Drugmaker Ipsen Sees More Deals Coming to Continue Buying Spree. $XBI

'We are going to continue to see what we can add to rare liver, but we are looking at adjacent areas. We have a lot of firepower left' - CFO

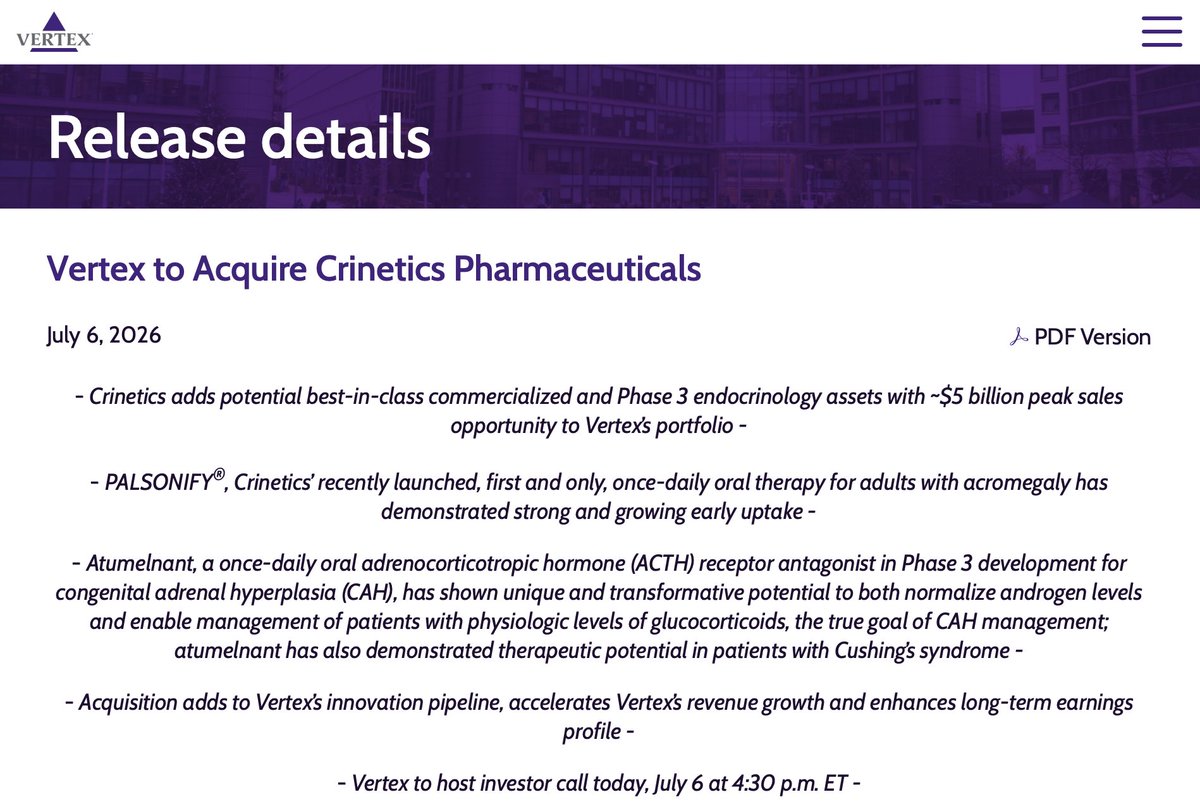

https://t.co/6l5vVBN6fn

With the Blessing of Sri Krishna, I am launching Bhāgavata-VāNi (Link next post)

The complete Śrīmad Bhāgavatam (all 12 skandhas) with synced audio recitation and karaoke-style highlighting.

- 10 scripts with topic descriptions

- ad-free

- stotra list,

- advanced searches

A 15-year-old dream has come true today. I started a PhD with the dream of creating a system that chants any Sanskrit shloka perfectly.

And here I am opening sourcing 𝐕𝐚𝐠𝐝𝐡𝐞𝐧𝐮 - 𝐀 𝐯ṛ𝐭𝐭𝐚 (𝐦𝐞𝐭𝐞𝐫) 𝐚𝐰𝐚𝐫𝐞 ś𝐥𝐨𝐤𝐚-𝐭𝐨-𝐜𝐡𝐚𝐧𝐭 𝐭𝐞𝐱𝐭-𝐭𝐨-𝐬𝐩𝐞𝐞𝐜𝐡 (TTS) 𝐬𝐲𝐬𝐭𝐞𝐦 𝐟𝐨𝐫 𝐒𝐚𝐧𝐬𝐤𝐫𝐢𝐭. This is the world's first vrutta-aware, open-source TTS for Sanskrit Chanting.

B Riley⬆️ $KYMR-$155 and reiterated Buy

CRVS APGE - $ABBV NKTR ORKA REGN $SNY GILD NRIX LLY

B Riley Commented: On 6/25, BMO, Buy-rated KYMR ($117 to $155 PT), unexpectedly announced completing BROADEN2 Ph2b enrollment in moderate-to-severe AtD roughly six months early, moving the topline to year-end 2026 from mid-2027 and advancing the planned Ph3 initiation to mid-2027.

We are buyers on this encouraging update, which converts KYMR's single most important value driver from a distant catalyst into a near-term event and resets the equity to a higher floor.

The majority ex-US enrollment footprint supports a contained placebo response setup in the readout, and the timing now puts it a clear step ahead of the rest of the oral STAT6 field and into the broader AtD/asthma space, which saw a floor value established by ABBV/Apogee's $11B transaction.

The acceleration also tightens a go-forward catalyst roadmap that also includes KT-579 IRF5 degrader Ph1 healthy-volunteer data in 2H26 (lupus the lead PoC indication), the Sanofi-partnered KT-485 IRAK4 degrader now in Ph1, and Gilead's KT-200 CDK2 molecular glue tracking to the clinic in 2027, each carrying partnered milestone flow against the wholly-owned core.

We raise our PT to $155 from $117 to reflect a launch we now model a year earlier and the scale and scope synergy of an AtD and asthma Ph3 program advancing in parallel into the back half of 2027.

Against a wholly-owned lead program KT-621 with multi-billion-dollar risk-adjusted sales, we view ~$8B EV as still constituting meaningful upside, with a broad slew of pipeline de-risking events anticipated in 2H26E.

@HOThomasWPhelps One thing to agree is their rate of trial enrollment is much faster

Market is appreciating it as the 2b readout timeline pushed to this year end

Perks of having lot of cash in hand to burn

@WallStSai Good take

I dont think they will go for it

For that matter $MRK $ABBV wont go for it rather find more compelling bolt on deals like $LLY does

$PFE did bought $SGEN for over $40 what is the roi

Large acquisition in AD space will make things interesting

Its been so long since $DICE bought out by $LLY

I think the next one would be $CRVS $NKTR(legal hangover unless its $LLY )