We’ve been solving the wrong payment problem in crypto for a long time.

For most companies that already accept crypto, payments are not the bottleneck anymore.

Speed is fine.

Fees are tolerable.

Stablecoin settlement works.

$USDC and $USDT already move globally. They settle faster than cards, cheaper than wires, and they do not care about borders. For one off payments, the rails exist.

So when I look at many crypto payments products, I keep asking one question.

What changes for a business after integrating this?

Most products stop at accepting crypto. But accepting crypto is table stakes.

The real pain starts after the payment lands.

The real friction is not checkout

It is what happens next

If you run a SaaS product, an API, an infra service, or any recurring revenue business, you already know the usual problems.

❌ Subscriptions fail because cards expire or hit limits.

❌ Global pull payments are still hard.

❌ Renewals become a manual process.

❌ Reconciliation becomes operational glue.

❌ Treasury sits idle between cycles.

Crypto was supposed to improve this. In practice, many tools just replaced Stripe with a wallet address.

That does not change the economics.

Why crypto payments still feel manual

Most crypto payment tools fall into three buckets.

Push only payments: The user signs a transaction every time. Fine for invoices. Not for subscriptions.

Prefunded escrow models: Users lock funds upfront. Capital inefficient and painful for cash management.

Card based wrappers: Crypto goes in, fiat logic comes out. You inherit delays, opacity, and fee layers.

All of them miss the same thing.

Businesses do not just need to receive money. They need money to repeat reliably.

That is not a checkout problem. That is an orchestration problem.

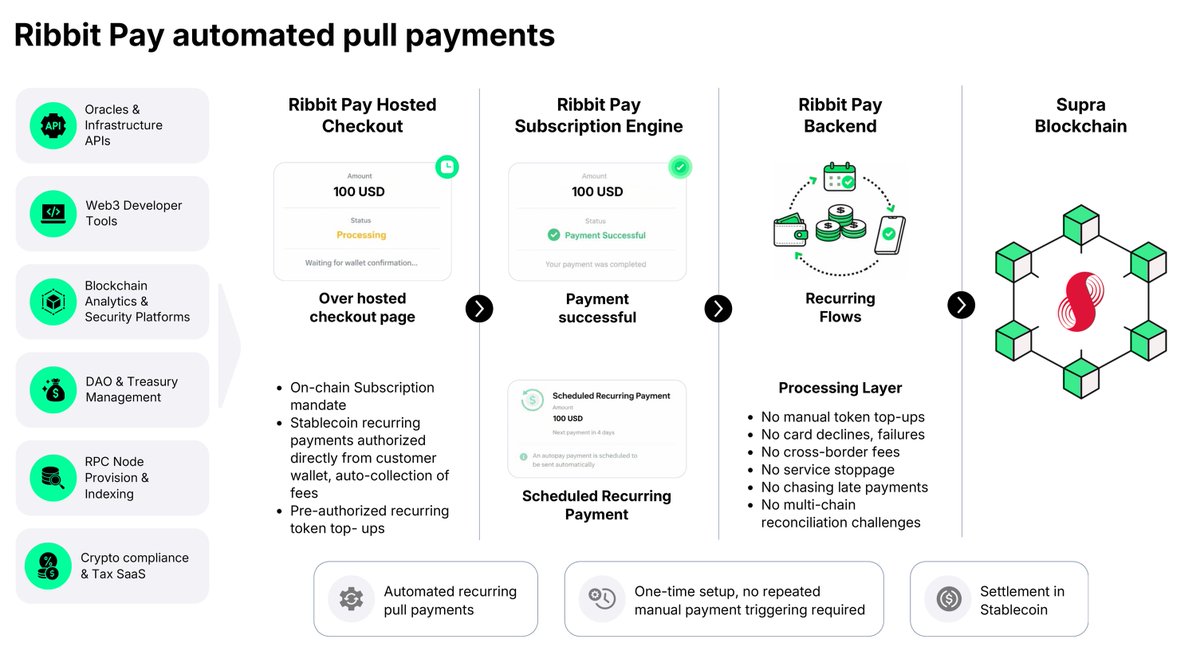

@RibbitWallet was not built as a wallet It was built as a payments orchestration layer

Ribbit does not start with “How do we help users pay with crypto?” It starts with “How do we make money programmable across time and obligations?”

That shift matters. Because once you stop thinking in transactions and start thinking in flows, new primitives become possible.

Pull payments rebuilt onchain Pull is the primitive that makes subscriptions work.

In traditional finance

⚫️ Cards pull funds.

⚫️ Direct debit pulls funds.

⚫️ Subscriptions depend on pull.

In crypto

⚫️ Everything is push.

⚫️ Or custodial.

⚫️ Or fragile automation.

Ribbit introduces onchain mandates.

How pull works in Ribbit

A user signs a mandate once.

For example up to 500 dollars per month for Company X.

That mandate lives onchain.

It is enforced by contracts, not by a processor.

On each billing cycle

Funds are pulled automatically.

The flow settles deterministically.

No card expiry.

No repeated approvals.

No renewal chasing.

For businesses, this feels like direct debit but global and self custodial.

For users, it feels invisible. Which is how payments should feel.

Pull improves reliability But the bigger unlock is what happens between cycles

Once you have reliable recurring execution, the next question is simple.

What is the money doing before it is pulled.

This is where Ribbit diverges from most payment products.

✅ Yield to pay: Turning treasury into a payment engine

Most businesses treat payments and treasury as separate systems.

Money arrives.

It sits.

It waits to be used.

Ribbit is built so funds do not have to sit idle by default.

Yield to pay, in simple terms

Balances can be routed into yield generating strategies.

Yield is earned continuously.

Obligations can be serviced using yield first.

Principal is used only if needed and only if permitted.

The goal is not to chase yield. The goal is to reduce waste.

A subscription model today

You charge 1,000 per month.

You pay fees.

Cash sits idle between cycles.

Treasury yield goes to banks and processors.

A subscription model with Ribbit

You charge 1,000 per month.

Settlement is native and programmable.

Yield can offset costs over time.

Payment operations become lower touch.

Same revenue.

Same customers.

Less value leaking through the system.

What Ribbit is and what it is not

Ribbit is not a card wrapper.

Ribbit is not a neobank.

Ribbit is not a DeFi frontend.

Ribbit is a coordination layer between

Recurring payments

Treasury routing

Execution and settlement

Event based reconciliation

Who this is for

Ribbit is not for everyone.

It is for teams that already have stablecoin flows and want them to behave like real subscription infrastructure.

Crypto native SaaS.

Infra companies billing globally.

API and data platforms.

Marketplaces with predictable repeat flows.

If you already accept crypto, Ribbit is not asking you to believe in anything new. We are asking one question.

"Why should your money stop working just because it is waiting?”

Most payment tools help you move money.

Ribbit helps you coordinate money across time and obligations.

Once you experience subscriptions that do not fail and payment operations that do not require constant manual glue, going back feels less like caution and more like leaving value on the table.

🚨 @SolidoMoney has brought a Supra AutoVault Framework (SAFV) to the $SUPRA ecosystem...

"A new construction standard for issuing strategy-backed on-chain assets on @SUPRA_Labs AutoFi"

Discover what it is, why it matters, and how it lets users build strategies that trade themselves.

Read now ⬇️

https://t.co/qofSVYuMV7

$SUPRA has been in a persistent downtrend with heavy drawdown.

Early supporters are taking the hardest hit.

The team should urgently address market confidence, communication, and pursue major exchange listings.

Silence at this stage only increases uncertainty.