In 5 years, $AVGO exploded 1000% from $47 to $470+

Tonight will be $AVGO biggest earnings in history.

I'm bullish on it and here's why:

1. AI Revenue Is About to Print the Biggest Single-Quarter Number in Broadcom's History

The guided number was $10.7B in AI chip revenue for Q2. That is not just a beat setup, it is a structural acceleration. Q1 came in at $8.4B and already beat expectations. If tonight prints $11B or higher, that is 140%+ YoY growth on a base that is already massive. For context, Broadcom did $4.4B in AI revenue just two quarters ago. The market will reprice the entire forward earnings curve in one session. A number above guidance at this scale does not get a polite reaction. It gets a gap.

2. The Q3 Guide Is the Real Catalyst, Not Q2

Every sophisticated trader knows tonight is about Q3 guidance, not the print itself. If Hock Tan walks onto that call and guides Q3 revenue toward $24-25B with AI chip revenue above $12B, the stock re-rates immediately. The $100B AI revenue figure he cited for 2027 becomes a straight-line extrapolation the market can finally model with confidence. Institutions that have been waiting on the sidelines for a clean entry point will not wait for a pullback. They chase.

3. Dealer Hedging Creates a Mechanical Bid That Cannot Be Stopped

The options market is loaded. Call volume is running nearly 2:1 over puts with a 0.46 put/call ratio. AVGO is already trading in the positive gamma extension zone above C1. The moment the stock gaps up on earnings, every dealer who sold calls into this print is forced to buy shares to stay delta-neutral. That buying pushes price higher, which forces more buying. It is not sentiment driven at that point. It is mechanical. The gamma squeeze feedback loop on a $400+ stock with this much open interest can add 3-5% on top of whatever the fundamental move is.

4. The $MRVL Read-Through Just De-Risked the Entire Custom Silicon Thesis

$MRVL reported last week and exploded 25%+. Their custom AI silicon business confirmed that hyperscaler demand for custom accelerators is not slowing, it is accelerating into the second half of 2026. Broadcom is the largest custom silicon player on the planet with more hyperscaler customers than anyone. $MRVL just told the market the cycle is real and durable. When the sector leader reports into a tape where the second-largest player just validated every bull thesis, you do not get a quiet reaction. The $MRVL print is the pre-game show. $AVGO is the main event.

$AVGO if they beat will do $DELL and $HPE explosion move.

♻️ RESHARE this post and write 1 comment, I'll DM you my exact play for $AVGO earnings tonight.

JENSEN HUANG DOING IT AGAIN

IN TAIPEI, HE SAID THESE STOCKS ARE THE FUTURE:

$NOW — AI agents run inside ServiceNow's enterprise software stack

$CRWD — Security layer every AI factory must have running

$PLTR — Turns AI agent outputs into real government/enterprise decisions

$MSFT — Co-built the entire agentic PC platform with Jensen

$TSM — Only company on earth that can build these chips

AND HE HAS A DEAL WITH THESE ONES:

$HPE — Builds and ships the physical AI factory server infrastructure

$IREN — Owns the cheap power AI factories are desperately hungry for

$CRWV — The cloud Jensen personally called out by dollar valuation

$ARM — Every AI chip on the planet runs on ARM architecture

$DELL — First to rack and deploy Vera Rubin in production

$NVDA STILL SUPER EARLY SO DON'T MISS IT!

♻️ RESHARE this post and write 1 comment, I'll share my $HPE earnings play with you. It's tonight.

Noone is focused on $HPE earnings this week.

In 1 month, $HPE spiked 125% from $20 → $45.

Earnings is exactly like $DELL:

• Revenue expected to surge 28% YoY to $9.77B one of the biggest growth quarters in HPE's history

• Networking revenue already exploded 152% YoY in Q1 Juniper acquisition turned HPE into an AI networking powerhouse

• Data center networking revenue specifically up 382.6% the AI buildout has found its backbone

AI backlog crossed $5B and 64% of orders are enterprise/sovereign, NOT hyperscalers. That's durable, diversified demand

• HPE raised full-year EPS guidance to $2.30–$2.50 and lifted networking revenue growth target to 68–73%

• Networking operating margins hit 23.7% in Q1 if that holds tonight, this stock re-rates immediately

• Q3 is expected to be the biggest AI revenue quarter tonight's print is just the setup, not the peak

• HPE has beaten EPS estimates 88% of the time and revenue 75% of the time the base rate is on the bull's side

♻️ RESHARE this post and write 1 comment, I'll DM you my exact play for $HPE just like $DELL.

