@_rob_anderson@NDR_Research Phenomenal chart. Curious if you have run the same analysis for SMID caps. Feels even more extreme in that part of the market.

@TheStalwart Difference is equity value v. borrower ability to repay. Software equity declines are due to re-pricing of terminal value. Current software fundamentals likely protect lenders over the duration of these loans. Inevitably some software cos will be disrupted causing charge-offs

This was actually published: "Following the success of PLTR & Anduril using names from JR Tolkien, imagine the multiple this newly listed business might garner if it were named something like Thorondor or Ancalagon the largest & most powerful dragon in the history of Middle-earth

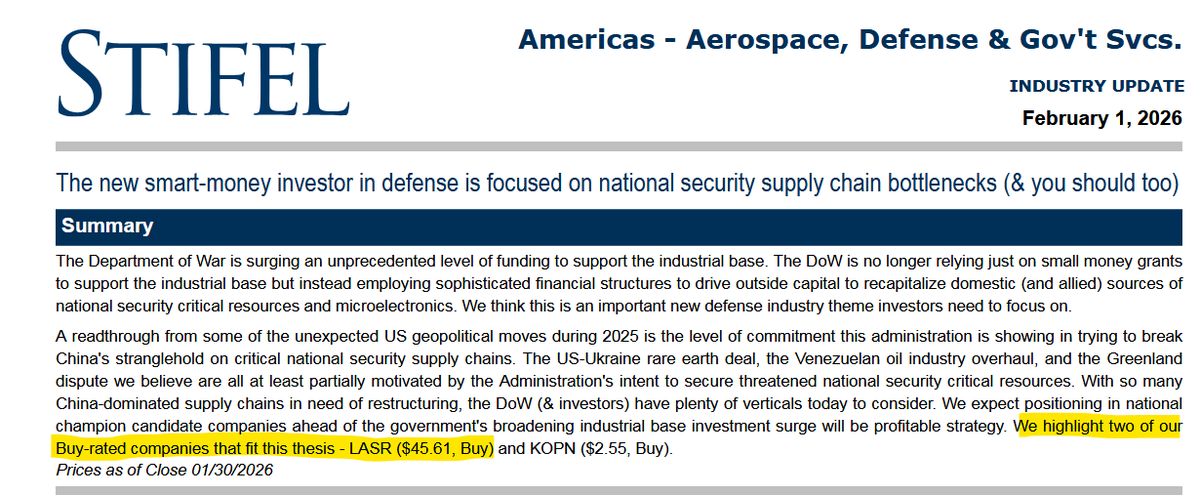

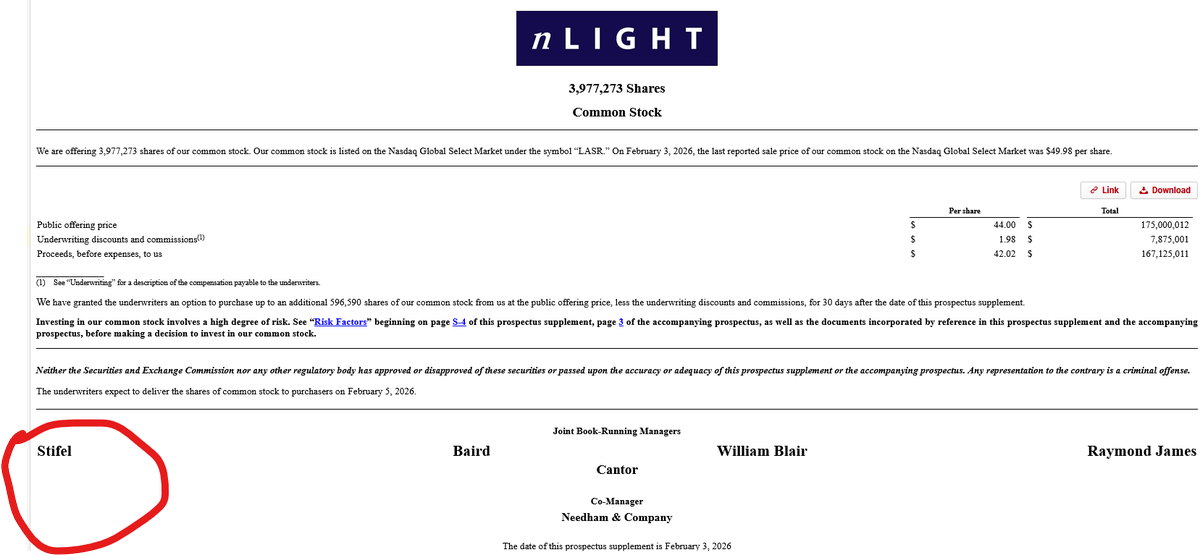

This one of the worst sell side reports I have ever read. Nothing of value, honestly wasn't sure why it was published. But they wanted to highlight $LASR. Next day... equity raise led by Stifel. Shameless

