Data Sources:

Kaspa Network (via Kaspa REST API server)

Silver Market Capitalization – CompaniesMarketCap

Methodology:

Kaspa’s total coin supply (stock) and current block reward (flow) were obtained from the Kaspa Network via the Kaspa REST API server.

Using these values, the exact time at which Kaspa’s S2F ratio would exceed silver’s estimated S2F of 22 was calculated using GPT-5.

Kaspa’s stock was not adjusted for burned coins; however, even with such an adjustment, the result remains essentially unchanged. With an adjusted coin supply, Kaspa’s S2F will still surpass silver’s on December 4, 2025, immediately following its block reward reduction.

Kaspa's Stock-to-Flow Ratio Just Surpassed That of Silver

At approximately midnight Eastern Standard Time on December 4, 2025, Kaspa’s stock-to-flow (S2F) ratio quietly crossed a historic milestone: it surpassed that of silver.

While a commodity’s S2F ratio does not directly determine its market capitalization, since many other factors influence fiat price action, if KAS were valued at the same aggregate level as the world’s above-ground silver, its price would be roughly $122 per KAS.

If one believes Kaspa to be the most advanced form of money ever devised, offering a ledger superior to silver or any other monetary commodity, then on what basis should we assume its market cap could never exceed silver’s?

Unlike gold and silver, Bitcoin and Kaspa are digital commodity monies that, for the first time in history, provide ledgers where the stock-to-flow ratio can be precisely measured and independently verified by anyone. In contrast, gold and silver rely on trust-based systems and remain vulnerable to coordination failures and information asymmetries.

In this respect, Bitcoin and Kaspa represent superior ledger technologies. They resolve the Byzantine Generals Problem, ensuring consensus without centralized trust.

By the end of this decade, Kaspa’s S2F ratio will exceed that of both gold and Bitcoin.

I completely agree that they could manipulate Kaspa’s fiat price, but would they really sell at $0.10 if they were buyers above that level?

It’s far more likely they’d wait for much, much higher prices before selling. And if the holder is Binance, there’s virtually no limit to how high they could drive the price.

With that said, no matter what this large holder does, they cannot control the Kaspa ecosystem; at best, they can manipulate the fiat price.

And if they do eventually sell, they’ll simply be making supply available to new adopters who are just then crossing the bridge into the Kaspa ecosystem. Selling KAS for fiat is ultimately just trading superior money for inferior "money".

Inactive supply metrics show that not only is Kaspa not a Ponzi scheme, but rather it is literally the most Ponzi-resistant ledger ever designed.

Any large holder who sells all of their KAS to new adopters will soon find themselves on the wrong side of history.

They would have erased the record of their wealth on the most unmanipulable, Ponzi-resistant ledger ever devised, only to record that wealth on a far more manipulable, Ponzi-prone ledger.

The holder of Kaspa’s largest address has created a supply shock. This holder’s continued accumulation of KAS is unsustainable, especially as demand from other market participants rises.

Kaspa’s supply shocks are likely to be extreme, due to its rapid emission schedule, completely inelastic supply, and strong tendency for rapid adoption as both a store of value and medium of exchange.

Wallet #1 Continues Aggressive KAS Accumulation

Over the past several months, the holder of Kaspa’s largest address (ending in m7n4uk5a, labeled “Wallet #1” in the animation) has been aggressively accumulating KAS.

This holder’s demand for KAS is so strong that even if every miner sold all newly mined KAS exclusively to them, it still wouldn’t meet their demand. They must therefore acquire some of their KAS from existing holders, not just from new supply.

Notice that Wallet #1’s net accumulation surged in the aftermath of the October 10 market crash. While some existing holders sold or were liquidated, Wallet #1 was aggressively accumulating.