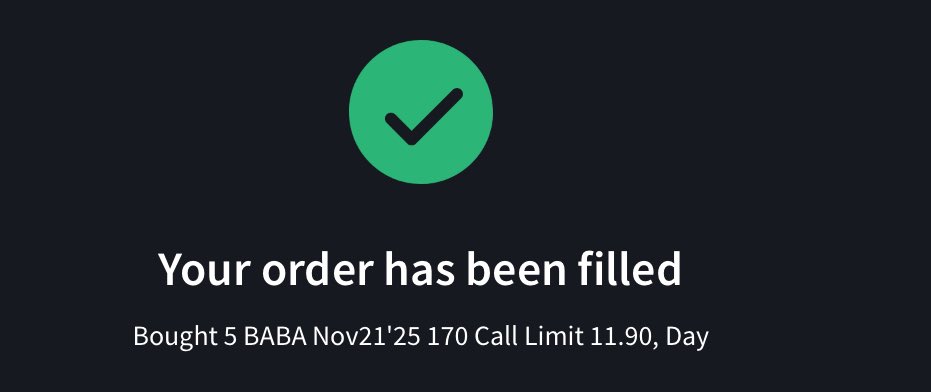

Yesterday, $DELL spiked 45% after its Q1 earnings.

Options exploded 20000%-30000% in 1 day (rare).

Next week, there's 4 earnings with exact same set-up:

1. $CRWD 📅 Earnings: June 3 (After Close)

As enterprises deploy thousands of AI agents, cloud workloads, and connected endpoints, the security perimeter expands infinitely, making Falcon's AI-driven threat detection not optional but mandatory.

No one builds a $500B AI datacenter and skimps on security. $CRWD is the toll booth on the AI buildout highway and that moat compounds with every new customer and dataset feeding its threat intelligence engine.

Target: $800 median | $700 Wedbush & Benchmark | $750 Oppenheimer

2. $AVGO 📅 Earnings: June 2 (After Close)

Custom AI chip (XPU) demand from hyperscalers accelerating every quarter. $AVGO is the silent infrastructure backbone of the AI supercycle.

While $NVDA dominates training, Broadcom owns the custom silicon layer designing the XPUs that $GOOG, $META, and Tiktok use to run inference at hyperscale, plus the networking chips that stitch datacenters together.

As hyperscalers race to reduce $NVDA dependency and build proprietary AI chips, Broadcom is the only company with the design expertise and manufacturing relationships to deliver.

Target: $500 avg | $480 Susquehanna | $560 high

3. $PANW 📅 Earnings: June 2 (After Close)

Platformization strategy converting AI security budgets into sticky, recurring revenue.

AI doesn't just create new threats it supercharges existing ones, making next-gen cybersecurity a non-negotiable line item for every enterprise on the planet.

PANW's platformization strategy is purpose-built for this world: one unified platform replacing dozens of point solutions, with AI models running across network, cloud, and endpoint security simultaneously.

Target: $320 avg | $340 high | $300 median (75 analysts)

4. $GTLB 📅 Earnings: June 2 (After Close)

AI-native DevSecOps platform controls full dev lifecycle as code volumes explode.

AI is going to produce more code in the next five years than humans wrote in the last fifty and all of it needs to be managed, secured, and deployed somewhere.

While competitors like GitHub Copilot focus on code generation, GitLab controls the entire pipeline and that becomes more valuable, not less, as AI-generated code volumes explode.

Target: $40 median | $60 high (Macquarie) | $27 low (Cantor)

$ORCL earnings is on June 10 and $MU is on June 24. These will explode like $DELL did most likely.

