PVC Nov 2025 futures break below $4,600!

With PMI surging to 67.1, it signals stronger construction demand.

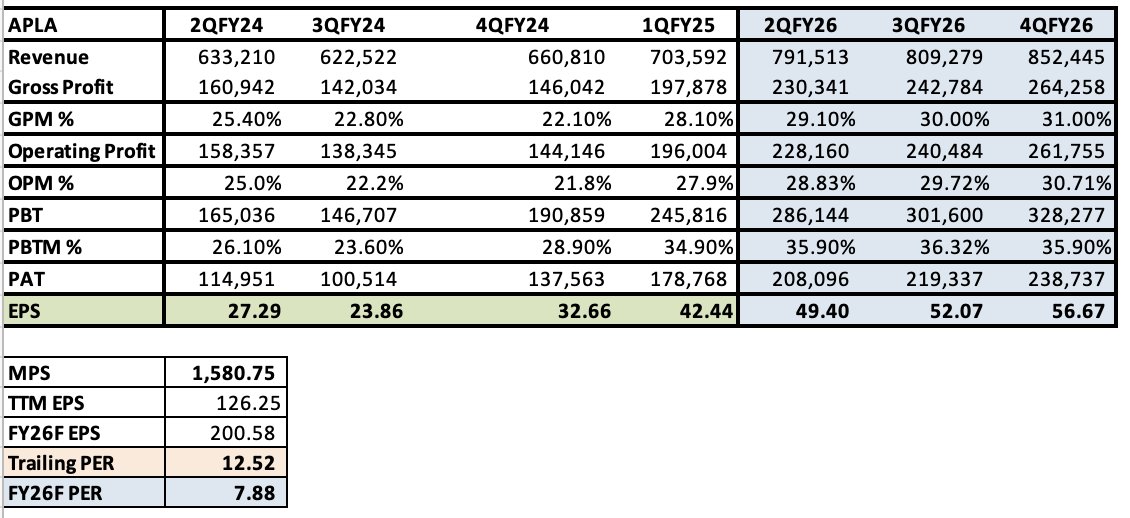

Macro setup for #APLA looks strong given the expected improvement in GPM and increase in capacity utilisations.

With the split boosting liquidity, is a rerating next?

PVC prices down 12.4% since July& 6.8% since 1QFY26.#APLA & #CIND GPMs should keep improving in 2Q–4QFY26F,as oil prices fall & PVC cost lowers.With rising cable demand & #APLA supplying all PVC required by #KCAB#ACL along with the split,can we expect more price action on #APLA?

@hareshdesoysa With demand rising for #ACL#KCAB products, #APLA should benefit from stronger volumes.If crude settles at $55–60, PVC resin could ease another 10%, supporting GPM expansion.That sets up a strong 2HFY26–FY27 earnings runway &added liquidity from the split a rerating looks likely!

With #KCAB & #APLA boasting debt free balancesheets, exceptional Net Current Assets per share & strong forecasted FY26–27F earnings, the 10:1split could be the catalyst that unlocks value long overlooked due to limited liquidity.Will the market now rerate both in line with peers?

@hareshdesoysa I’m hearing the same on current utilisation levels.#KCAB & #ACL still running at 50%. With AWPLR easing & building materials demand picking up, 2HFY26F- FY27F earnings should see strong upside.

With liquidity improving postsplit, a rerating to 11–12× PER looks entirely plausible

Rcvd few msgs on #APLA#KCAB. With the expected growth in demand for cables in2HFY26 &competitors like #SIRA running close to full capacity, #KCAB & #ACL are well positioned for volume growth. #APLA will also benefit frm volume growth and stronger GPs frm reduction in PVC prices

@Channa_Amare 3. Softer RM prices+rising cable demand at KCAB & ACL(2Q–4QFY26) position APLA for strong EPS growth in FY26. Cable demand typically emerges in the early phase of new builds, much like cement.

MPS: Rs 1,240

EPS: Rs 126.3 (TTM) → Rs 190 (+50%) FY26F

PER: 9.8× (TTM) → 6.5× FY26F

@Neerajan_S@Channa_Amare Yes CIND and APLA GP margins should improve in coming quarters. If oil goes below 60 as most expect, we can expect PVC prices to come down even more

@Channa_Amare 3. Softer RM prices+rising cable demand at KCAB & ACL(2Q–4QFY26) position APLA for strong EPS growth in FY26. Cable demand typically emerges in the early phase of new builds, much like cement.

MPS: Rs 1,240

EPS: Rs 126.3 (TTM) → Rs 190 (+50%) FY26F

PER: 9.8× (TTM) → 6.5× FY26F

@Channa_Amare 2. The real kicker for APLA is the plunging PVC resin prices, with prices touching a 5-yr low in September 2025, GPMs should expand (~29% FY26) & EPS.

PVC Resin Futures (Oct ’25 deliveries):

Jan25: CNY5,479/MT → Jun25: CNY4,906/MT (-10% YTD) → Sep25: CNY 4,763/MT (-3% QoQ)

Brent down >18.5% from YTD Peak = major macro boost for SL. Lower oil import bill narrows current account deficit (2.5% of GDP), eases inflation, supports additional rate cuts (potentially in Sep), boosts GDP growth. Most bullish setup for #CSE in 2H2025 #BrentOil#Equities

Should we expect some funds from maturing bonds especially from private investors to rotate into the CSE in July? Combined with lower oil prices and low interest rates, this could be a key trigger for further upside on the CSE given the pull back experienced over the last 12 days

While many investors track global markets for signals on the CSE, Brent Crude may be the more relevant indicator for the CSE. Oil is now below pre Iran–Israel conflict levels supportive for SL’s Macro fundamentals. A CSE re-rating could follow in due course to reflect the same.

3. A LKR 295Bn bond auction is due on June 27 to partly roll over LKR 336.6Bn in maturing debt. With a primary surplus, the gov’t could retire some debt—reducing bond supply and helping keep yields low and maintain excess liquidity amid rising credit growth.

As per page 19 of PARQs 2025 AR, the Group plans to launch Swisstek Cement. With DP acquiring PowerTech Cement (10% market share), it’s highly likely the brand will be rebranded and operated under PARQ-adding a strategic new vertical to its expanding building materials portfolio

Overhang from potential loss of EU tariff concession to SL’s largest export market is removed. GSP+ access is confirmed through 2027, supporting exporters. Resultant risk premia and counter-specific valuation discounts are expected to reverse #CSE https://t.co/0sl405bcDE

Assuming Chinese rubber glove imports face a 125% reciprocal tariff, a 20% fentanyl-related tariff, and Section 301 tariffs of 7.5% in 2025 rising to 25% in 2026

What’s the impact on Sri Lanka’s Rubber glove exports to the US if China faces a 152.5% tariff in 2025 and 170% in 2026? With China supplying 42% of US medical glove imports in 2024, and SL producing 5% of global output (20% exported to the US), how much does SL stands to gain?

@BuhardeenImtiaz Once governance KPIs are achieved, a coupon reduction will be triggered in the GLB.Bondholders are in agreement as it will reduce the Country Risk Premium (CRP) which will offset the impact on price from the coupon reduction. Reduction in the CRP will help the MLB pricing too