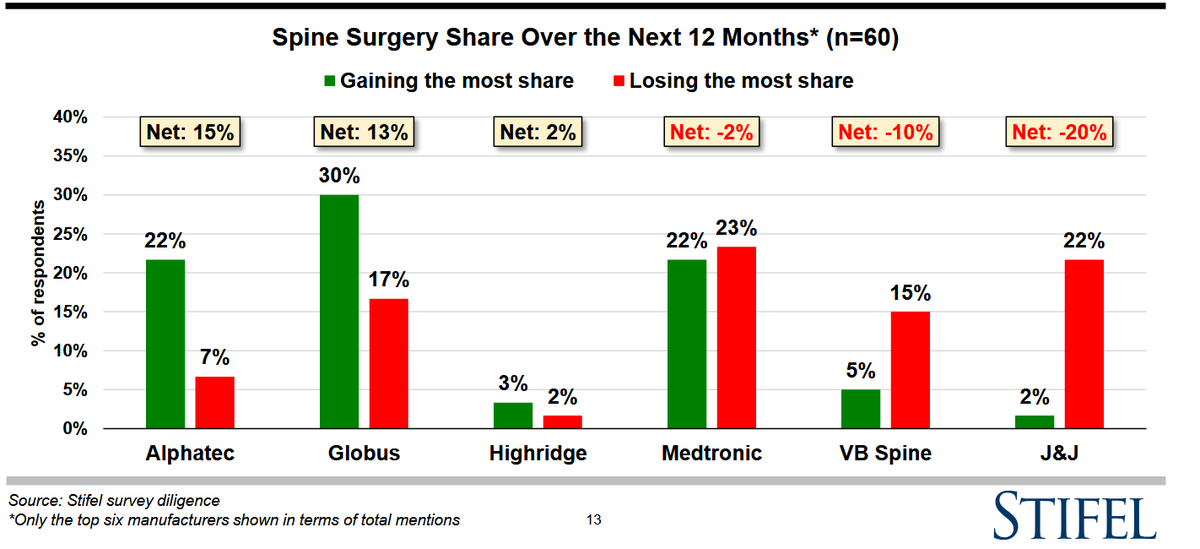

$GMED Aaand here come the upgrades. Yesterday: spine is terrible, structural loser. 8x EBITDA. Hold. Today: HSD rev grower, high teens EPS compounder. $91 PT (+50% from yesterday's price) Not expensive at 12x EBITDA. BUY.

$GMED Structural share gainer thanks to innovation (robotics) and comprehensive product portfolio. Growing HSD, 30-35% EBITDA margins depending on assumptions for timing of synergies. Net cash position. Printing cash. HOLD rating at 8x EBITDA. Thanks sell side.

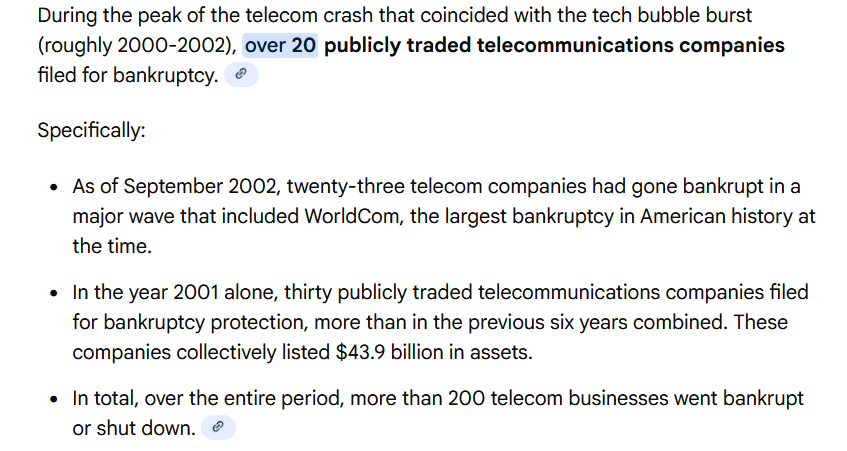

@BenBajarin Semantics. Tell this to railroad and telco investors. It's still a capital cycle that will ultimately lead to over-investment and poor returns on capital.

@WarrenPies I think this is more related to $ORCL earnings release on 9/9 when they announced the $450B OpenAI deal. Lower yields just fuel to the fire of AI capitulation by all fund managers after the ORCL announcement

Cyclical industrials getting tech valuations. Applaud this management team for taking advantage by raising capital, but what does this imply for future equity returns? And if they deploy this capital into similar high multiple businesses that are over-earning?

One of the more interesting set-ups that I think will play out over the next 6 mos is $ICFI. Market is laser focused on the company's Fed Civ business, which has been torpedoed by DOGE. But market is missing growth in their commercial energy consulting biz. It's a sneaky AI play

While the market has correctly focused on the risk to Fed Civ revs, it has missed the success $ICFI is having in energy consulting. As Fed Civ rev concentration declines, this headwind to top-line growth should abate, leading to investor focus on commercial energy growth

@SouthernValue95 It's definitely already occurring. The Oracle announcement was the catalyst. TBD on duration. Reactions to hyperscaler CAPEX will be interesting, but it "feels" like there is more gas in the tank for this divergence 😔

Does anyone have this chart/data from pre-Trump (maybe summer of 2024)? Would love to see how it has changed to see if we have actually stimulated manufacturing activity. @Borlaug_ post earlier today got me thinking more about this

@WTCM3 Maybe not to these extremes, but this is every part of the market that isn't benefiting from AI. Multiple compression overwhelming any EPS growth.