♻️ RESHARE this post and write 1 comment, I'll DM the best $MU contract to get for earnings right now.

It's 2035, you're a millionaire, you did exactly this in June 2026:

1. Open up a ROTH IRA (or tax-free savings account)

2. Buy stocks Trump is telling you to buy when he says it (not after it spikes)

- $NOW $85 →$400+

- $DELL $235 → $800+

- $MU $320 → $3000+

- $IBM $220 → $600+

- $INTC $20 → 400+

*these are going a lot higher by 2035 just like $NVDA $AAPL $GOOG $TSLA $AMZN $MSFT

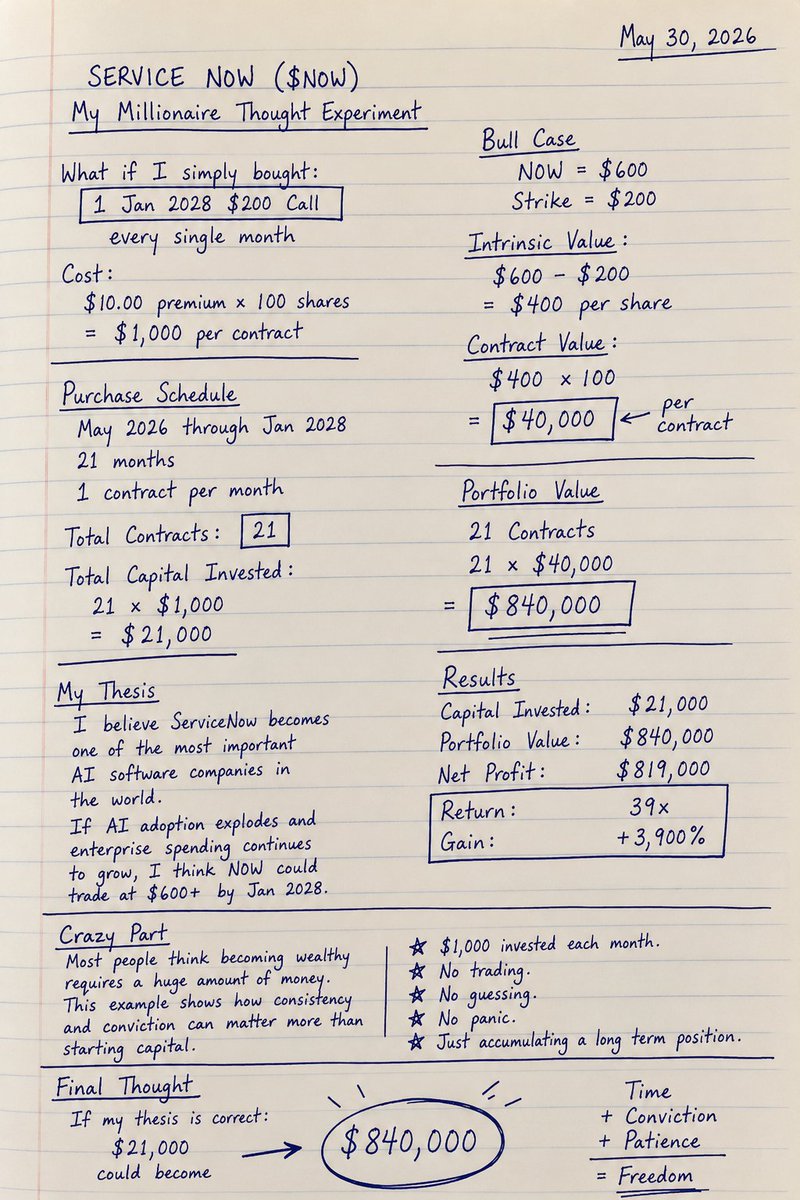

3. BUY LEAPS example $NOW buy Jan 2028 $200 calls.

4. OR just put $500-$1000 bucks into $VOO $QQQ each month (safest)

5. Be patient, keep it boring and simple.

♻️ RESHARE this post and write 1 comment, I'll DM you what LEAP to buy for each of these. Then do nothing, just buy and hold it.

$NOW can easily triple from $125 by Jan 2027.

