$UMC $2303 UMC: Scarcity Premium and the Mature-Node Resurgence. Investment Thesis.

UMC has moved beyond the standard foundry recovery narrative and is beginning to attract attention as a scarcity asset — a characterization that reflects both the strategic repositioning underway and the broader market recognition that specialty node capacity is not easily replicated. The shift toward 22nm and 14nm specialty nodes moves UMC away from commoditized legacy production and toward a more defensible position where technical qualification requirements and customer switching costs create pricing durability that generic wafer volume cannot support.

The Intel manufacturing partnership is the most strategically significant recent development. It extends UMC's technological reach and geographic relevance without requiring the kind of capital commitment that an independent leading-edge buildout would demand. In an environment where geopolitical supply chain resilience is an active customer priority, that partnership adds a dimension to UMC's value proposition that pure process technology comparisons don't capture.

The exploration of AI-adjacent packaging and silicon photonics is worth monitoring as a longer-term optionality story. Neither is a near-term revenue driver at scale, but both represent logical adjacencies for a foundry with specialty node expertise and a customer base increasingly focused on heterogeneous integration. The trajectory of those initiatives will indicate how seriously UMC is investing in the transition versus using them as narrative support.

Utilization rates are improving and operational momentum is genuine. The financial foundation is solid. The concern is entirely in the valuation. The year-to-date rally has pulled forward a significant portion of the fundamental upside, and the current share price appears to embed a best-case scenario that requires sustained pricing power, continued utilization improvement, and ongoing earnings beats to justify. That is a demanding setup in a cyclical industry where demand visibility beyond a few quarters is inherently limited.

The business is genuinely improving and the strategic direction is credible. The investment question is not whether UMC is a better company than it was — it clearly is — but whether the current entry point leaves sufficient upside to compensate for the execution requirements now embedded in the multiple.

🚨 عاجل وخطيير

🇺🇸 عم بيحقن الاحتياطي الفيدرالي 7,585,000,000.00 دولار في الأسواق بكرا الساعة 9 الصبح بتوقيت الشرق الأمريكي، قبل ما يفتح سوق الولايات المتحدة!

وها هي آلة طباعة الفلوس عم تشتغل على مدار الساعة لتحفيز الاقتصاد وسط أزمة النفط!

اللي عم بيصير هلق شي ما صار من قبل… الوضع بديع!

a man raised $4.2B from crypto investors, bought 164,000 Bitcoin at $6,000 with their money, and IPO'd a $10B company

and investors got nothing

be @BrendanBlumer

- CEO of Block(dot)one

- the company behind EOS

- ran the biggest ICO in crypto history

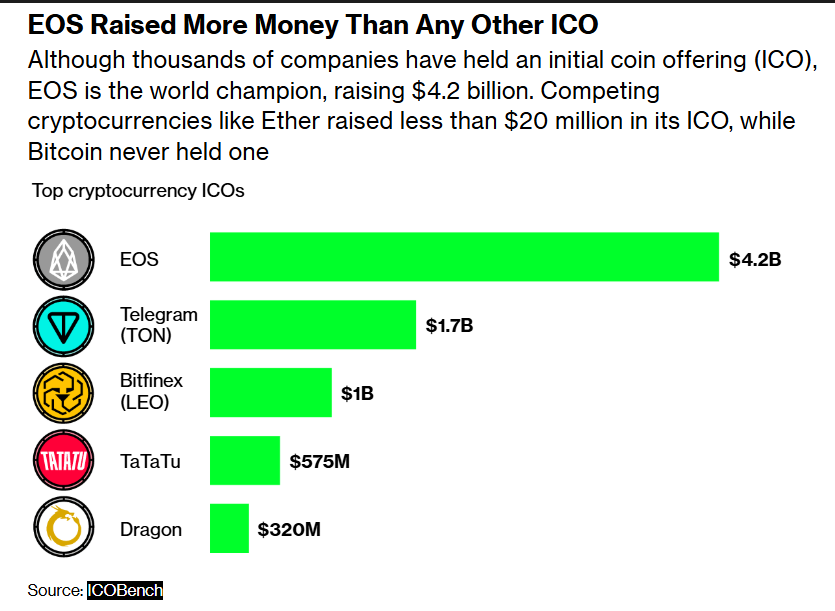

June 2017 to June 2018

- Block(dot)one ran a year long ICO for EOS tokens

- raised $4.1 billion in ETH from retail investors

- biggest ICO ever at the time

- money went straight to Blockone not the EOS chain

- Cayman Islands company

everyone thought they were funding the next Ethereum killer

they were funding Brendan's Bitcoin bag

heres what he actually did with the money

- crypto winter hit in 2018

- BTC crashed to $3,200

- while everyone was panicking Brendan was buying

- converted a massive chunk of the $4.1B into Bitcoin

- bought around the $6,000 level

- accumulated 164,000 BTC

- at $6K thats roughly $1 billion spent on BTC

- put the rest in US government bonds

by 2021 that 164,000 BTC was worth $10,000,000,000

read that again. he turned investor money into a $10B Bitcoin treasury.

the SEC came knocking

- fined Blockone $24 million for unregistered securities

- thats 0.6% of what they raised

- nobody had to give money back

- Brendan paid it like a parking ticket

then he built Bullish

- a crypto exchange seeded with his Bitcoin stash

- put in 164,000 BTC

- put in $100M cash

- put in 20M EOS tokens

- got Peter Thiel, Mike Novogratz, and Nomura to invest $300M more

- hired Tom Farley the former NYSE president as CEO

- total starting balance sheet: over $10 billion

August 2025

- Bullish IPO'd on the NYSE

- ticker: BLSH

- raised $1.1 billion at $37 per share

- shares surged 84-160% on day one

- closed around $68-70

- market cap instantly hit $10 billion+

Brendan owns 26-30% of Bullish after the IPO

he is now a billionaire

meanwhile EOS investors

- Block(dot)one promised to invest $1B back into the EOS ecosystem

- most of the money went to BTC, bonds, and Bullish instead

- EOS the token massively underperformed

- Blockone quietly stepped away from the project

- the community felt completely betrayed

- lawsuits and class action settlements are still ongoing

this is the greatest finesse in crypto history and its not even close

bookmark this to read it twice