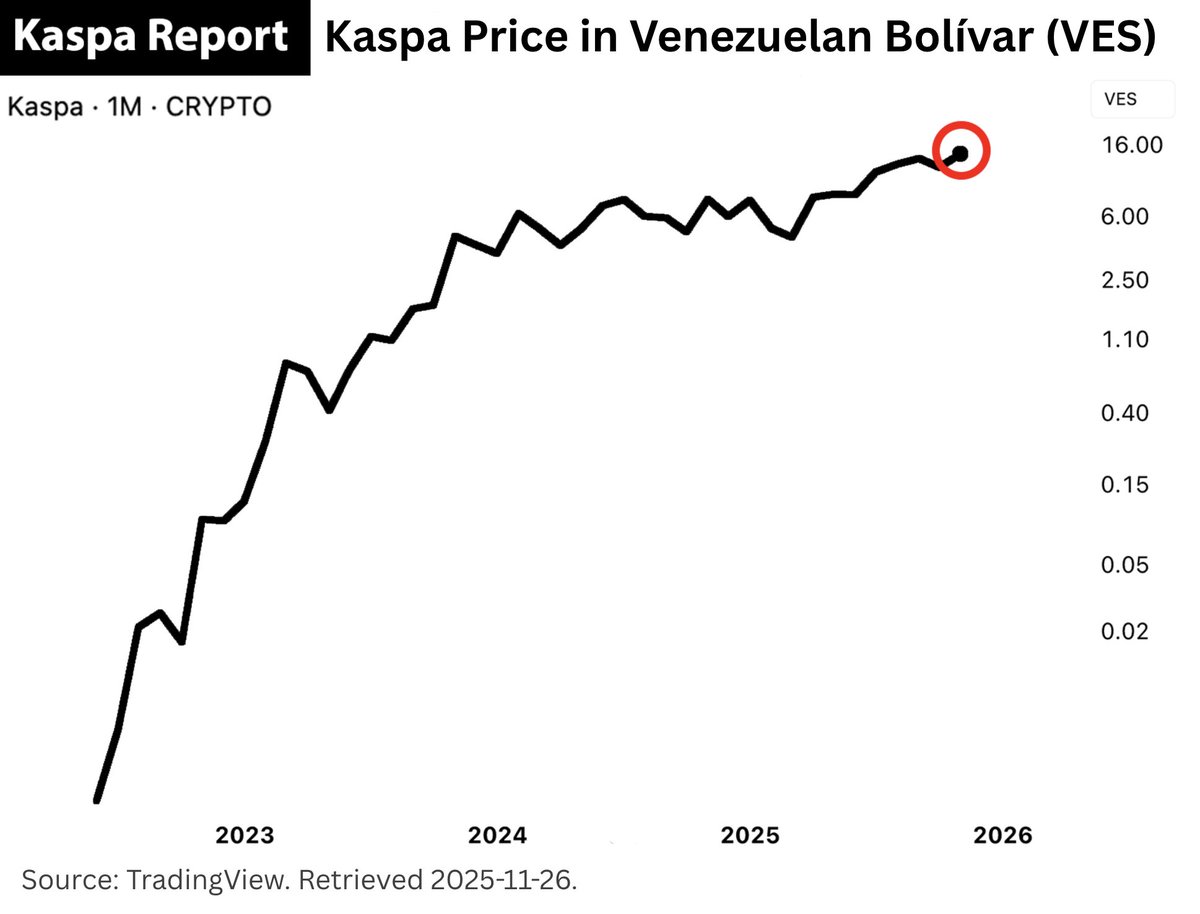

Kaspa hits new all-time high against the Venezuelan bolívar.

Although the Venezuelan bolívar (VES) is among the world’s fastest-devaluing fiat currencies, all fiat currencies will generally tend to depreciate against Kaspa in a similar way over time.

Interestingly, Kaspa’s power law model fits much better when Kaspa is priced in the Venezuelan bolívar: there is less deviation from the line of best fit than when priced in U.S. dollars or in fiat currencies effectively pegged to the U.S. dollar.

That tighter fit arises from two confounding factors that largely cancel each other out. First, the Venezuelan bolívar is suppressed against the U.S. dollar because Venezuela has restricted dollar access. Second, Kaspa is suppressed against the U.S. dollar by certain exchanges. These exchanges use many tactics to suppress Kaspa’s price, but chief among them is trapping long KAS exposure in USD stablecoins through Kaspa perpetual futures.

These two unrelated factors tend to suppress each currency against the dollar by a roughly similar magnitude, causing them to offset each other and leaving the KAS/VES price time series with a better power law fit.

This shows that the choice of unit (currency) for the dependent variable (Kaspa’s price) can materially affect the power law model’s explanatory power (e.g., R² value). It strengthens the case for using on-chain, hard-to-manipulate metrics to measure Kaspa’s monetary value.

Inactive supply is harder to manipulate and better reflects Kaspa’s use as a store of value—a core function of money—making it a more reliable indicator of Kaspa’s monetary value than any single fiat currency price time series.

Setting legal considerations aside, it’s possible. But if true, it would suggest that a third party — not Grayscale — controls the Kaspa, since the coins came from an exchange Grayscale was restricted from using and were never moved out of that wallet. It also wouldn’t really make much sense for Grayscale to source KAS primarily from an exchange they weren’t allowed to do business with when other exchanges were available. There is nothing currently preventing Grayscale from acquiring KAS from American exchanges and/or miners. As far as I know, this address has never sourced KAS from an American exchange.

Wallet #1 Continues Aggressive KAS Accumulation

Over the past several months, the holder of Kaspa’s largest address (ending in m7n4uk5a, labeled “Wallet #1” in the animation) has been aggressively accumulating KAS.

This holder’s demand for KAS is so strong that even if every miner sold all newly mined KAS exclusively to them, it still wouldn’t meet their demand. They must therefore acquire some of their KAS from existing holders, not just from new supply.

Notice that Wallet #1’s net accumulation surged in the aftermath of the October 10 market crash. While some existing holders sold or were liquidated, Wallet #1 was aggressively accumulating.

@BlossomsRare@CryptosDawn@Grayscale In short, the holder is unlikely to be a U.S. company because we know that the address has been receiving funds from an exchange that’s restricted in the United States.

Abandon the idea of taking profit from Kaspa at a specific price target, since doing so would mean exchanging superior money for inferior money. Instead, transform your understanding of money: aim to spend only what you need and use KAS to store remaining value.

Based on my research, I do not believe this wallet belongs to Wintermute, though I acknowledge it remains a possibility.

First, we know this wallet has transacted with Gate io, something Wintermute would likely be restricted from doing under the regulatory frameworks they operate within. Second, it’s difficult to view this address as belonging to any liquidity provider, as it does not appear to source assets directly from miners or mining pools, which is generally what we would expect from liquidity providers of a proof-of-work cryptocurrency. In fact, on a net basis, this address has been removing a substantial amount of liquidity from exchanges rather than supplying it.

That said, it’s important to acknowledge that it’s impossible to conclusively determine who controls any given Kaspa address unless the holder takes explicit action to prove ownership, and even then, such proof only establishes control at that specific moment in time.

They’re effectively the opposite of a liquidity provider: over the past 18 months they've removed roughly 1.2 billion KAS from the ecosystem. As a result, the market has become more illiquid due to this wallet’s accumulation and is now far more vulnerable to a significant supply shock.