

What makes this report so compelling to me isn't just the headline number; it is the composition of those orders. More than half of the bookings €7.4 billion were for their Extreme Ultraviolet (EUV) lithography machines.

These are the most sophisticated, complex, and expensive machines in the world, required to manufacture the most advanced chips at 3nm and 2nm nodes. This tells us that the demand isn't for legacy nodes or commodity chips; it is squarely focused on the bleeding edge of compute power required for training and running massive AI models.

ASML’s Chief Executive Officer Christophe Fouquet explicitly stated that customers have a "notably more positive assessment of the medium-term market situation." This directly contradicts the fears of an "AI air pocket" or a pause in spending.

In fact, this aligns perfectly with what we are seeing from the hyperscalers. Meta Platforms and Microsoft are pouring hundreds of billions into data centers. TSMC just announced they anticipate capital spending of more than $52 billion in 2026. You don't spend $52 billion on CapEx unless you have a crystal clear line of sight into end-market demand.

The Trillion-Dollar Infrastructure Play

Jensen Huang, Nvidia’s CEO, recently called this the "largest infrastructure build out in human history" and estimated a need for trillions of dollars of additional investment.

I believe the market is still having trouble wrapping its head around the sheer scale of this. We are moving from general-purpose computing to accelerated computing, and that requires replacing roughly $1 trillion worth of traditional data centers with AI factories.

ASML’s machinery is the integral component in this transition. The fact that their order book exploded to this degree confirms that chipmakers like TSMC, Intel, and Samsung are racing to secure capacity for 2026 and beyond. They are voting with their wallets, and that vote is a resounding vote of confidence in the longevity of the AI cycle.

The China Floor

There is another aspect of this report that I think the market is underappreciating, and that is the resilience of the Chinese market.

Despite US-led restrictions preventing ASML from selling its most advanced EUV and even some deep ultraviolet (DUV) tools to China, the region still accounted for 36% of net system sales in the fourth quarter.

While Chinese chipmakers are restricted to buying older equipment that is eight generations behind the most sophisticated models, the demand remains robust. They are buying up older equipment to manufacture mature chips, which creates a solid revenue floor for ASML while the AI boom provides the exponential ceiling.

The Valuation Reality

The AI boom has pushed ASML’s market value over $500 billion this month, and looking at the guidance, I believe this premium is justified. Revenue is seen between €34 billion and €39 billion this year, which is higher than previous guidance.

However, there is one piece of "fine print" in the report that investors need to watch. ASML stated they won’t report bookings in future quarterly reports, arguing the metric doesn't accurately capture business momentum due to lumpiness.

Usually, when a company stops reporting a key metric, it raises a red flag. But given the massive lead times and the astronomical price tag of these machines, quarterly bookings can indeed be incredibly volatile. The sheer size of the backlog they just built gives them tremendous visibility, regardless of quarter-to-quarter fluctuations.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G_u7bszXMAAiorS.jpg)