Remember, token use is expected to 2800% in 5 years says $GS.

So these 24 stocks can still 10x-20x:

(COMPUTE / GPU)

1. $NVDA — Every token touches a GPU. 24x tokens = 24x chip demand, full stop.

2. $AMD — MI300X gaining enterprise traction. Second GPU source as hyperscalers diversify suppliers.

3. $INTC — Gaudi AI accelerators + x86 CPUs running inference at the edge and enterprise.

(NETWORKING)

4. $ANET — AI clusters need ultra-low latency switching. 24x tokens = 24x network traffic routed.

5.$AVGO — Custom AI ASICs for hyperscalers. Token volume drives ASIC and switching orders higher.

6. $CSCO — Data center fabric and ethernet switching. Every agent call crosses Cisco infrastructure.

7. $CIEN — Optical networking backbone connecting AI data centers. Bandwidth demand scales with tokens.

(MEMORY / STORAGE)

8. $MU — HBM3E stacked on NVDA GPUs. More inference = direct memory bandwidth demand explosion.

9. $WDC — Flash storage holds model weights and KV caches. Agent scale drives NAND demand structurally.

10. $STX — Hard drives store cold AI training data. Data center storage TAM expands with every model.

(POWER / COOLING)

11. $VRT — More tokens = more heat. Liquid cooling demand explodes alongside data center power density.

12. $ETN — Electrical infrastructure for AI data centers. Power management is the #1 buildout bottleneck.

13. $GEV — Gas turbines and grid solutions powering new data center campuses requiring gigawatt-scale energy.

14. $VST — Power generator selling directly to hyperscalers. AI energy contracts already locked in long-term.

(CLOUD PLATFORM)

15. $MSFT — Azure hosts majority of enterprise agents. Token spend flows straight through its cloud margin.

16. $AMZN — AWS Bedrock is the enterprise agent backbone. More agents, more API calls, more revenue.

17. $GOOGL — TPU infrastructure + Gemini API. Every token processed on Google Cloud prints margin.

(ENTERPRISE AGENT LAYER)

18. $NOW — Enterprise agents run on its platform. Every workflow automated burns more tokens daily.

19. $CRM — Agentforce deploys AI agents across sales, service, and marketing. Per-action token billing scales.

20. $PLTR — AIP platform runs AI agents on enterprise and government data. Token volume is its revenue driver.

(AI INFRASTRUCTURE)

21. $NBIS — Pure-play AI infrastructure at ground level. Token supercycle lifts the entire compute ecosystem.

22. $SMCI — Builds GPU server racks for data centers. Every NVDA chip needs a SMCI chassis to run.

23. $DELL — AI server sales to enterprises exploding. Token growth drives hardware refresh cycles faster.

24. $ARM — Chip architecture inside every mobile and edge AI device. Royalties scale with token proliferation.

$NOW is the most undervalued right now. This is why Jensen Huang says the market has made a mistake on it.

♻️ RESHARE this post and write 1 comment, I'll DM you the best $NOW contract to buy and hold.

2 years ago, I called out $ASTS at $2. Its up 6500% so far at $130.

My target at least $200+ when $SPCX IPOs.

Right now, $ORCL is the most obvious play. Its earnings is on June 10 then $MU on June 24.

This year, I explained these would 10x-20x:

$INTC — $AAPL chip deal + foundry turnaround tripled the stock in months (Trump)

$DELL — Pentagon contract + AI server orders created a multi-catalyst monster (Trump)

$MU — HBM memory sold out through 2026, AI supercycle just getting started (Trump)

$NOW — Enterprise AI agents replacing entire IT workflows, 22% revenue growth accelerating (Trump)

$PLTR — Government + commercial AI contracts exploding, revenue up 56% in 2025 (Trump call)

$TE — nuclear power is the only answer to AI's insatiable electricity demand (Leopold call)

♻️ RESHARE this post and write 1 comment, I'll DM you my exact 1000% play for $ORCL

You could but it doesn't always appear. As mentioned on the screenshot the small downcandle on low vol is already suggesting the selling pressure has abated.