Interestingly, one could say that ending QT completely could be akin to a rate cut of sorts, and then re-starting QE could serve as another.

Our advice is to stay tuned and try not to get too caught up in the day-to-day headlines and tweets that are out there because this is going to be a very fluid situation

Remember, the key here is for financial and non-financial companies to be able to fund themselves. While there has been some tightening up in conditions in recent trading sessions, there is not any sign of worrisome funding pressures at this point.

some thoughts on the Treasury market turbulence...i think it's a confluence of factors all coming together...reversal of the flight-to-quality rally, resulting in bets it would continue to be unwound, selling to raise cash (reversal of the basis trade)...NOT active retaliation by China. They hold too many Treasuries hence it would be counterproductive (losses)...Japan and China have been reducing UST holdings over the last year but it is orderly and rates still fell at times during this period

if it got to the point of creating 'plumbing' issues in the funds market, the Fed could stop QT in Treasuries altogether and start to re-buy (QE)...they wouldn't necessarily have to cut rates

I read a story where some one asked: if the US raising tariffs produces recession fears and higher inflation concerns for the US, then wouldn't the same potential results apply to countries/regions that impose retaliatory counter/tariffs, i.e. raises there existing tariffs, like the EU?

Chart of the week...Rip Van Winkle woke up from his nap starting on pre-election Day and said: Oh , the UST 10-yr yield hasn't changed at all...what's all the fuss?

what else did we learn this week? The Treasury 10-yr yield has already discounted the potential for reduced economic growth (not a recession) and has also been supported by ‘risk-off’ sentiment, while arguably ignoring tariff-induced inflation probabilities…validation of the rally will be required at some point yet again

what did we learn this week? it appears as if the Fed's concerns surrounding potential adverse impacts on the economy from tariffs may be modestly outweighing the potential effects on inflation…the Fed Chair actually revived the word “transitory” to describe possible tariff-induced price pressures

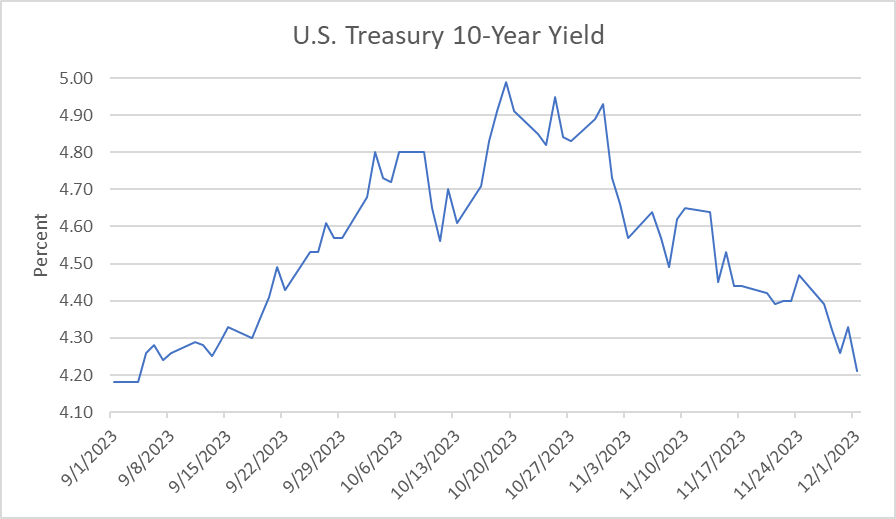

The recent rally in Treasuries has been one for the ages. The UST-10yr yield plummeted nearly -90bp in the process. Now the key question was: would such a move be validated? Based on the November jobs report, the first test to this rally, the answer is no.

i never really thought Powell's presser last week was as 'dovish' as portrayed...what was he gonna tell the bond market 'you've got it all wrong'...now markets are looking squarely at a 5-5.25% fed funds rate

Powell, paraphrased: Despite many people believing (or hoping) the Fed's recent inflation projections were too high because inflation would come down faster, the Fed didn't see it that way and, given last week's job report, still doesn't.

so Mr. Powell, is there anything bothering you? Well, yes there is...I've raised rates 350bp since May and financial conditions are right back where they were then...

The Fed has never hiked their Fed Funds rate past the level of 2y Treasury yields.

The widely expected 50 bps hike in December will basically get us there

Any additional hike in 2023 will push us through uncharted territory from this point of view.